Advertisement

- China

- /

- Gas Utilities

- /

- SHSE:600681

3 Global Penny Stocks With Market Caps Over US$40M

Simply Wall St

Reviewed by Simply Wall St

Global markets have been navigating a complex landscape marked by geopolitical tensions and fluctuating trade policies, with recent events in the Middle East impacting oil prices and causing volatility in stock indices. For investors exploring opportunities beyond mainstream stocks, penny stocks—typically representing smaller or newer companies—remain a relevant area of interest despite their somewhat outdated label. By focusing on those with solid financials and potential for growth, investors can uncover promising opportunities among these lesser-known entities.

Top 10 Penny Stocks Globally

| Name | Share Price | Market Cap | Rewards & Risks |

| Lever Style (SEHK:1346) | HK$1.23 | HK$788.69M | ✅ 4 ⚠️ 1 View Analysis > |

| Foresight Group Holdings (LSE:FSG) | £3.96 | £445.19M | ✅ 4 ⚠️ 1 View Analysis > |

| Warpaint London (AIM:W7L) | £4.05 | £327.19M | ✅ 5 ⚠️ 3 View Analysis > |

| Angler Gaming (NGM:ANGL) | SEK3.70 | SEK277.44M | ✅ 4 ⚠️ 2 View Analysis > |

| CNMC Goldmine Holdings (Catalist:5TP) | SGD0.44 | SGD178.33M | ✅ 3 ⚠️ 2 View Analysis > |

| Tasmea (ASX:TEA) | A$3.19 | A$753.99M | ✅ 3 ⚠️ 2 View Analysis > |

| Yangzijiang Shipbuilding (Holdings) (SGX:BS6) | SGD2.28 | SGD8.97B | ✅ 5 ⚠️ 0 View Analysis > |

| Bredband2 i Skandinavien (OM:BRE2) | SEK2.365 | SEK2.26B | ✅ 4 ⚠️ 1 View Analysis > |

| DXN Holdings Bhd (KLSE:DXN) | MYR0.50 | MYR2.49B | ✅ 5 ⚠️ 0 View Analysis > |

| Croma Security Solutions Group (AIM:CSSG) | £0.875 | £12.05M | ✅ 3 ⚠️ 3 View Analysis > |

Click here to see the full list of 5,630 stocks from our Global Penny Stocks screener.

Let's explore several standout options from the results in the screener.

Cosmo Lady (China) Holdings (SEHK:2298)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Cosmo Lady (China) Holdings Company Limited is an investment holding company involved in the design, research, development, and sale of branded intimate wear products in the People's Republic of China, with a market cap of HK$529.58 million.

Operations: The company generates revenue of CN¥3.01 billion from the designing, marketing, and selling of intimate wear products.

Market Cap: HK$529.58M

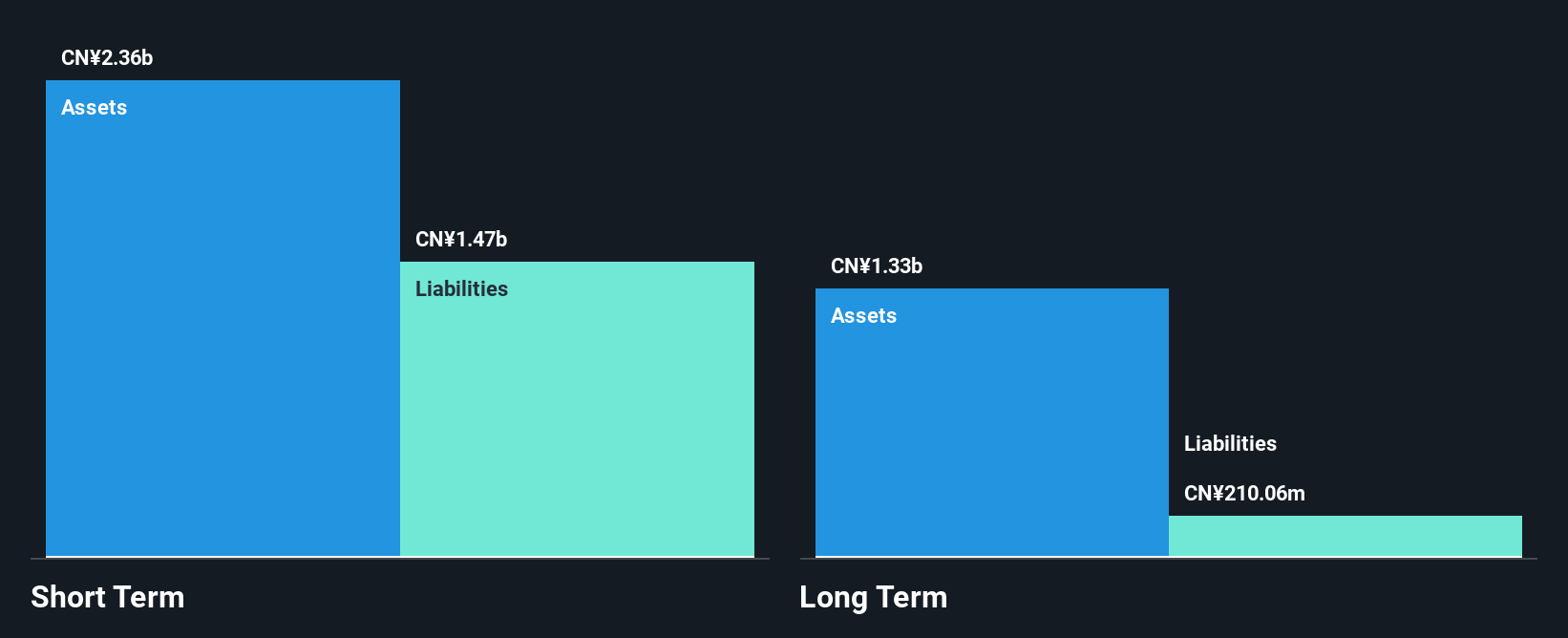

Cosmo Lady (China) Holdings demonstrates financial stability with CN¥2.4 billion in short-term assets surpassing both its short and long-term liabilities, and more cash than total debt. The company reported a net income increase to CN¥126.16 million for 2024, reflecting improved profit margins of 4.2%. Earnings growth of 197% last year outpaced the luxury industry significantly, indicating robust performance despite low return on equity at 5.7%. Recent dividend affirmation suggests some commitment to shareholder returns, though the track record is unstable. The management team and board are experienced, contributing to strategic consistency amidst market volatility.

- Click here and access our complete financial health analysis report to understand the dynamics of Cosmo Lady (China) Holdings.

- Review our historical performance report to gain insights into Cosmo Lady (China) Holdings' track record.

Novautek Technologies Group (SEHK:519)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Novautek Technologies Group Limited (SEHK:519) is an investment holding company involved in resort and property development, as well as property investment in the People’s Republic of China and Hong Kong, with a market cap of approximately HK$381.89 million.

Operations: The company's revenue is primarily derived from property development (HK$18.19 billion) and property investment (HK$10.04 billion), with a smaller contribution from investment holding (HK$6.95 million).

Market Cap: HK$381.89M

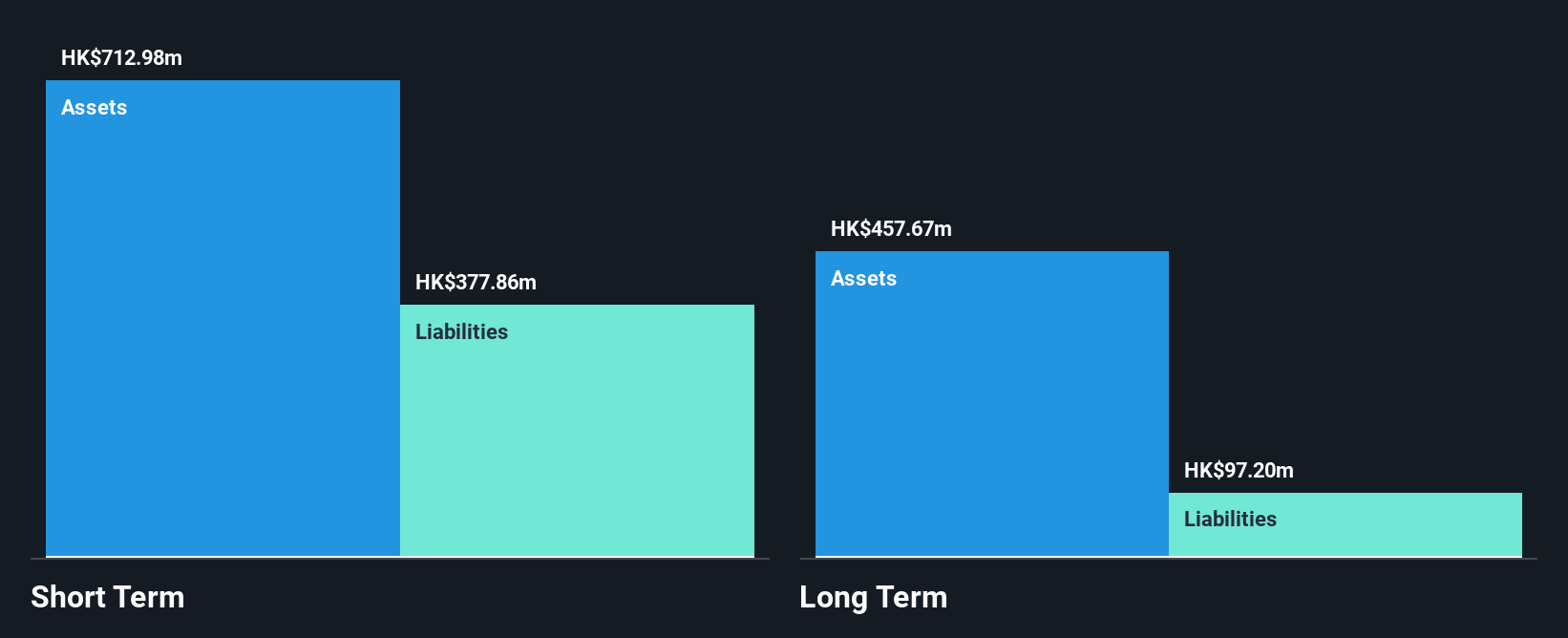

Novautek Technologies Group Limited is navigating financial challenges as it remains unprofitable, though it has reduced losses by 28.3% annually over the past five years. The company's debt to equity ratio increased slightly, yet its net debt level is satisfactory at 10.2%. Despite volatility in share price and a lack of meaningful revenue (HK$36M), Novautek's short-term assets cover both short and long-term liabilities comfortably. The management team demonstrates experience with an average tenure of 4.8 years, although the board lacks similar depth with only 1.4 years on average, indicating recent changes in leadership structure.

- Unlock comprehensive insights into our analysis of Novautek Technologies Group stock in this financial health report.

- Understand Novautek Technologies Group's track record by examining our performance history report.

Bestsun Energy (SHSE:600681)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Bestsun Energy Co., Ltd. operates in the city gas business and has a market capitalization of CN¥4.71 billion.

Operations: The company's revenue is derived entirely from its operations in China, totaling CN¥5.13 billion.

Market Cap: CN¥4.71B

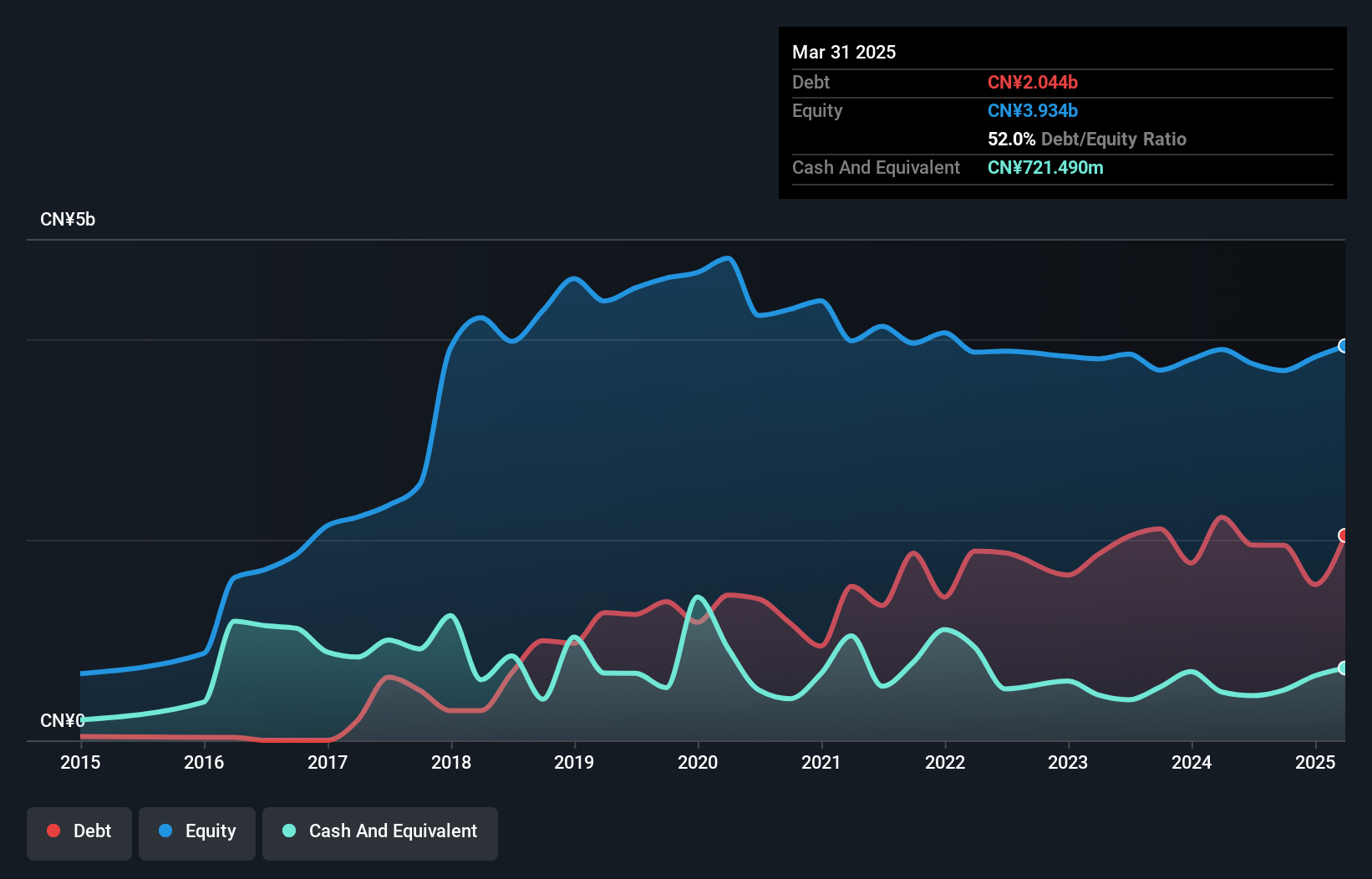

Bestsun Energy Co., Ltd. has shown financial resilience with a recent earnings growth of 16.3%, outpacing the gas utilities industry. Despite a decline in profits over five years, its net profit margin improved to 6.5% from last year’s 5.3%. The company's debt is well managed with adequate cash flow coverage and satisfactory net debt to equity ratio at 33.6%. However, short-term liabilities exceed short-term assets by CN¥1.1 billion, indicating potential liquidity concerns. While trading below estimated fair value, dividend sustainability remains questionable as it is not well covered by earnings despite a yield of 6.6%.

- Jump into the full analysis health report here for a deeper understanding of Bestsun Energy.

- Examine Bestsun Energy's past performance report to understand how it has performed in prior years.

Seize The Opportunity

- Gain an insight into the universe of 5,630 Global Penny Stocks by clicking here.

- Searching for a Fresh Perspective? AI is about to change healthcare. These 22 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bestsun Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:600681

Good value with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|37.6% undervalued

TR

Community Contributor