3 Growth Companies With High Insider Ownership Growing Revenues Up To 44%

Reviewed by Simply Wall St

In the wake of a significant "red sweep" in the U.S. elections, global markets have been buoyed by investor optimism about potential growth and tax reforms, with major indices like the S&P 500 and Nasdaq Composite reaching record highs. Amid these developments, investors are increasingly focusing on growth companies with high insider ownership, as such stocks often reflect strong confidence from those who know the company best and can potentially capitalize on favorable market conditions.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| People & Technology (KOSDAQ:A137400) | 16.4% | 36.6% |

| Medley (TSE:4480) | 34% | 30.4% |

| Pharma Mar (BME:PHM) | 11.8% | 56.4% |

| Findi (ASX:FND) | 34.8% | 64.8% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| Alkami Technology (NasdaqGS:ALKT) | 11.2% | 98.6% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.6% |

We'll examine a selection from our screener results.

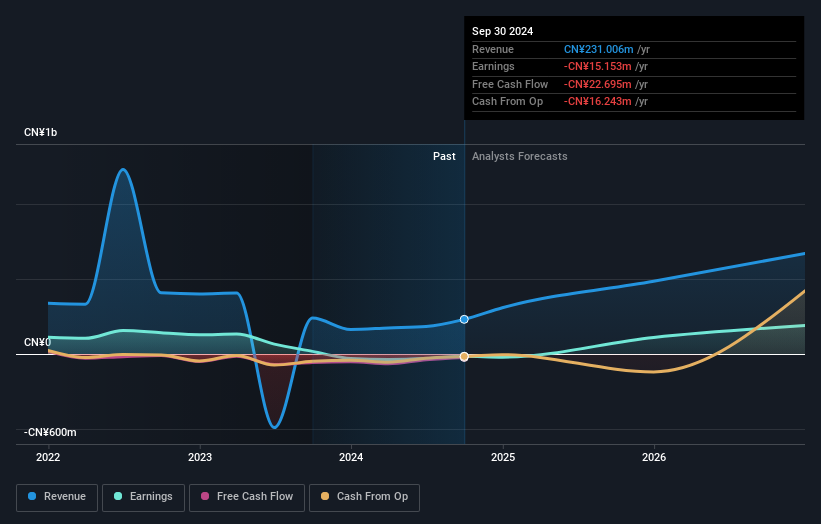

Hunan Kylinsec Technology (SHSE:688152)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hunan Kylinsec Technology Co., Ltd. is a company that supplies software products, with a market cap of CN¥6.63 billion.

Operations: The company's revenue segments are not specified in the provided text.

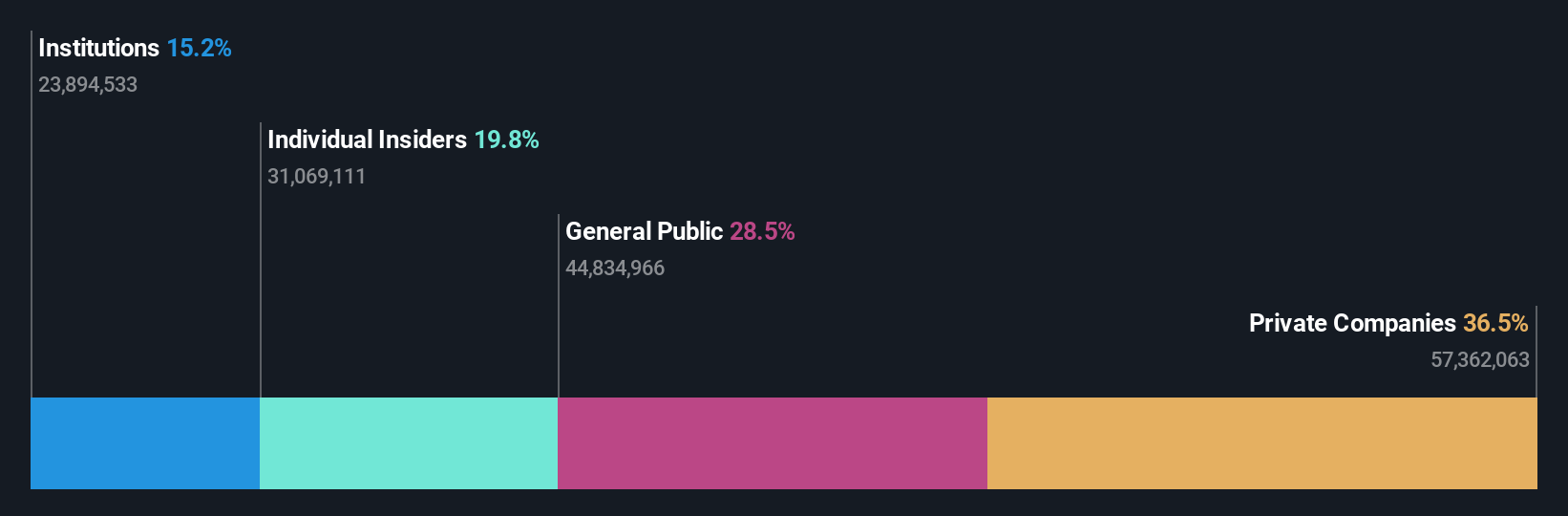

Insider Ownership: 38.3%

Revenue Growth Forecast: 44.9% p.a.

Hunan Kylinsec Technology shows promising growth potential, with revenue expected to increase at 44.9% annually, outpacing the broader Chinese market. Recent earnings reveal a narrowing net loss of CNY 22.94 million for the first nine months of 2024, down from CNY 37.9 million a year prior, indicating improved financial health. Despite its volatile share price and low forecasted return on equity, it is anticipated to achieve profitability within three years without significant insider trading activity recently reported.

- Unlock comprehensive insights into our analysis of Hunan Kylinsec Technology stock in this growth report.

- Our valuation report unveils the possibility Hunan Kylinsec Technology's shares may be trading at a premium.

Wuxi Taclink Optoelectronics Technology (SHSE:688205)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Wuxi Taclink Optoelectronics Technology Co., Ltd. operates in the optoelectronics industry and has a market cap of CN¥9.38 billion.

Operations: Unfortunately, the revenue segment details for Wuxi Taclink Optoelectronics Technology Co., Ltd. are not provided in the text you shared. Please provide the specific revenue segment information for further assistance.

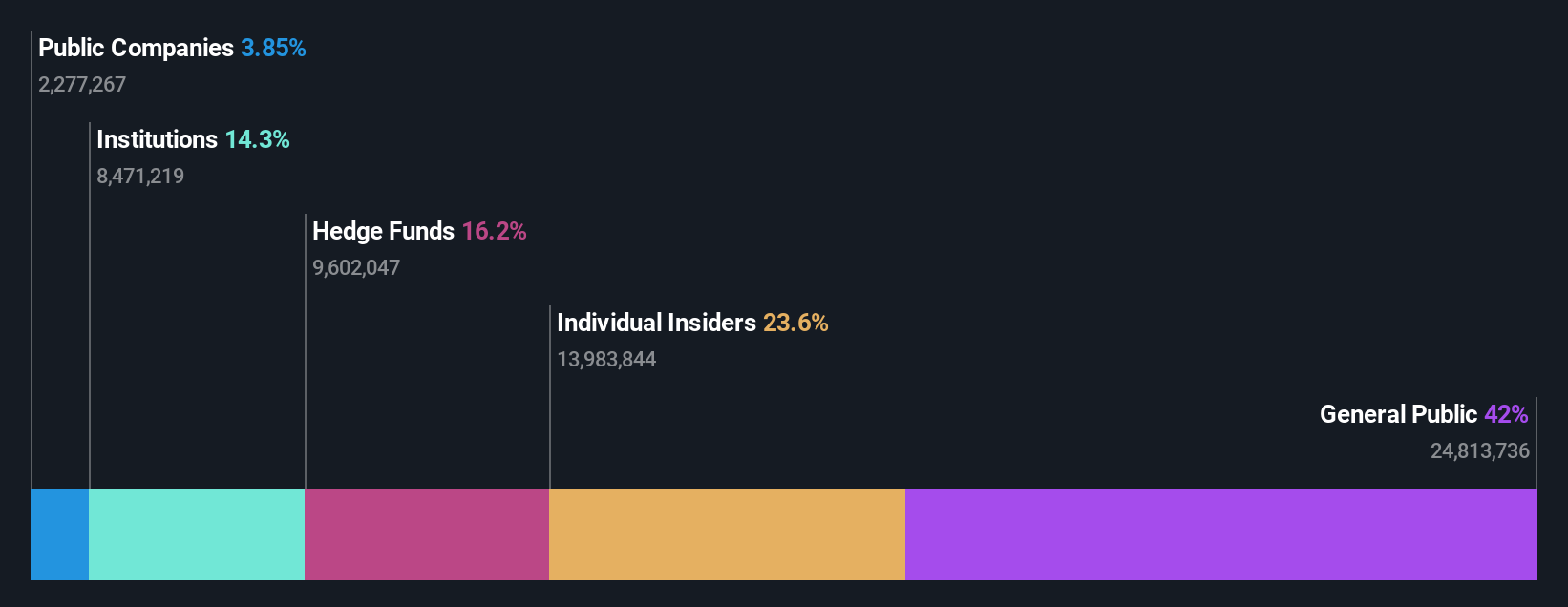

Insider Ownership: 19.8%

Revenue Growth Forecast: 23.4% p.a.

Wuxi Taclink Optoelectronics Technology is poised for substantial growth, with revenue and earnings projected to outpace the Chinese market at 23.4% and 33.1% annually, respectively. Recent earnings show an increase in net income to CNY 76.29 million from CNY 66.32 million year-over-year, reflecting strong operational performance despite a volatile share price. The company was recently added to the S&P Global BMI Index but lacks recent insider trading activity that could signal confidence or concern among insiders.

- Dive into the specifics of Wuxi Taclink Optoelectronics Technology here with our thorough growth forecast report.

- Our valuation report here indicates Wuxi Taclink Optoelectronics Technology may be overvalued.

freee K.K (TSE:4478)

Simply Wall St Growth Rating: ★★★★★☆

Overview: freee K.K. provides cloud-based accounting and HR software solutions in Japan, with a market cap of ¥176.74 billion.

Operations: The company generates revenue primarily from its Platform Business segment, which accounted for ¥25.43 billion.

Insider Ownership: 23.8%

Revenue Growth Forecast: 18.2% p.a.

freee K.K. is set for notable growth, with revenue projected to increase at 18.2% annually, outpacing the Japanese market. The company anticipates net sales of ¥33.06 billion for fiscal 2025 and aims to become profitable within three years, which is above average market growth. Recent leadership changes include Yasuhiro Kimura stepping in as CPO, potentially enhancing strategic direction despite a volatile share price and no recent insider trading activity signaling confidence or concern among insiders.

- Click here to discover the nuances of freee K.K with our detailed analytical future growth report.

- Upon reviewing our latest valuation report, freee K.K's share price might be too pessimistic.

Next Steps

- Unlock our comprehensive list of 1528 Fast Growing Companies With High Insider Ownership by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hunan Kylinsec Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688152

Flawless balance sheet with high growth potential.