- Germany

- /

- Auto Components

- /

- XTRA:SHA0

European Value Stock Picks That May Be Trading Below Their Worth

Reviewed by Simply Wall St

Amidst cautious optimism in Europe, the pan-European STOXX Europe 600 Index edged slightly higher as investors navigated U.S. trade policy developments and geopolitical efforts to resolve the Russia-Ukraine conflict. In this environment of mixed economic signals and fluctuating indices, identifying stocks that may be undervalued can provide opportunities for investors seeking value; such stocks often exhibit strong fundamentals or potential for growth despite current market challenges.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Sword Group (ENXTPA:SWP) | €33.30 | €64.76 | 48.6% |

| Vestas Wind Systems (CPSE:VWS) | DKK102.35 | DKK204.12 | 49.9% |

| Laboratorio Reig Jofre (BME:RJF) | €2.69 | €5.32 | 49.4% |

| Star7 (BIT:STAR7) | €6.40 | €12.38 | 48.3% |

| Cint Group (OM:CINT) | SEK6.745 | SEK13.29 | 49.2% |

| Surgical Science Sweden (OM:SUS) | SEK157.50 | SEK310.06 | 49.2% |

| Canatu Oyj (HLSE:CANATU) | €12.80 | €24.82 | 48.4% |

| Better Collective (OM:BETCO) | SEK109.20 | SEK216.56 | 49.6% |

| Fodelia Oyj (HLSE:FODELIA) | €7.20 | €13.91 | 48.2% |

| Galderma Group (SWX:GALD) | CHF109.48 | CHF212.91 | 48.6% |

We'll examine a selection from our screener results.

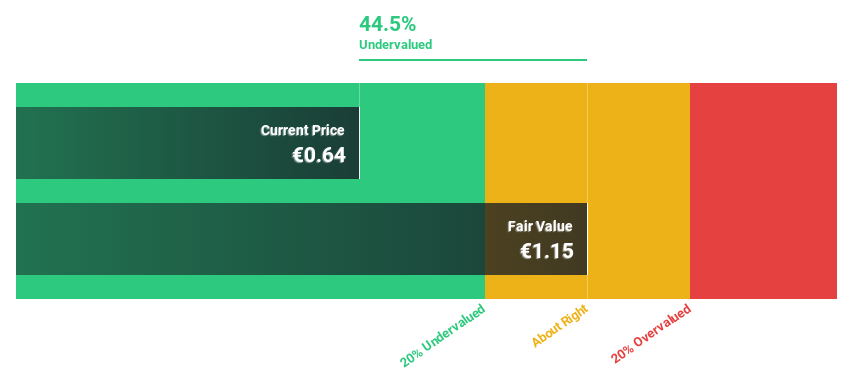

Prosegur Cash (BME:CASH)

Overview: Prosegur Cash, S.A. offers cash cycle management and payment automation services across various sectors including retail, financial institutions, and government agencies, with a market cap of €966.90 million.

Operations: Prosegur Cash generates revenue by providing cash cycle management and payment automation services to sectors such as retail, financial institutions, government agencies, central banks, mints, and jewellery stores.

Estimated Discount To Fair Value: 43.7%

Prosegur Cash appears undervalued, trading 43.7% below its estimated fair value of €1.16. Recent earnings showed a strong growth with net income rising to €89.07 million from €62.93 million, supported by a share repurchase program worth €8 million. Despite high debt levels and slower revenue growth compared to the market, its earnings are forecasted to grow significantly at 22% annually over the next three years, outpacing the Spanish market's average growth rate.

- According our earnings growth report, there's an indication that Prosegur Cash might be ready to expand.

- Take a closer look at Prosegur Cash's balance sheet health here in our report.

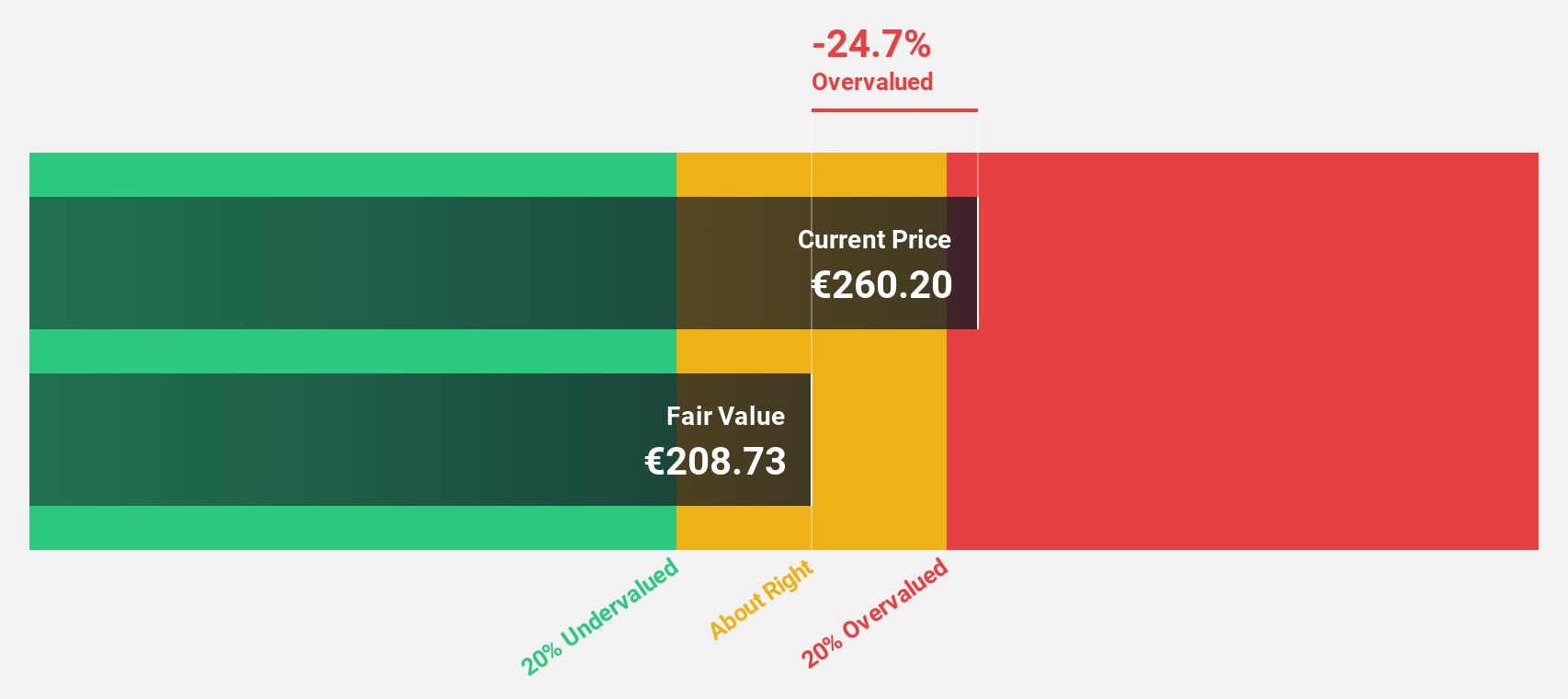

Safran (ENXTPA:SAF)

Overview: Safran SA, along with its subsidiaries, operates in the aerospace and defense sectors globally and has a market capitalization of approximately €103.57 billion.

Operations: The company's revenue is primarily derived from Aerospace Propulsion (€13.65 billion), Aeronautical Equipment, Defense and Aerosystems (€10.62 billion), and Aircraft Interiors (€3.04 billion).

Estimated Discount To Fair Value: 11.5%

Safran is trading at €248.5, about 11.5% below its estimated fair value of €280.87, suggesting potential undervaluation based on cash flows. Despite a net loss of €667 million in 2024, revenue increased to €28.15 billion from the previous year's €24.13 billion, and earnings are expected to grow by 42% annually as profitability returns within three years. Safran's strategic focus includes bolt-on acquisitions and a substantial share buyback program worth up to €5 billion by 2028.

- Insights from our recent growth report point to a promising forecast for Safran's business outlook.

- Unlock comprehensive insights into our analysis of Safran stock in this financial health report.

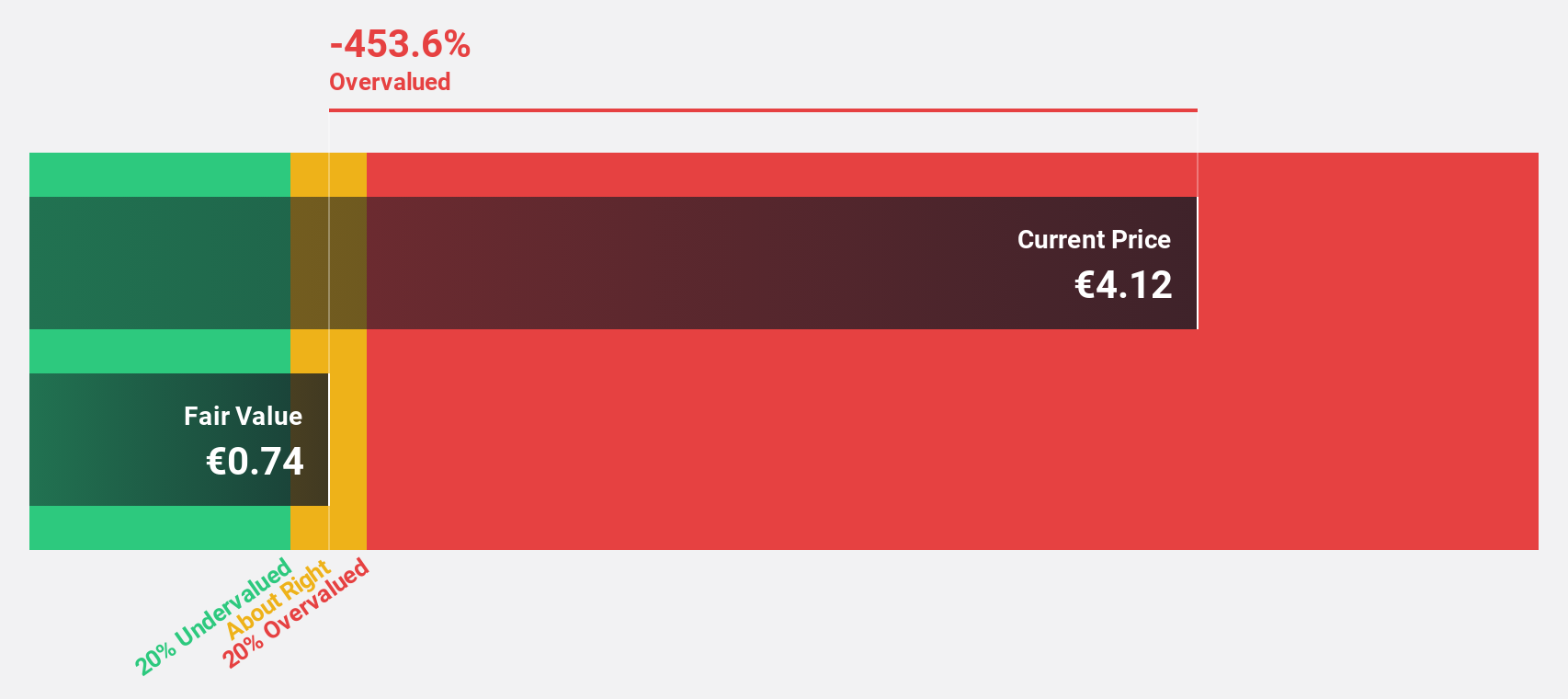

Schaeffler (XTRA:SHA0)

Overview: Schaeffler AG, along with its subsidiaries, develops, manufactures, and sells components and systems for industrial applications across Europe, the Americas, China, and the Asia Pacific; it has a market cap of approximately €4.69 billion.

Operations: The company's revenue segments include Automotive Technologies at €9.73 billion, Vehicle Lifetime Solutions at €2.50 billion, and Bearings & Industrial Solutions at €3.99 billion.

Estimated Discount To Fair Value: 25.1%

Schaeffler, trading at €4.97, is significantly undervalued with an estimated fair value of €6.64. Despite recent shareholder dilution and a dividend yield of 9.06% not covered by earnings or free cash flow, the company's earnings are forecast to grow substantially at 65% annually, outpacing the German market's growth rate. However, profit margins have declined to 0.9%, and interest payments remain poorly covered by earnings, highlighting financial challenges amidst strong growth potential.

- Our expertly prepared growth report on Schaeffler implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of Schaeffler here with our thorough financial health report.

Key Takeaways

- Discover the full array of 197 Undervalued European Stocks Based On Cash Flows right here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:SHA0

Schaeffler

Develops, manufactures, and sells components and system for industrial applications in Europe, the Americas, China, and the Asia Pacific.

High growth potential slight.

Similar Companies

Market Insights

Community Narratives