Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688368

Little Excitement Around Shanghai Bright Power Semiconductor Co., Ltd.'s (SHSE:688368) Revenues

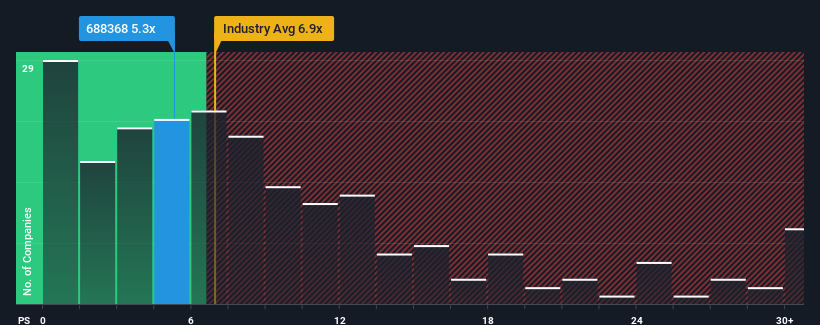

Shanghai Bright Power Semiconductor Co., Ltd.'s (SHSE:688368) price-to-sales (or "P/S") ratio of 5.3x might make it look like a buy right now compared to the Semiconductor industry in China, where around half of the companies have P/S ratios above 6.9x and even P/S above 12x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

Check out our latest analysis for Shanghai Bright Power Semiconductor

What Does Shanghai Bright Power Semiconductor's P/S Mean For Shareholders?

Recent times have been advantageous for Shanghai Bright Power Semiconductor as its revenues have been rising faster than most other companies. It might be that many expect the strong revenue performance to degrade substantially, which has repressed the share price, and thus the P/S ratio. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Keen to find out how analysts think Shanghai Bright Power Semiconductor's future stacks up against the industry? In that case, our free report is a great place to start.Is There Any Revenue Growth Forecasted For Shanghai Bright Power Semiconductor?

Shanghai Bright Power Semiconductor's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 24% last year. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 34% overall. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to climb by 31% during the coming year according to the two analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 49%, which is noticeably more attractive.

With this in consideration, its clear as to why Shanghai Bright Power Semiconductor's P/S is falling short industry peers. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As expected, our analysis of Shanghai Bright Power Semiconductor's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

You always need to take note of risks, for example - Shanghai Bright Power Semiconductor has 1 warning sign we think you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688368

Shanghai Bright Power Semiconductor

Engages in the research, development, and sale of power management and motor control chips in China and internationally.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor