Advertisement

- Germany

- /

- Real Estate

- /

- XTRA:WCMK

Does WCM Beteiligungs- und Grundbesitz-AG (ETR:WCMK) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that WCM Beteiligungs- und Grundbesitz-AG (ETR:WCMK) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for WCM Beteiligungs- und Grundbesitz-AG

What Is WCM Beteiligungs- und Grundbesitz-AG's Debt?

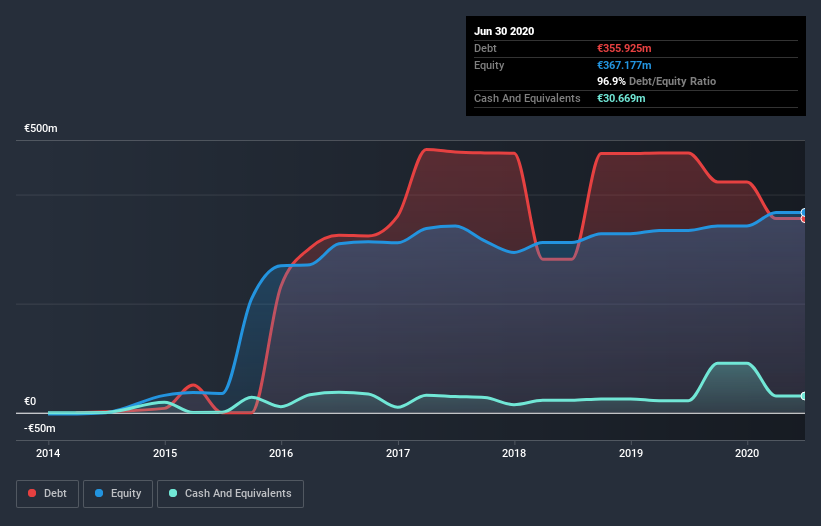

The image below, which you can click on for greater detail, shows that WCM Beteiligungs- und Grundbesitz-AG had debt of €355.8m at the end of June 2020, a reduction from €476.2m over a year. On the flip side, it has €30.7m in cash leading to net debt of about €325.2m.

How Healthy Is WCM Beteiligungs- und Grundbesitz-AG's Balance Sheet?

According to the last reported balance sheet, WCM Beteiligungs- und Grundbesitz-AG had liabilities of €50.8m due within 12 months, and liabilities of €378.1m due beyond 12 months. On the other hand, it had cash of €30.7m and €5.07m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by €393.1m.

This deficit is considerable relative to its market capitalization of €547.2m, so it does suggest shareholders should keep an eye on WCM Beteiligungs- und Grundbesitz-AG's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

WCM Beteiligungs- und Grundbesitz-AG has a rather high debt to EBITDA ratio of 9.3 which suggests a meaningful debt load. However, its interest coverage of 4.3 is reasonably strong, which is a good sign. Fortunately, WCM Beteiligungs- und Grundbesitz-AG grew its EBIT by 3.3% in the last year, slowly shrinking its debt relative to earnings. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since WCM Beteiligungs- und Grundbesitz-AG will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, WCM Beteiligungs- und Grundbesitz-AG recorded free cash flow worth 53% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

WCM Beteiligungs- und Grundbesitz-AG's net debt to EBITDA was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. For example, its conversion of EBIT to free cash flow is relatively strong. Taking the abovementioned factors together we do think WCM Beteiligungs- und Grundbesitz-AG's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Consider for instance, the ever-present spectre of investment risk. We've identified 6 warning signs with WCM Beteiligungs- und Grundbesitz-AG (at least 2 which are a bit concerning) , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade WCM Beteiligungs- und Grundbesitz-AG, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if WCM Beteiligungs- und Grundbesitz-AG might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About XTRA:WCMK

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor