- Germany

- /

- Specialty Stores

- /

- XTRA:ZAL

3 German Growth Companies With High Insider Ownership And 31% Earnings Growth

Reviewed by Simply Wall St

As the German DAX index shows modest gains amid mixed economic signals, investors are increasingly looking for resilient opportunities in growth companies with strong insider ownership. In this context, stocks that combine robust earnings growth with significant insider stakes can offer a compelling proposition.

Top 10 Growth Companies With High Insider Ownership In Germany

| Name | Insider Ownership | Earnings Growth |

| pferdewetten.de (XTRA:EMH) | 26.8% | 75.4% |

| YOC (XTRA:YOC) | 24.8% | 21.8% |

| Deutsche Beteiligungs (XTRA:DBAN) | 39.4% | 54.1% |

| Exasol (XTRA:EXL) | 25.3% | 104.5% |

| NAGA Group (XTRA:N4G) | 14.1% | 78.3% |

| Alelion Energy Systems (DB:2FZ) | 37.4% | 106.6% |

| Stratec (XTRA:SBS) | 30.9% | 20.5% |

| elumeo (XTRA:ELB) | 25.8% | 99.1% |

| Redcare Pharmacy (XTRA:RDC) | 17.7% | 50.1% |

| Friedrich Vorwerk Group (XTRA:VH2) | 18% | 30.4% |

Here's a peek at a few of the choices from the screener.

Hypoport (XTRA:HYQ)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hypoport SE develops and markets technology platforms for the financial services, property, and insurance industries in Germany, with a market cap of approximately €1.73 billion.

Operations: The company's revenue segments are distributed as follows: Credit Platform €155.60 million, Insurance Platform €66.29 million, and Segment Adjustment €153.22 million.

Insider Ownership: 35.1%

Earnings Growth Forecast: 31.3% p.a.

Hypoport SE demonstrates strong growth potential with significant insider ownership. The company reported a notable turnaround in Q2 2024, with sales rising to €110.62 million and net income reaching €2.4 million from a previous net loss. Earnings are forecast to grow at 31.27% annually, outpacing the German market's 19.3%. Despite recent share price volatility and low future return on equity forecasts, Hypoport’s revenue growth surpasses market expectations at 13.2% per year.

- Click here to discover the nuances of Hypoport with our detailed analytical future growth report.

- Our expertly prepared valuation report Hypoport implies its share price may be too high.

Verve Group (XTRA:M8G)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Verve Group SE operates a software platform for the automated buying and selling of digital advertising space in North America and Europe, with a market cap of €507.82 million.

Operations: Verve Group SE generates revenue from its Demand Side Platforms (DSP) segment, which brings in €51.53 million, and its Supply Side Platforms (SSP) segment, contributing €318.35 million.

Insider Ownership: 25.1%

Earnings Growth Forecast: 20.6% p.a.

Verve Group SE, with substantial insider ownership, is poised for significant growth. Earnings are forecast to grow at 20.62% annually, outpacing the German market's 19.3%. Despite a highly volatile share price and low future return on equity (13.2%), Verve’s revenue is expected to grow faster than the market at 12.4% per year. Recent leadership changes and strategic acquisitions, such as Jun Group, enhance its demand-side capabilities and financial position following a successful bond issue reducing financing costs by €10 million annually.

- Click to explore a detailed breakdown of our findings in Verve Group's earnings growth report.

- Upon reviewing our latest valuation report, Verve Group's share price might be too pessimistic.

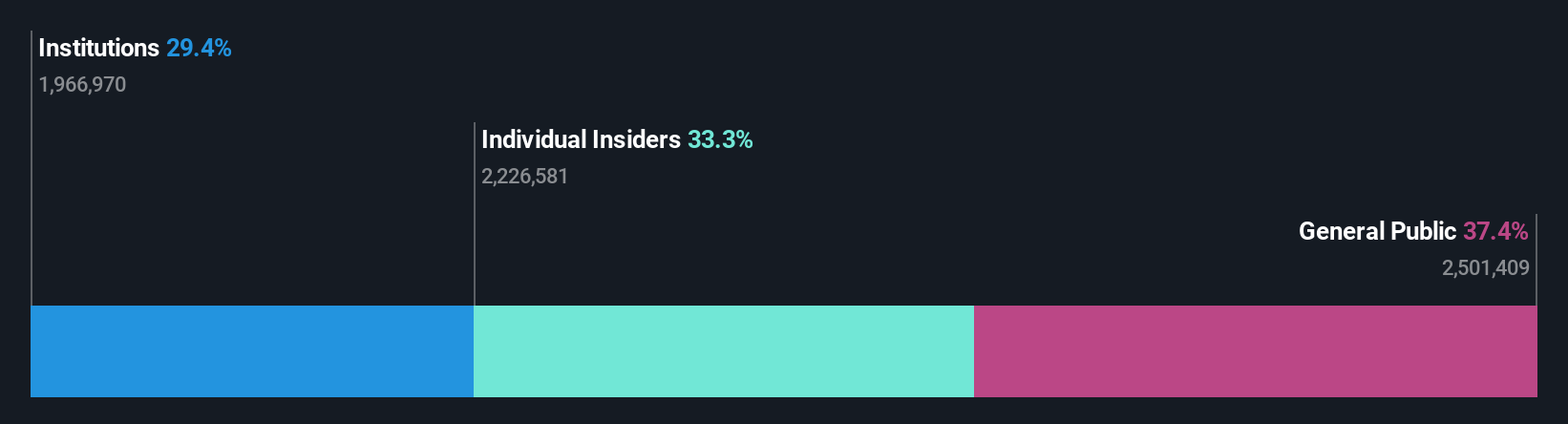

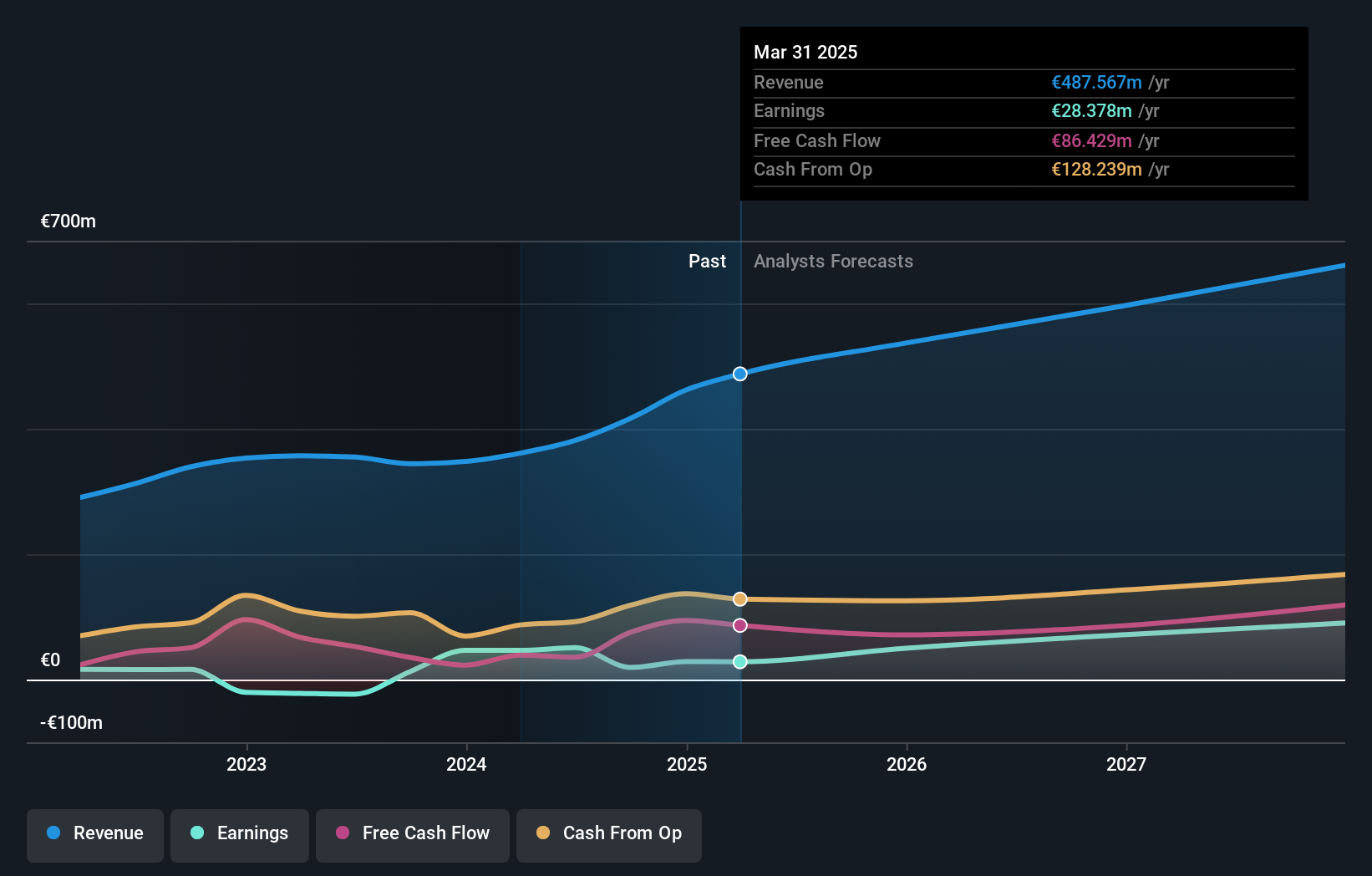

Zalando (XTRA:ZAL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Zalando SE operates an online platform for fashion and lifestyle products and has a market cap of approximately €5.88 billion.

Operations: Zalando SE generates revenue of €10.49 billion from its online platform for fashion and lifestyle products.

Insider Ownership: 10.4%

Earnings Growth Forecast: 24.6% p.a.

Zalando SE demonstrates strong growth potential with high insider ownership, as earnings are forecast to grow 24.64% annually, surpassing the German market's 19.3%. Recent earnings reports show a significant rise in net income for Q2 2024 to €95.7 million from €56.6 million a year ago, reflecting robust performance despite modest revenue growth projections of 5.6% annually. Trading at 60.3% below its estimated fair value and with no substantial insider selling, Zalando remains an attractive growth prospect in Germany’s e-commerce sector.

- Get an in-depth perspective on Zalando's performance by reading our analyst estimates report here.

- Our valuation report unveils the possibility Zalando's shares may be trading at a premium.

Where To Now?

- Access the full spectrum of 19 Fast Growing German Companies With High Insider Ownership by clicking on this link.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Zalando might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:ZAL

Excellent balance sheet with proven track record.