Advertisement

Subdued Growth No Barrier To Chongqing Lummy Pharmaceutical Co., Ltd. (SZSE:300006) With Shares Advancing 32%

Despite an already strong run, Chongqing Lummy Pharmaceutical Co., Ltd. (SZSE:300006) shares have been powering on, with a gain of 32% in the last thirty days. Taking a wider view, although not as strong as the last month, the full year gain of 24% is also fairly reasonable.

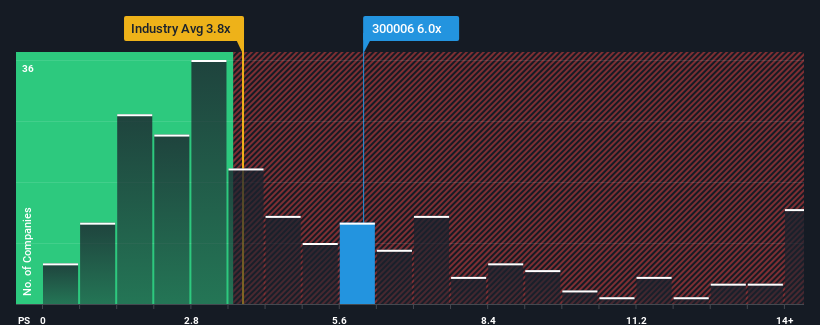

Following the firm bounce in price, you could be forgiven for thinking Chongqing Lummy Pharmaceutical is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 6x, considering almost half the companies in China's Pharmaceuticals industry have P/S ratios below 3.8x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Chongqing Lummy Pharmaceutical

What Does Chongqing Lummy Pharmaceutical's Recent Performance Look Like?

It looks like revenue growth has deserted Chongqing Lummy Pharmaceutical recently, which is not something to boast about. One possibility is that the P/S is high because investors think the benign revenue growth will improve to outperform the broader industry in the near future. However, if this isn't the case, investors might get caught out paying too much for the stock.

Although there are no analyst estimates available for Chongqing Lummy Pharmaceutical, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is Chongqing Lummy Pharmaceutical's Revenue Growth Trending?

In order to justify its P/S ratio, Chongqing Lummy Pharmaceutical would need to produce outstanding growth that's well in excess of the industry.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. Whilst it's an improvement, it wasn't enough to get the company out of the hole it was in, with revenue down 39% overall from three years ago. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

In contrast to the company, the rest of the industry is expected to grow by 226% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

In light of this, it's alarming that Chongqing Lummy Pharmaceutical's P/S sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

What Does Chongqing Lummy Pharmaceutical's P/S Mean For Investors?

Shares in Chongqing Lummy Pharmaceutical have seen a strong upwards swing lately, which has really helped boost its P/S figure. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our examination of Chongqing Lummy Pharmaceutical revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. With a revenue decline on investors' minds, the likelihood of a souring sentiment is quite high which could send the P/S back in line with what we'd expect. Unless the the circumstances surrounding the recent medium-term improve, it wouldn't be wrong to expect a a difficult period ahead for the company's shareholders.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Chongqing Lummy Pharmaceutical that you should be aware of.

If you're unsure about the strength of Chongqing Lummy Pharmaceutical's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300006

Chongqing Lummy Pharmaceutical

Engages in the research and development, manufacture, and sale of pharmaceutical products in China.

Flawless balance sheet and overvalued.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor