- China

- /

- Real Estate

- /

- SZSE:001979

Does China Merchants Shekou Industrial Zone Holdings (SZSE:001979) Have A Healthy Balance Sheet?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies China Merchants Shekou Industrial Zone Holdings Co., Ltd. (SZSE:001979) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for China Merchants Shekou Industrial Zone Holdings

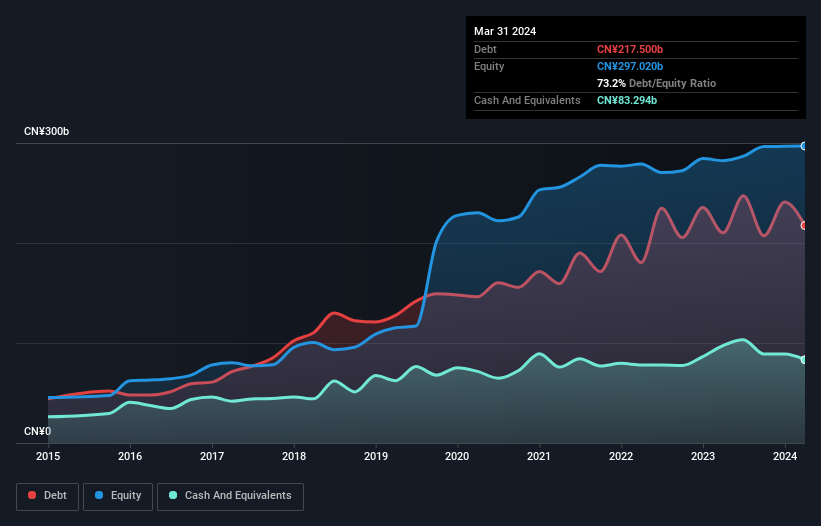

How Much Debt Does China Merchants Shekou Industrial Zone Holdings Carry?

The chart below, which you can click on for greater detail, shows that China Merchants Shekou Industrial Zone Holdings had CN¥217.5b in debt in March 2024; about the same as the year before. On the flip side, it has CN¥83.3b in cash leading to net debt of about CN¥134.2b.

How Healthy Is China Merchants Shekou Industrial Zone Holdings' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that China Merchants Shekou Industrial Zone Holdings had liabilities of CN¥430.3b due within 12 months and liabilities of CN¥192.5b due beyond that. On the other hand, it had cash of CN¥83.3b and CN¥125.0b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥414.5b.

This deficit casts a shadow over the CN¥89.7b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, China Merchants Shekou Industrial Zone Holdings would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

As it happens China Merchants Shekou Industrial Zone Holdings has a fairly concerning net debt to EBITDA ratio of 8.1 but very strong interest coverage of 1k. So either it has access to very cheap long term debt or that interest expense is going to grow! Unfortunately, China Merchants Shekou Industrial Zone Holdings's EBIT flopped 14% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine China Merchants Shekou Industrial Zone Holdings's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. In the last three years, China Merchants Shekou Industrial Zone Holdings created free cash flow amounting to 19% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

To be frank both China Merchants Shekou Industrial Zone Holdings's net debt to EBITDA and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But on the bright side, its interest cover is a good sign, and makes us more optimistic. Taking into account all the aforementioned factors, it looks like China Merchants Shekou Industrial Zone Holdings has too much debt. That sort of riskiness is ok for some, but it certainly doesn't float our boat. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for China Merchants Shekou Industrial Zone Holdings (1 doesn't sit too well with us!) that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:001979

China Merchants Shekou Industrial Zone Holdings

Develops and sells residential properties in China and internationally.

Average dividend payer and fair value.

Similar Companies

Market Insights

Community Narratives