- China

- /

- Life Sciences

- /

- SZSE:300030

Improve Medical Instruments Co., Ltd. (SZSE:300030) Held Back By Insufficient Growth Even After Shares Climb 46%

The Improve Medical Instruments Co., Ltd. (SZSE:300030) share price has done very well over the last month, posting an excellent gain of 46%. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 23% over that time.

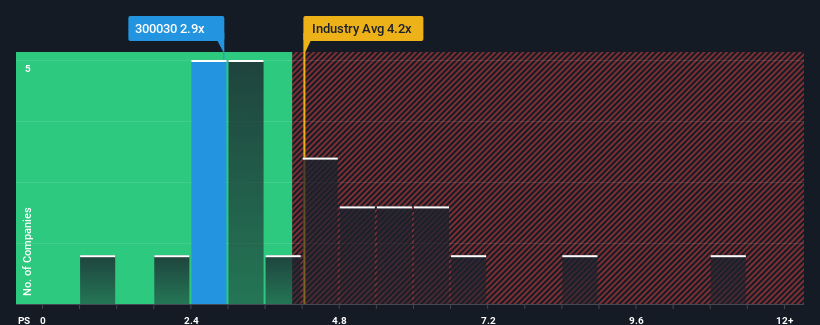

Even after such a large jump in price, it would still be understandable if you think Improve Medical Instruments is a stock with good investment prospects with a price-to-sales ratios (or "P/S") of 2.9x, considering almost half the companies in China's Life Sciences industry have P/S ratios above 4.2x. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Improve Medical Instruments

What Does Improve Medical Instruments' P/S Mean For Shareholders?

For instance, Improve Medical Instruments' receding revenue in recent times would have to be some food for thought. It might be that many expect the disappointing revenue performance to continue or accelerate, which has repressed the P/S. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

Although there are no analyst estimates available for Improve Medical Instruments, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is Improve Medical Instruments' Revenue Growth Trending?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Improve Medical Instruments' to be considered reasonable.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 8.9%. The last three years don't look nice either as the company has shrunk revenue by 34% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

In contrast to the company, the rest of the industry is expected to grow by 16% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

In light of this, it's understandable that Improve Medical Instruments' P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Key Takeaway

The latest share price surge wasn't enough to lift Improve Medical Instruments' P/S close to the industry median. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Improve Medical Instruments revealed its shrinking revenue over the medium-term is contributing to its low P/S, given the industry is set to grow. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. If recent medium-term revenue trends continue, it's hard to see the share price moving strongly in either direction in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 2 warning signs for Improve Medical Instruments you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300030

Improve Medical Instruments

Engages in the provision of relevant technologies, products, and services for clinical laboratory and clinical nursing in China and internationally.

Flawless balance sheet and slightly overvalued.

Market Insights

Community Narratives