Advertisement

- China

- /

- Semiconductors

- /

- SZSE:300373

Yangzhou Yangjie Electronic Technology Co., Ltd. Just Recorded A 8.4% EPS Beat: Here's What Analysts Are Forecasting Next

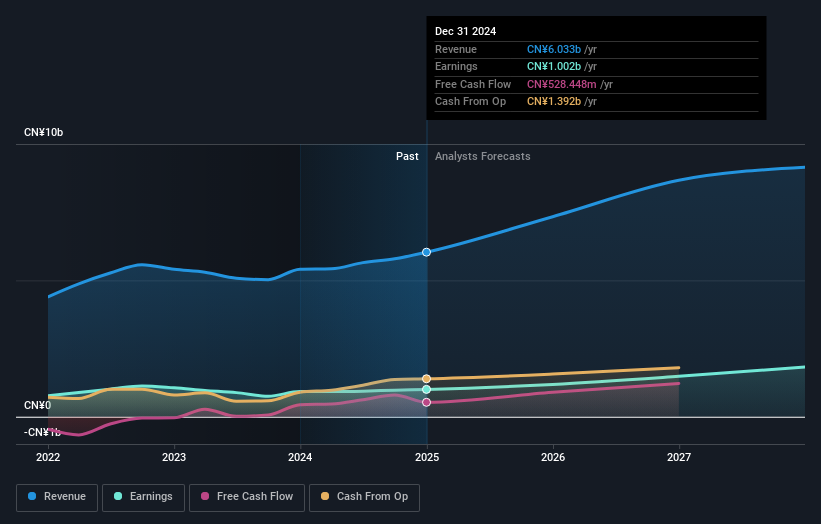

Yangzhou Yangjie Electronic Technology Co., Ltd. (SZSE:300373) shareholders are probably feeling a little disappointed, since its shares fell 7.1% to CN¥46.36 in the week after its latest full-year results. Yangzhou Yangjie Electronic Technology reported CN¥6.0b in revenue, roughly in line with analyst forecasts, although statutory earnings per share (EPS) of CN¥1.85 beat expectations, being 8.4% higher than what the analysts expected. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Following the latest results, Yangzhou Yangjie Electronic Technology's five analysts are now forecasting revenues of CN¥7.33b in 2025. This would be a substantial 22% improvement in revenue compared to the last 12 months. Per-share earnings are expected to swell 18% to CN¥2.18. Yet prior to the latest earnings, the analysts had been anticipated revenues of CN¥7.44b and earnings per share (EPS) of CN¥2.18 in 2025. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

See our latest analysis for Yangzhou Yangjie Electronic Technology

The analysts reconfirmed their price target of CN¥48.80, showing that the business is executing well and in line with expectations. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Yangzhou Yangjie Electronic Technology, with the most bullish analyst valuing it at CN¥58.00 and the most bearish at CN¥43.40 per share. This is a very narrow spread of estimates, implying either that Yangzhou Yangjie Electronic Technology is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 22% growth on an annualised basis. That is in line with its 19% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 24% annually. So although Yangzhou Yangjie Electronic Technology is expected to maintain its revenue growth rate, it's only growing at about the rate of the wider industry.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have forecasts for Yangzhou Yangjie Electronic Technology going out to 2027, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 1 warning sign for Yangzhou Yangjie Electronic Technology that you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300373

Yangzhou Yangjie Electronic Technology

Yangzhou Yangjie Electronic Technology Co., Ltd.

Undervalued with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor