- China

- /

- Semiconductors

- /

- SHSE:688496

There's Reason For Concern Over Suzhou QingYue Optoelectronics Technology Co., Ltd.'s (SHSE:688496) Massive 27% Price Jump

Suzhou QingYue Optoelectronics Technology Co., Ltd. (SHSE:688496) shareholders are no doubt pleased to see that the share price has bounced 27% in the last month, although it is still struggling to make up recently lost ground. The last 30 days bring the annual gain to a very sharp 32%.

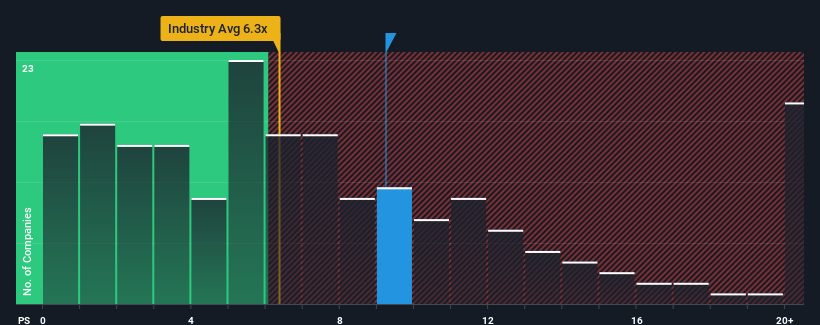

After such a large jump in price, Suzhou QingYue Optoelectronics Technology may be sending bearish signals at the moment with its price-to-sales (or "P/S") ratio of 9.2x, since almost half of all companies in the Semiconductor in China have P/S ratios under 6.3x and even P/S lower than 3x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

View our latest analysis for Suzhou QingYue Optoelectronics Technology

What Does Suzhou QingYue Optoelectronics Technology's Recent Performance Look Like?

For instance, Suzhou QingYue Optoelectronics Technology's receding revenue in recent times would have to be some food for thought. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Suzhou QingYue Optoelectronics Technology will help you shine a light on its historical performance.What Are Revenue Growth Metrics Telling Us About The High P/S?

Suzhou QingYue Optoelectronics Technology's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Retrospectively, the last year delivered a frustrating 36% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 34% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 37% shows it's noticeably less attractive.

With this in mind, we find it worrying that Suzhou QingYue Optoelectronics Technology's P/S exceeds that of its industry peers. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

What Does Suzhou QingYue Optoelectronics Technology's P/S Mean For Investors?

Suzhou QingYue Optoelectronics Technology's P/S is on the rise since its shares have risen strongly. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Suzhou QingYue Optoelectronics Technology revealed its poor three-year revenue trends aren't detracting from the P/S as much as we though, given they look worse than current industry expectations. When we see slower than industry revenue growth but an elevated P/S, there's considerable risk of the share price declining, sending the P/S lower. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

You should always think about risks. Case in point, we've spotted 2 warning signs for Suzhou QingYue Optoelectronics Technology you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688496

Suzhou QingYue Optoelectronics Technology

Suzhou QingYue Optoelectronics Technology Co., Ltd.

Excellent balance sheet and slightly overvalued.

Market Insights

Community Narratives