Advertisement

- China

- /

- Semiconductors

- /

- SHSE:600667

Wuxi Taiji Industry Limited Corporation (SHSE:600667) Surges 33% Yet Its Low P/S Is No Reason For Excitement

Those holding Wuxi Taiji Industry Limited Corporation (SHSE:600667) shares would be relieved that the share price has rebounded 33% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Looking further back, the 12% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

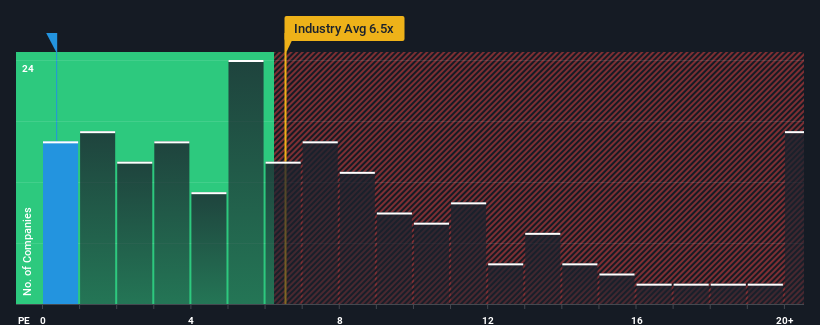

In spite of the firm bounce in price, Wuxi Taiji Industry Limited may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 0.4x, since almost half of all companies in the Semiconductor industry in China have P/S ratios greater than 6.5x and even P/S higher than 12x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

Check out our latest analysis for Wuxi Taiji Industry Limited

What Does Wuxi Taiji Industry Limited's Recent Performance Look Like?

There hasn't been much to differentiate Wuxi Taiji Industry Limited's and the industry's revenue growth lately. It might be that many expect the mediocre revenue performance to degrade, which has repressed the P/S ratio. Those who are bullish on Wuxi Taiji Industry Limited will be hoping that this isn't the case.

Want the full picture on analyst estimates for the company? Then our free report on Wuxi Taiji Industry Limited will help you uncover what's on the horizon.How Is Wuxi Taiji Industry Limited's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as depressed as Wuxi Taiji Industry Limited's is when the company's growth is on track to lag the industry decidedly.

If we review the last year of revenue growth, the company posted a terrific increase of 20%. The latest three year period has also seen an excellent 123% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Shifting to the future, estimates from the one analyst covering the company suggest revenue should grow by 25% over the next year. That's shaping up to be materially lower than the 37% growth forecast for the broader industry.

In light of this, it's understandable that Wuxi Taiji Industry Limited's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

Wuxi Taiji Industry Limited's recent share price jump still sees fails to bring its P/S alongside the industry median. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Wuxi Taiji Industry Limited maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Wuxi Taiji Industry Limited with six simple checks.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Wuxi Taiji Industry Limited might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600667

Wuxi Taiji Industry Limited

Primarily engages in the semiconductor packaging and testing business.

Flawless balance sheet with high growth potential and pays a dividend.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.1% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|22.0% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.6% undervalued

RO

Community Contributor