Advertisement

Changchun BCHT Biotechnology Co. (SHSE:688276) Shares Slammed 25% But Getting In Cheap Might Be Difficult Regardless

Changchun BCHT Biotechnology Co. (SHSE:688276) shareholders that were waiting for something to happen have been dealt a blow with a 25% share price drop in the last month. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 37% share price drop.

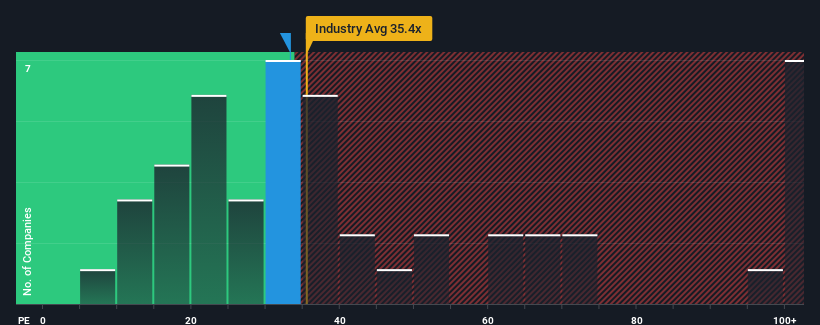

Although its price has dipped substantially, given around half the companies in China have price-to-earnings ratios (or "P/E's") below 29x, you may still consider Changchun BCHT Biotechnology as a stock to potentially avoid with its 33.3x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Recent times have been advantageous for Changchun BCHT Biotechnology as its earnings have been rising faster than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

See our latest analysis for Changchun BCHT Biotechnology

How Is Changchun BCHT Biotechnology's Growth Trending?

There's an inherent assumption that a company should outperform the market for P/E ratios like Changchun BCHT Biotechnology's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 175% gain to the company's bottom line. The latest three year period has also seen a 6.5% overall rise in EPS, aided extensively by its short-term performance. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 33% each year during the coming three years according to the six analysts following the company. With the market only predicted to deliver 21% each year, the company is positioned for a stronger earnings result.

With this information, we can see why Changchun BCHT Biotechnology is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

There's still some solid strength behind Changchun BCHT Biotechnology's P/E, if not its share price lately. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Changchun BCHT Biotechnology's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 1 warning sign for Changchun BCHT Biotechnology that you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688276

Changchun BCHT Biotechnology

Changchun BCHT Biotechnology Co. Ltd., a biopharmaceutical company, engages in the research and development, production, and sale of human vaccines in China and internationally.

Flawless balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor