Advertisement

Beijing Kawin Technology Share-Holding Co., Ltd. (SHSE:688687) Stocks Shoot Up 25% But Its P/E Still Looks Reasonable

Those holding Beijing Kawin Technology Share-Holding Co., Ltd. (SHSE:688687) shares would be relieved that the share price has rebounded 25% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Taking a wider view, although not as strong as the last month, the full year gain of 12% is also fairly reasonable.

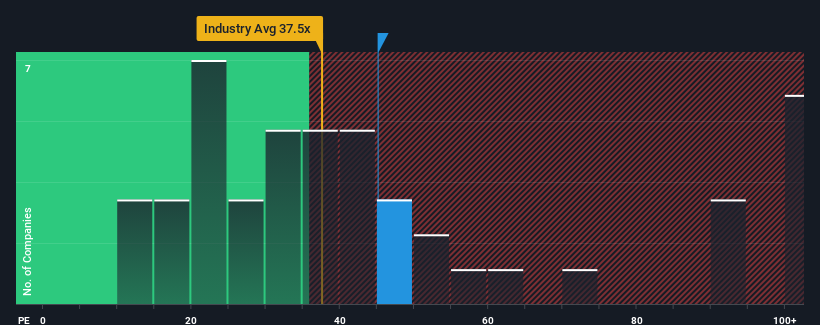

Following the firm bounce in price, Beijing Kawin Technology Share-Holding may be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 45.1x, since almost half of all companies in China have P/E ratios under 31x and even P/E's lower than 18x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Beijing Kawin Technology Share-Holding certainly has been doing a good job lately as it's been growing earnings more than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Beijing Kawin Technology Share-Holding

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as high as Beijing Kawin Technology Share-Holding's is when the company's growth is on track to outshine the market.

If we review the last year of earnings growth, the company posted a terrific increase of 41%. EPS has also lifted 18% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 46% as estimated by the four analysts watching the company. That's shaping up to be materially higher than the 41% growth forecast for the broader market.

In light of this, it's understandable that Beijing Kawin Technology Share-Holding's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

Beijing Kawin Technology Share-Holding's P/E is getting right up there since its shares have risen strongly. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Beijing Kawin Technology Share-Holding's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

It is also worth noting that we have found 1 warning sign for Beijing Kawin Technology Share-Holding that you need to take into consideration.

Of course, you might also be able to find a better stock than Beijing Kawin Technology Share-Holding. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Kawin Technology Share-Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688687

Beijing Kawin Technology Share-Holding

A biopharmaceutical company, provides treatment solutions for viral and immune diseases in China.

Undervalued with solid track record.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor