Advertisement

Has BNP Paribas Run Too Far After 45% Gain Or Is There Still Value?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether BNP Paribas still represents good value after such a strong run, or if you are arriving late to the story, this breakdown will walk you through what the current price is really telling us.

- The stock has climbed 2.6% over the last week and 12.5% over the past month. It is now up 44.6% over 1 year and 135.8% over 5 years, so the market clearly likes the story so far.

- Recent coverage has highlighted how European banks are benefiting from higher interest rates and more resilient-than-expected economic conditions. This has helped lift sentiment toward major lenders such as BNP Paribas. At the same time, ongoing discussions around regulation and capital requirements are reminding investors that the sector is not without its risks.

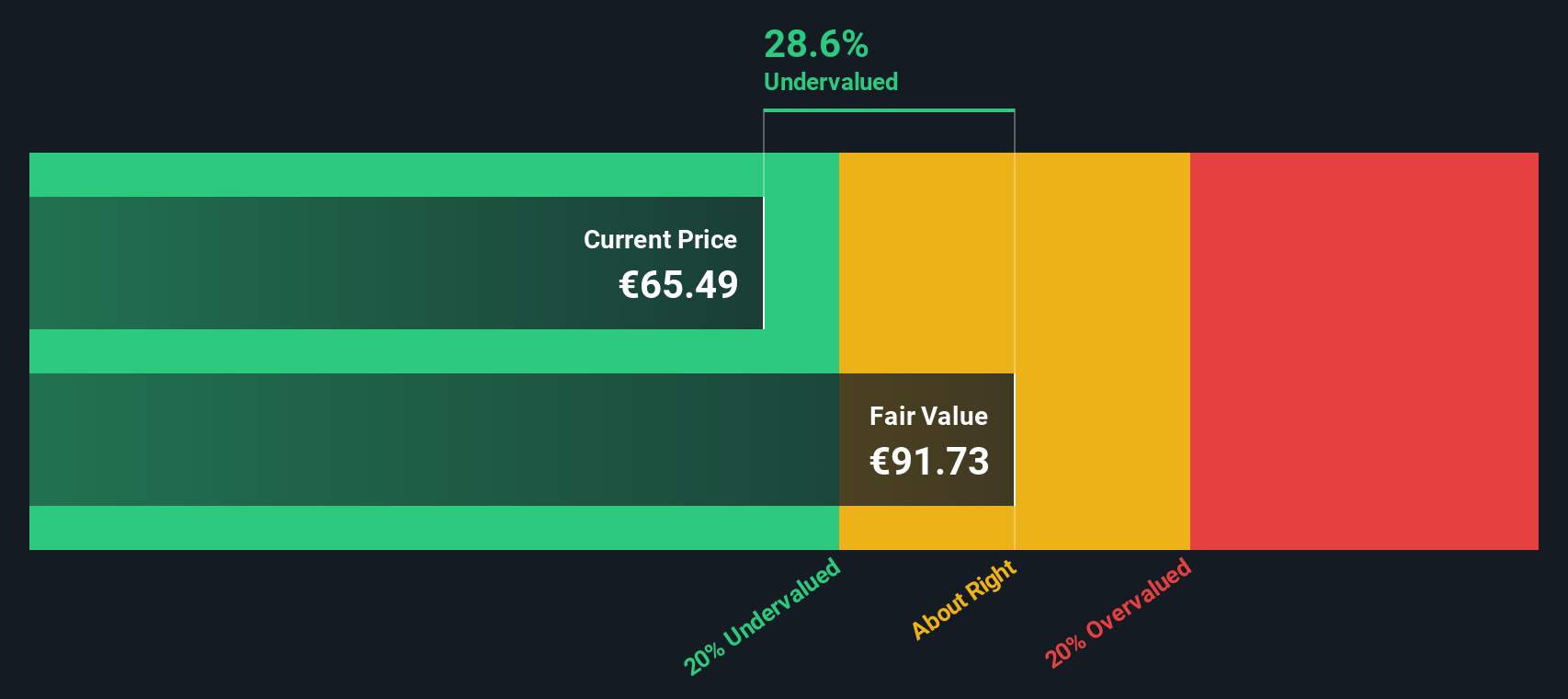

- Against that backdrop, BNP Paribas currently scores a 4/6 valuation score, suggesting it looks undervalued on several key checks. We will unpack those methods next and introduce a sharper way to think about fair value by the end of this article.

Find out why BNP Paribas's 44.6% return over the last year is lagging behind its peers.

Approach 1: BNP Paribas Excess Returns Analysis

The Excess Returns model looks at how efficiently BNP Paribas turns shareholder capital into profits, then compares those returns to the cost of that capital. In simple terms, it asks whether each euro invested in the bank is earning more than it costs to raise.

