When it comes to investing, there are some useful financial metrics that can warn us when a business is potentially in trouble. More often than not, we'll see a declining return on capital employed (ROCE) and a declining amount of capital employed. Ultimately this means that the company is earning less per dollar invested and on top of that, it's shrinking its base of capital employed. And from a first read, things don't look too good at China Film (SHSE:600977), so let's see why.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for China Film:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.0099 = CN¥135m ÷ (CN¥20b - CN¥6.6b) (Based on the trailing twelve months to September 2023).

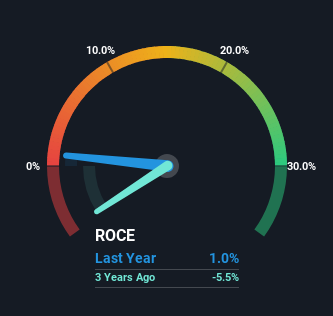

Therefore, China Film has an ROCE of 1.0%. Ultimately, that's a low return and it under-performs the Entertainment industry average of 4.5%.

See our latest analysis for China Film

In the above chart we have measured China Film's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for China Film .

What The Trend Of ROCE Can Tell Us

There is reason to be cautious about China Film, given the returns are trending downwards. Unfortunately the returns on capital have diminished from the 9.4% that they were earning five years ago. On top of that, it's worth noting that the amount of capital employed within the business has remained relatively steady. This combination can be indicative of a mature business that still has areas to deploy capital, but the returns received aren't as high due potentially to new competition or smaller margins. If these trends continue, we wouldn't expect China Film to turn into a multi-bagger.

The Key Takeaway

In summary, it's unfortunate that China Film is generating lower returns from the same amount of capital. Long term shareholders who've owned the stock over the last five years have experienced a 37% depreciation in their investment, so it appears the market might not like these trends either. With underlying trends that aren't great in these areas, we'd consider looking elsewhere.

On a final note, we've found 1 warning sign for China Film that we think you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600977

China Film

Engages in the production, distribution, projection, technology, service, and innovation of films and television dramas in China and internationally.

Moderate growth potential with mediocre balance sheet.

Market Insights

Community Narratives