Wacker Chemie (XTRA:WCH) Faces Earnings Drop but Sees Growth Potential in Asia-Pacific Markets

Reviewed by Simply Wall St

Wacker Chemie (XTRA:WCH) has recently announced its earnings results for the third quarter and nine months ending September 30, 2024, revealing a slight decline in sales and net income compared to the previous year. Despite a strong earnings forecast and strategic product launches, the company faces challenges such as margin pressures and rising raw material costs, which have impacted its financial performance. Readers should expect a detailed analysis of these factors, along with insights into emerging market opportunities and potential risks that could influence Wacker Chemie's future trajectory.

Unlock comprehensive insights into our analysis of Wacker Chemie stock here.

Innovative Factors Supporting Wacker Chemie

Wacker Chemie's earnings forecast of 46.1% annual growth surpasses the German market's 20.1%, underscoring its strong market positioning. The company's seasoned management, with an average tenure of 9 years, ensures strategic stability and continuity, fostering a culture of innovation and resilience. The recent launch of new products, receiving positive customer feedback, highlights its commitment to staying ahead in the competitive market. Financially, the company maintains a satisfactory net debt to equity ratio of 17.8%, indicating sound fiscal health. However, the Price-To-Earnings Ratio of 31.2x suggests a premium valuation compared to the European Chemicals industry average of 17.8x, reflecting investor confidence in its growth prospects.

To dive deeper into how Wacker Chemie's valuation metrics are shaping its market position, check out our detailed analysis of Wacker Chemie's Valuation.Strategic Gaps That Could Affect Wacker Chemie

Challenges persist, with a significant 75.9% drop in earnings growth over the past year, highlighting vulnerabilities in its financial structure. The current net profit margin of 2.2% is notably lower than the previous year's 7.5%, indicating margin pressures. Rising raw material costs further strain profitability, as noted in the latest earnings call. Additionally, the company's revenue growth forecast of 5.2% lags behind industry averages, pointing to potential strategic gaps that need addressing. These financial challenges are compounded by a high dividend payout ratio of 119.8%, which raises concerns about the sustainability of shareholder returns.

Learn about Wacker Chemie's dividend strategy and how it impacts shareholder returns and financial stability.Emerging Markets Or Trends for Wacker Chemie

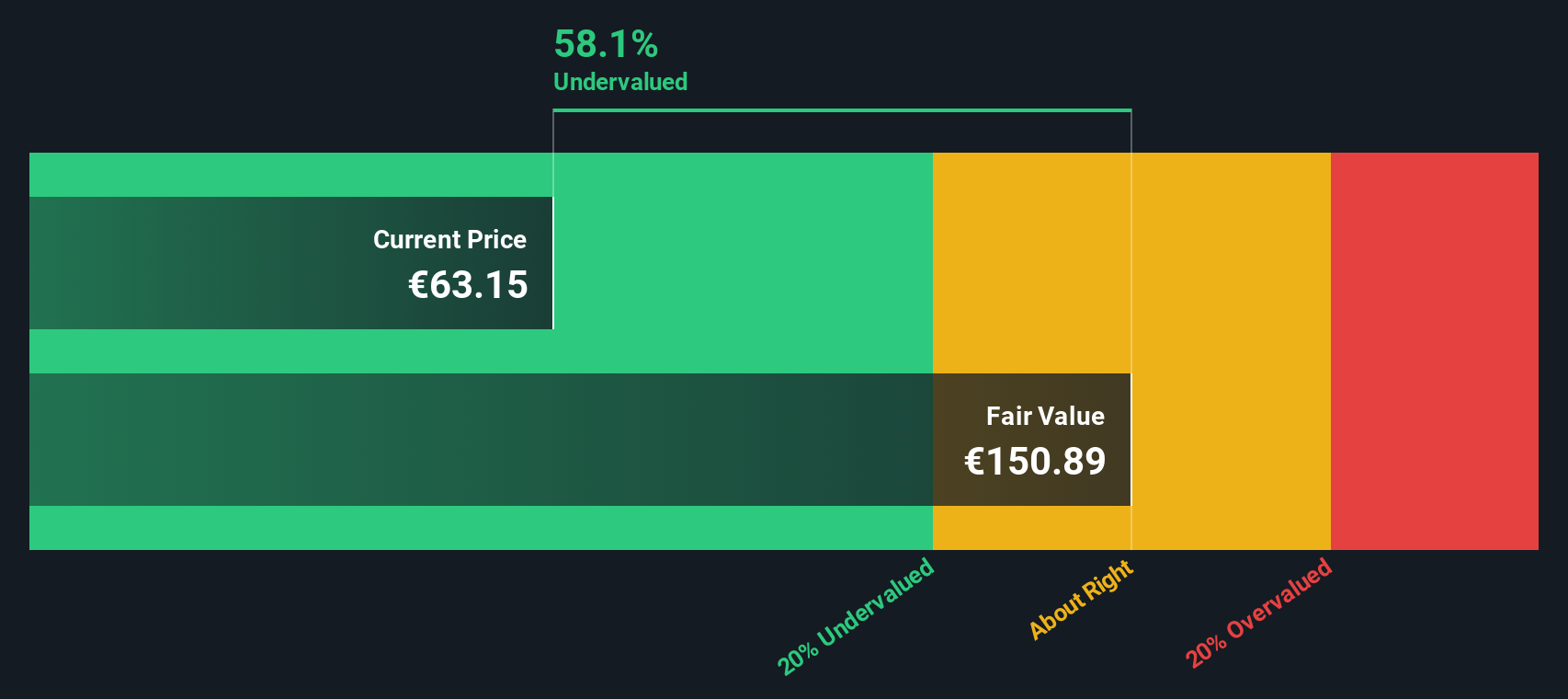

Opportunities abound with the company's shares trading at 62.2% below estimated fair value, suggesting significant upside potential. The target price exceeding the current share price by over 20% indicates room for growth. Strategic alliances and product-related announcements, such as the introduction of innovative product lines, are poised to enhance market share and capitalize on emerging trends. These initiatives could drive expansion into underperforming regions, such as the Asia-Pacific, where targeted marketing efforts are underway to stimulate growth.

To gain deeper insights into Wacker Chemie's historical performance, explore our detailed analysis of past performance.Key Risks and Challenges That Could Impact Wacker Chemie's Success

External threats loom, with economic headwinds and increased market competition posing significant risks. The latest earnings call highlights the company's vigilance in monitoring these factors, emphasizing the need for continuous innovation and customer engagement. Regulatory changes also present potential hurdles, requiring strategic compliance measures to ensure operational stability. The low return on equity forecast of 3.2% further underscores the need for strategic adjustments to maintain competitive advantage and shareholder value.

See what the latest analyst reports say about Wacker Chemie's future prospects and potential market movements.Conclusion

Wacker Chemie's projected annual earnings growth of 46.1% is a testament to its strong market positioning and innovative management, yet the premium Price-To-Earnings Ratio of 31.2x indicates high investor expectations, exceeding both industry and peer averages. While the company faces challenges such as a significant drop in earnings growth and low profit margins, its strategic initiatives in emerging markets, particularly in the Asia-Pacific, offer potential for future expansion and revenue enhancement. However, the sustainability of shareholder returns is questionable due to a high dividend payout ratio, necessitating careful financial management to balance growth opportunities with fiscal prudence. Ultimately, Wacker Chemie's future performance hinges on its ability to navigate economic headwinds and leverage its innovative product offerings to maintain competitive advantage.

Seize The Opportunity

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Wacker Chemie might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About XTRA:WCH

Flawless balance sheet and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)