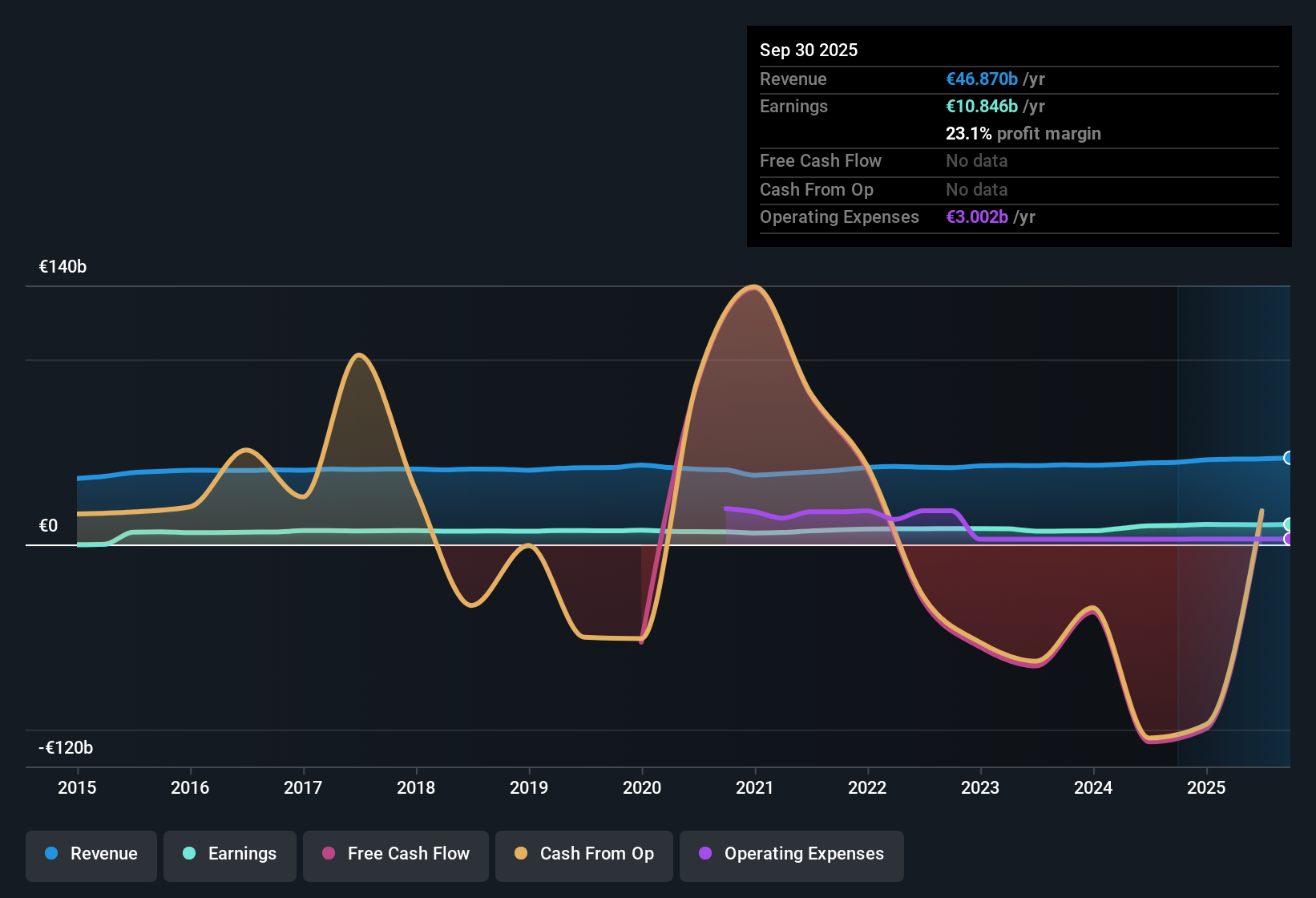

BNP Paribas has a Book Value of €111.07 per share and a Stable Book Value estimate of €114.66 per share, based on forecasts from 9 analysts. Its Stable EPS is estimated at €11.82 per share, derived from weighted future Return on Equity expectations from 14 analysts. That implies an Average Return on Equity of 10.30%.

However, the Cost of Equity is higher at €14.10 per share, which leads to an Excess Return of €-2.29 per share. Based on these inputs, the model indicates an intrinsic value of roughly €92.24 per share, implying the stock is about 19.5% undervalued versus the current market price.

Result: UNDERVALUED

Our Excess Returns analysis suggests BNP Paribas is undervalued by 19.5%. Track this in your watchlist or portfolio, or discover 916 more undervalued stocks based on cash flows.

Approach 2: BNP Paribas Price vs Earnings

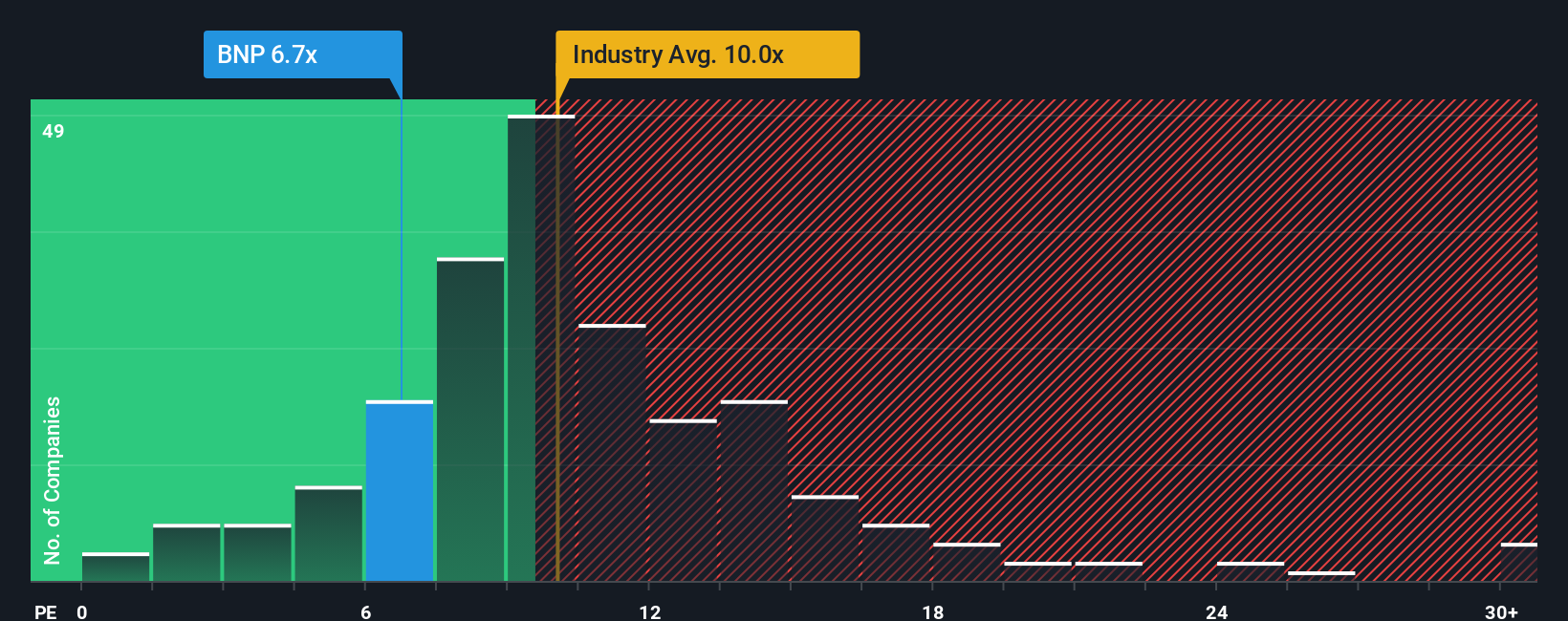

For established, profitable banks like BNP Paribas, the Price to Earnings, or PE, ratio is a practical way to gauge value because it links what investors pay today to the profits the business is already generating. In general, companies with stronger growth prospects and lower perceived risk can justify a higher PE ratio, while slower growing or riskier firms tend to trade on lower multiples.

BNP Paribas currently trades on a PE of 7.61x, which sits below both the wider Banks industry average of around 10.56x and the peer group average of about 8.98x. Simply Wall St also calculates a proprietary Fair Ratio for BNP Paribas of 8.35x. This reflects what its PE should be after adjusting for factors such as earnings growth outlook, profitability, risk profile, industry positioning and market capitalization. This tailored Fair Ratio is more informative than a simple comparison with peers or the sector, because it accounts for the specific strengths and risks of BNP Paribas rather than assuming all banks deserve the same multiple.

With the current PE of 7.61x sitting below the Fair Ratio of 8.35x, BNP Paribas still screens as modestly undervalued on this earnings based lens.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your BNP Paribas Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page that lets you attach your own story about BNP Paribas to the numbers. You can link your assumptions for future revenue, earnings and margins into a financial forecast, turn that into a fair value, and then compare that fair value with today’s price to decide whether to buy, hold or sell. The whole view updates automatically as new news, earnings or regulatory developments come in. For example, one investor might build a bullish BNP Paribas Narrative around accelerating digital finance expansion, improving margins and a fair value closer to the top analyst target of about €100. A more cautious investor could focus on Eurozone growth constraints, regulatory pressure and legal risks and land nearer the low end around €77. Both of those perspectives are visible, comparable and easy to explore within the platform used by millions of investors so you can quickly see which story, and which fair value, you find more convincing.

Do you think there's more to the story for BNP Paribas? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BNP Paribas might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:BNP

BNP Paribas

Provides various banking and financial products and services in Europe, the Middle East, Africa, the Americas, and the Asia Pacific.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

40 followersusers have followed this narrative

6 commentsusers have commented on this narrative

11 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

115 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative