- Finland

- /

- Electronic Equipment and Components

- /

- HLSE:ACG1V

Aspocomp Group Oyj's (HEL:ACG1V) Shareholders Will Receive A Bigger Dividend Than Last Year

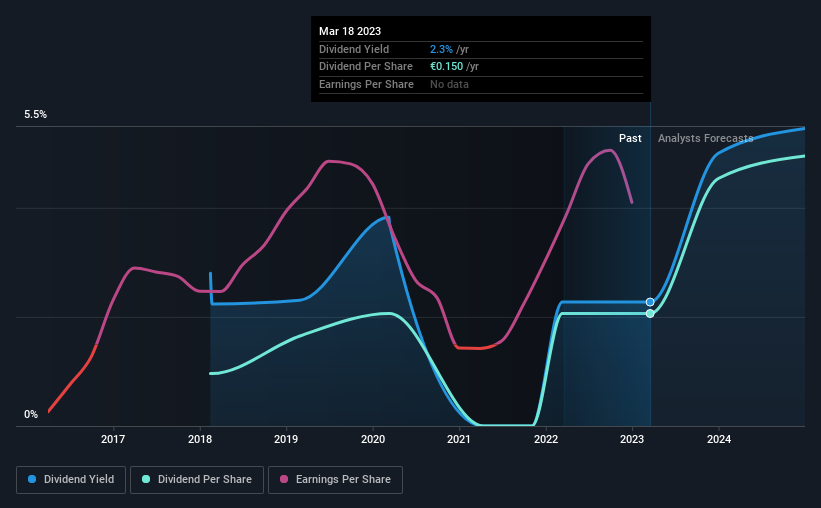

The board of Aspocomp Group Oyj (HEL:ACG1V) has announced that it will be increasing its dividend by 40% on the 2nd of May to €0.21, up from last year's comparable payment of €0.15. This will take the dividend yield to an attractive 2.3%, providing a nice boost to shareholder returns.

View our latest analysis for Aspocomp Group Oyj

Aspocomp Group Oyj's Payment Has Solid Earnings Coverage

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Prior to this announcement, Aspocomp Group Oyj was quite comfortably covering its dividend with earnings and it was paying more than 75% of its free cash flow to shareholders. The company is clearly earning enough to pay this type of dividend, but it is definitely focused on returning cash to shareholders, rather than growing the business.

Looking forward, earnings per share is forecast to rise by 40.4% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 33%, which is in the range that makes us comfortable with the sustainability of the dividend.

Aspocomp Group Oyj's Dividend Has Lacked Consistency

It's comforting to see that Aspocomp Group Oyj has been paying a dividend for a number of years now, however it has been cut at least once in that time. This suggests that the dividend might not be the most reliable. Since 2018, the annual payment back then was €0.07, compared to the most recent full-year payment of €0.15. This means that it has been growing its distributions at 16% per annum over that time. Aspocomp Group Oyj has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Looks Likely To Grow

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. We are encouraged to see that Aspocomp Group Oyj has grown earnings per share at 22% per year over the past five years. Aspocomp Group Oyj is clearly able to grow rapidly while still returning cash to shareholders, positioning it to become a strong dividend payer in the future.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think Aspocomp Group Oyj's payments are rock solid. The low payout ratio is a redeeming feature, but generally we are not too happy with the payments Aspocomp Group Oyj has been making. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For instance, we've picked out 2 warning signs for Aspocomp Group Oyj that investors should take into consideration. Is Aspocomp Group Oyj not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:ACG1V

Aspocomp Group Oyj

Manufactures and sells printed circuit boards (PCBs) in Finland, Europe, and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)