The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Finnair Oyj (HEL:FIA1S) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Finnair Oyj

How Much Debt Does Finnair Oyj Carry?

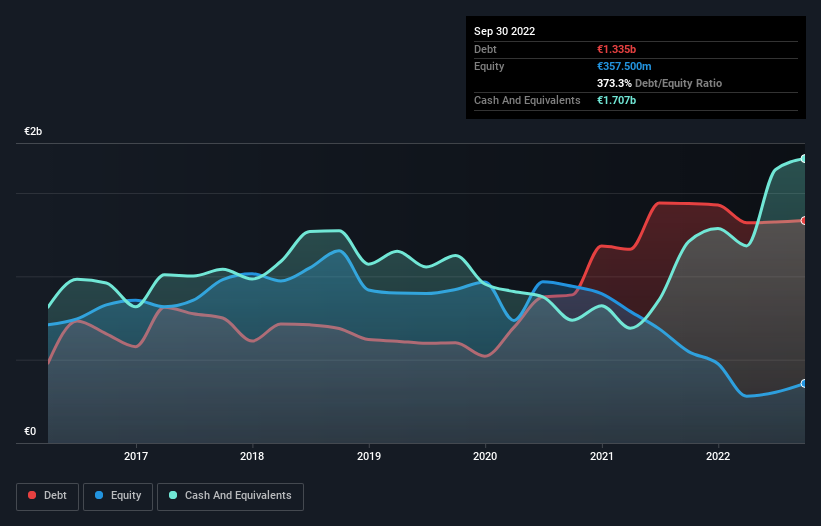

The image below, which you can click on for greater detail, shows that Finnair Oyj had debt of €1.33b at the end of September 2022, a reduction from €1.44b over a year. But on the other hand it also has €1.71b in cash, leading to a €371.9m net cash position.

How Healthy Is Finnair Oyj's Balance Sheet?

According to the last reported balance sheet, Finnair Oyj had liabilities of €1.80b due within 12 months, and liabilities of €2.16b due beyond 12 months. On the other hand, it had cash of €1.71b and €146.8m worth of receivables due within a year. So it has liabilities totalling €2.11b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the €597.7m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Finnair Oyj would likely require a major re-capitalisation if it had to pay its creditors today. Given that Finnair Oyj has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Finnair Oyj's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Finnair Oyj wasn't profitable at an EBIT level, but managed to grow its revenue by 295%, to €2.1b. When it comes to revenue growth, that's like nailing the game winning 3-pointer!

So How Risky Is Finnair Oyj?

While Finnair Oyj lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow €253m. So although it is loss-making, it doesn't seem to have too much near-term balance sheet risk, keeping in mind the net cash. The saving grace for the stock is the strong revenue growth of 295% over the last twelve months. But we genuinely do think the balance sheet is a risky. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how Finnair Oyj's profit, revenue, and operating cashflow have changed over the last few years.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:FIA1S

Finnair Oyj

Operates in the airline business in North Atlantic, Asia, Europe, Middle East, and internationally.

Very undervalued with imperfect balance sheet.