Advertisement

- Spain

- /

- Electric Utilities

- /

- BME:ELE

Endesa (BME:ELE) Hasn't Managed To Accelerate Its Returns

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. However, after briefly looking over the numbers, we don't think Endesa (BME:ELE) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Endesa, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

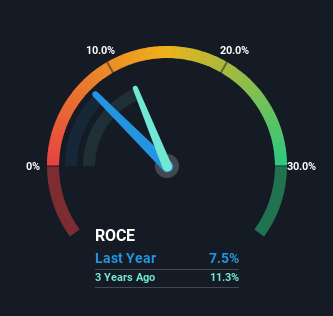

0.075 = €2.0b ÷ (€39b - €12b) (Based on the trailing twelve months to September 2024).

Thus, Endesa has an ROCE of 7.5%. On its own, that's a low figure but it's around the 7.1% average generated by the Electric Utilities industry.

View our latest analysis for Endesa

In the above chart we have measured Endesa's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Endesa for free.

So How Is Endesa's ROCE Trending?

Things have been pretty stable at Endesa, with its capital employed and returns on that capital staying somewhat the same for the last five years. This tells us the company isn't reinvesting in itself, so it's plausible that it's past the growth phase. With that in mind, unless investment picks up again in the future, we wouldn't expect Endesa to be a multi-bagger going forward. That being the case, it makes sense that Endesa has been paying out 73% of its earnings to its shareholders. Most shareholders probably know this and own the stock for its dividend.

What We Can Learn From Endesa's ROCE

We can conclude that in regards to Endesa's returns on capital employed and the trends, there isn't much change to report on. Unsurprisingly, the stock has only gained 16% over the last five years, which potentially indicates that investors are accounting for this going forward. As a result, if you're hunting for a multi-bagger, we think you'd have more luck elsewhere.

One more thing to note, we've identified 3 warning signs with Endesa and understanding them should be part of your investment process.

While Endesa may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Endesa might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:ELE

Endesa

Engages in the generation, distribution, and sale of electricity in Spain, Portugal, France, Germany, the United Kingdom, Switzerland, Luxembourg, the Netherlands, Singapore, Italy, Morocco, and internationally.

Proven track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1156.8% undervalued

34 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.5% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9219.7% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19010.1% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

ES

Esteban on Mastercard ·

Capital-light, high-return payment network that is successfully expanding into high-margin security and data services faster than its peers.

Fair Value:US$395.534.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JM

JM7 on Soluna Holdings ·

Soluna: Powering Renewable AI, Funding the Risk

Fair Value:US$985.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on RENOVA ·

Empowering the future with “new energy”

Fair Value:JP¥690.0941.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.8% undervalued

70 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23038.1% overvalued

89 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative