Advertisement

The Bull Case For Bayer (XTRA:BAYN) Could Change Following Promising Parkinson’s Trial and U.S. Farming Initiative

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this month, Bayer and its U.S. subsidiary BlueRock Therapeutics reported positive 36-month Phase I data for bemdaneprocel, an investigational cell therapy for Parkinson's disease, with encouraging safety results and favorable trends in motor function outcomes.

- The company also expanded its commitment to sustainable agriculture by launching the first U.S. Bayer ForwardFarm in the Midwest, highlighting progress in regenerative farming practices alongside its healthcare innovations.

- We'll examine how positive results from Bayer's Parkinson's therapy program could influence the company's long-term investment narrative.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Bayer Investment Narrative Recap

To be a shareholder in Bayer, you need to believe that its pipeline innovation and focus on both healthcare and sustainable agriculture will drive value over the long term, despite ongoing legal and regulatory challenges. While positive Phase I data in Parkinson’s disease research and the launch of Bayer’s ForwardFarm in the Midwest point to progress and pipeline strength, the most important short-term catalyst, pipeline-driven revenue replacement amid patent expirations, remains only modestly impacted by the latest news, while large-scale litigation and regulatory risks continue to overshadow sentiment.

Of the recent announcements, the advancement of bemdaneprocel in Parkinson’s disease is the most relevant, reinforcing confidence in Bayer’s late-stage pharmaceuticals pipeline just as competitive pressure rises in its core segments. This positive clinical development could support Bayer’s efforts to offset revenue impacts from generic competition and patent losses, which are central to its investment story as it strives for sustainable profit growth.

Yet, in contrast to these innovations, investors should be aware of persistent legal liabilities and uncertainties that continue to threaten cash flow and...

Read the full narrative on Bayer (it's free!)

Bayer's outlook anticipates €48.0 billion in revenue and €3.1 billion in earnings by 2028. This scenario relies on a 1.3% annual revenue growth rate and a €6.5 billion increase in earnings from the current level of €-3.4 billion.

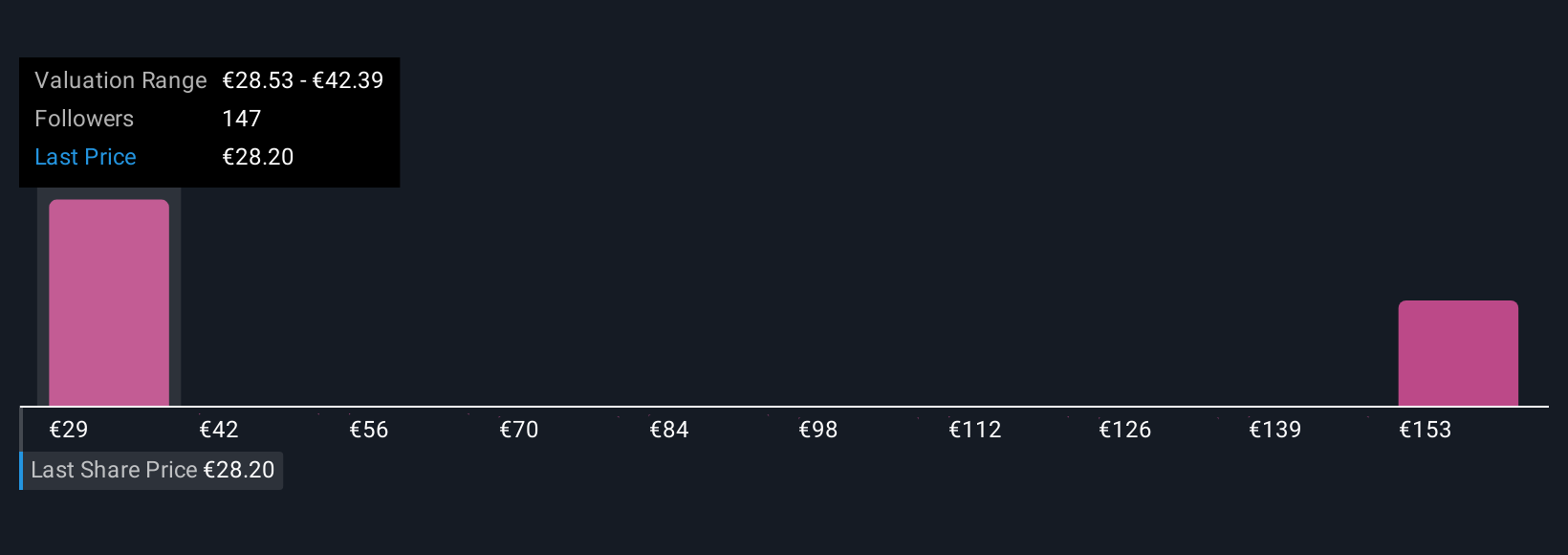

Uncover how Bayer's forecasts yield a €28.53 fair value, in line with its current price.

Exploring Other Perspectives

Fourteen distinct fair value estimates from the Simply Wall St Community range widely, from €28.53 to €167.20 per share. Despite pipeline progress, unresolved litigation risk remains a key theme influencing sentiment and future performance, so compare different viewpoints before deciding where you stand.

Explore 14 other fair value estimates on Bayer - why the stock might be worth over 5x more than the current price!

Build Your Own Bayer Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Bayer research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bayer research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bayer's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our top stock finds are flying under the radar-for now. Get in early:

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bayer might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:BAYN

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor