These 4 Measures Indicate That Indra Sistemas (BME:IDR) Is Using Debt Reasonably Well

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Indra Sistemas, S.A. (BME:IDR) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Indra Sistemas

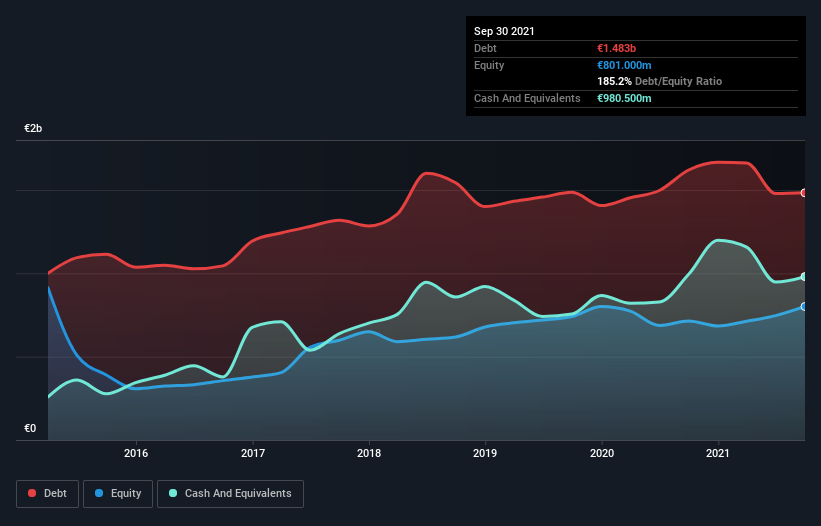

What Is Indra Sistemas's Debt?

The image below, which you can click on for greater detail, shows that Indra Sistemas had debt of €1.48b at the end of September 2021, a reduction from €1.62b over a year. However, it does have €980.5m in cash offsetting this, leading to net debt of about €502.7m.

How Healthy Is Indra Sistemas' Balance Sheet?

We can see from the most recent balance sheet that Indra Sistemas had liabilities of €1.85b falling due within a year, and liabilities of €1.76b due beyond that. Offsetting this, it had €980.5m in cash and €1.51b in receivables that were due within 12 months. So its liabilities total €1.13b more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of €1.60b, so it does suggest shareholders should keep an eye on Indra Sistemas' use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Indra Sistemas has net debt worth 2.2 times EBITDA, which isn't too much, but its interest cover looks a bit on the low side, with EBIT at only 5.9 times the interest expense. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. Pleasingly, Indra Sistemas is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 147% gain in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Indra Sistemas's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Indra Sistemas generated free cash flow amounting to a very robust 88% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

Happily, Indra Sistemas's impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. But, on a more sombre note, we are a little concerned by its level of total liabilities. Looking at all the aforementioned factors together, it strikes us that Indra Sistemas can handle its debt fairly comfortably. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Indra Sistemas has 2 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:IDR

Indra Sistemas

Operates as a technology and consulting company for aerospace, defense, and mobility business worldwide.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives