- Finland

- /

- Electric Utilities

- /

- HLSE:FORTUM

Do These 3 Checks Before Buying Fortum Oyj (HEL:FORTUM) For Its Upcoming Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Fortum Oyj (HEL:FORTUM) is about to go ex-dividend in just three days. The ex-dividend date is usually set to be two business days before the record date, which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade can take two business days or more to settle. In other words, investors can purchase Fortum Oyj's shares before the 2nd of April in order to be eligible for the dividend, which will be paid on the 10th of April.

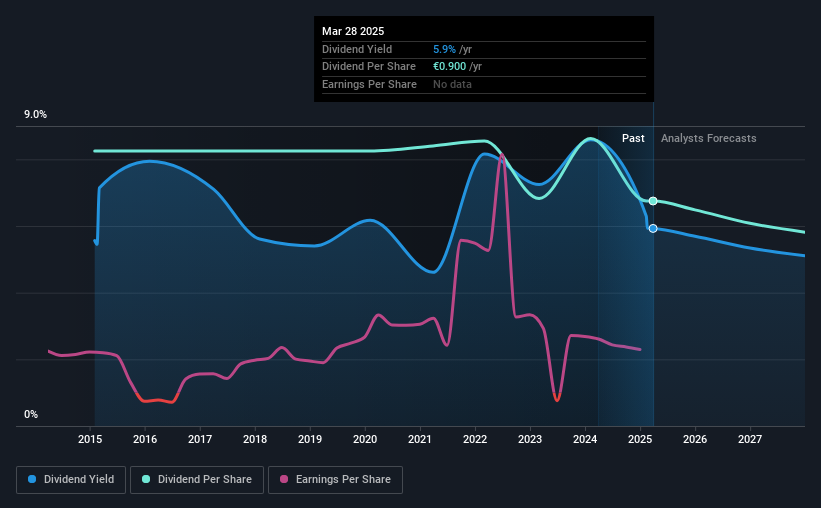

The company's next dividend payment will be €1.40 per share, on the back of last year when the company paid a total of €0.90 to shareholders. Calculating the last year's worth of payments shows that Fortum Oyj has a trailing yield of 5.9% on the current share price of €15.185. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! As a result, readers should always check whether Fortum Oyj has been able to grow its dividends, or if the dividend might be cut.

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Fortum Oyj paid out more than half (69%) of its earnings last year, which is a regular payout ratio for most companies. A useful secondary check can be to evaluate whether Fortum Oyj generated enough free cash flow to afford its dividend. Fortum Oyj paid out more free cash flow than it generated - 112%, to be precise - last year, which we think is concerningly high. We're curious about why the company paid out more cash than it generated last year, since this can be one of the early signs that a dividend may be unsustainable.

While Fortum Oyj's dividends were covered by the company's reported profits, cash is somewhat more important, so it's not great to see that the company didn't generate enough cash to pay its dividend. Cash is king, as they say, and were Fortum Oyj to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

See our latest analysis for Fortum Oyj

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If earnings fall far enough, the company could be forced to cut its dividend. So we're not too excited that Fortum Oyj's earnings are down 4.9% a year over the past five years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Fortum Oyj's dividend payments per share have declined at 2.0% per year on average over the past 10 years, which is uninspiring.

To Sum It Up

Should investors buy Fortum Oyj for the upcoming dividend? It's definitely not great to see earnings per share shrinking. The company paid out an acceptable percentage of its income, but an uncomfortably high percentage of its cash flow over the past year. It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

So if you're still interested in Fortum Oyj despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. To that end, you should learn about the 2 warning signs we've spotted with Fortum Oyj (including 1 which is a bit unpleasant).

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:FORTUM

Fortum Oyj

Engages in the generation and sale of electricity and heat in Finland, Sweden, the Netherlands, Ireland, Denmark, Belgium, the United Kingdom, Switzerland, Spain, France, Germany, Norway, and internationally.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)