Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that HOCHTIEF Aktiengesellschaft (ETR:HOT) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for HOCHTIEF

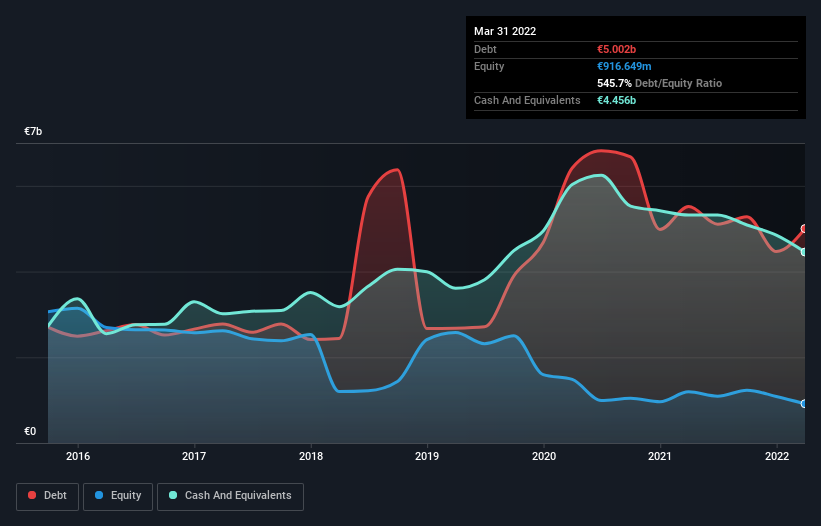

What Is HOCHTIEF's Debt?

As you can see below, HOCHTIEF had €5.00b of debt at March 2022, down from €5.52b a year prior. However, it does have €4.46b in cash offsetting this, leading to net debt of about €546.0m.

A Look At HOCHTIEF's Liabilities

According to the last reported balance sheet, HOCHTIEF had liabilities of €10.6b due within 12 months, and liabilities of €5.41b due beyond 12 months. Offsetting these obligations, it had cash of €4.46b as well as receivables valued at €6.37b due within 12 months. So its liabilities total €5.24b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the €3.09b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, HOCHTIEF would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While HOCHTIEF's low debt to EBITDA ratio of 0.93 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 4.3 times last year does give us pause. But the interest payments are certainly sufficient to have us thinking about how affordable its debt is. We also note that HOCHTIEF improved its EBIT from a last year's loss to a positive €416m. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if HOCHTIEF can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. During the last year, HOCHTIEF generated free cash flow amounting to a very robust 89% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Our View

HOCHTIEF's level of total liabilities and interest cover definitely weigh on it, in our esteem. But its conversion of EBIT to free cash flow tells a very different story, and suggests some resilience. Taking the abovementioned factors together we do think HOCHTIEF's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 4 warning signs with HOCHTIEF (at least 1 which is a bit concerning) , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if HOCHTIEF might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:HOT

Average dividend payer with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|41.9% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|31.9% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|24.9% undervalued

MA

Community Contributor