Why Investors Shouldn't Be Surprised By Jiangsu Nata Opto-electronic Material Co., Ltd.'s (SZSE:300346) 36% Share Price Surge

Jiangsu Nata Opto-electronic Material Co., Ltd. (SZSE:300346) shareholders are no doubt pleased to see that the share price has bounced 36% in the last month, although it is still struggling to make up recently lost ground. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 16% over that time.

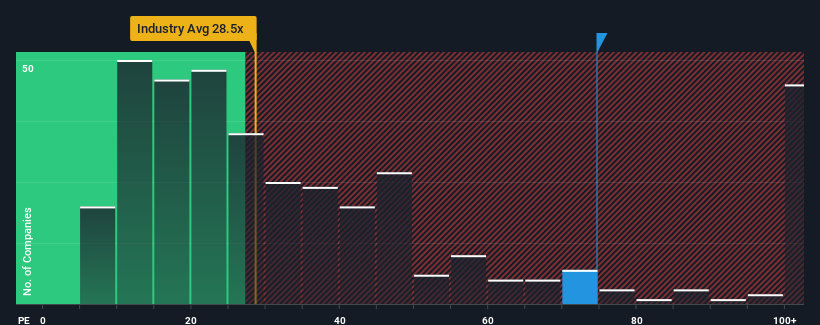

Following the firm bounce in price, given close to half the companies in China have price-to-earnings ratios (or "P/E's") below 30x, you may consider Jiangsu Nata Opto-electronic Material as a stock to avoid entirely with its 74.6x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

With earnings that are retreating more than the market's of late, Jiangsu Nata Opto-electronic Material has been very sluggish. It might be that many expect the dismal earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Jiangsu Nata Opto-electronic Material

Is There Enough Growth For Jiangsu Nata Opto-electronic Material?

The only time you'd be truly comfortable seeing a P/E as steep as Jiangsu Nata Opto-electronic Material's is when the company's growth is on track to outshine the market decidedly.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 16%. Even so, admirably EPS has lifted 79% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 61% during the coming year according to the three analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 42%, which is noticeably less attractive.

In light of this, it's understandable that Jiangsu Nata Opto-electronic Material's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Jiangsu Nata Opto-electronic Material's P/E?

Shares in Jiangsu Nata Opto-electronic Material have built up some good momentum lately, which has really inflated its P/E. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Jiangsu Nata Opto-electronic Material's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Jiangsu Nata Opto-electronic Material you should know about.

You might be able to find a better investment than Jiangsu Nata Opto-electronic Material. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300346

Jiangsu Nata Opto-electronic Material

Jiangsu Nata Opto-electronic Material Co., Ltd.

Reasonable growth potential with adequate balance sheet.