Advertisement

- China

- /

- Healthtech

- /

- SHSE:688246

3 Growth Stocks With High Insider Ownership And Up To 104% Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

As global markets react to easing inflation and strong bank earnings, major U.S. stock indexes have rebounded, with value stocks outpacing growth shares amid sector-specific shifts. In this environment, identifying growth companies with high insider ownership can be particularly compelling, as it often signals confidence from those closest to the business in its long-term potential and resilience amidst fluctuating market conditions.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.8% | 38.9% |

| CD Projekt (WSE:CDR) | 29.7% | 30.6% |

| Pharma Mar (BME:PHM) | 11.9% | 55.1% |

| Waystream Holding (OM:WAYS) | 11.3% | 113.3% |

| On Holding (NYSE:ONON) | 19.1% | 29.8% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 135% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

Here we highlight a subset of our preferred stocks from the screener.

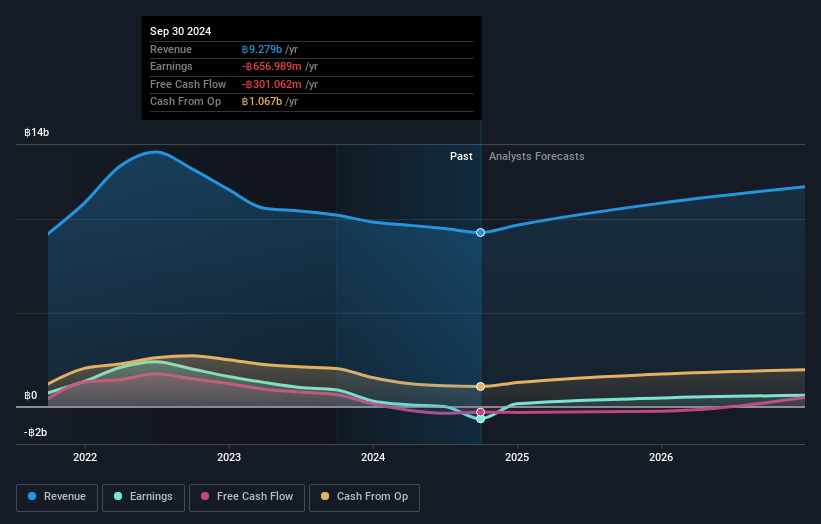

Thonburi Healthcare Group (SET:THG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Thonburi Healthcare Group Public Company Limited, along with its subsidiaries, operates private hospitals in Thailand and has a market cap of THB11.27 billion.

Operations: The company generates revenue primarily from Hospital Operations (THB8.19 billion), followed by Hospital Management (THB764.61 million), Healthcare Solution Provider (THB427.75 million), and Development and Sales of Hospital Operation Software (THB36 million).

Insider Ownership: 33.1%

Earnings Growth Forecast: 104.5% p.a.

Thonburi Healthcare Group faces challenges with recent executive changes and a net loss for the third quarter of 2024, despite trading at a significant discount to its estimated fair value. Its revenue is forecast to grow faster than the Thai market but remains below 20% annually. The company is expected to become profitable within three years, though its return on equity is projected to remain low, and current debt levels are not well covered by operating cash flow.

- Click to explore a detailed breakdown of our findings in Thonburi Healthcare Group's earnings growth report.

- The analysis detailed in our Thonburi Healthcare Group valuation report hints at an deflated share price compared to its estimated value.

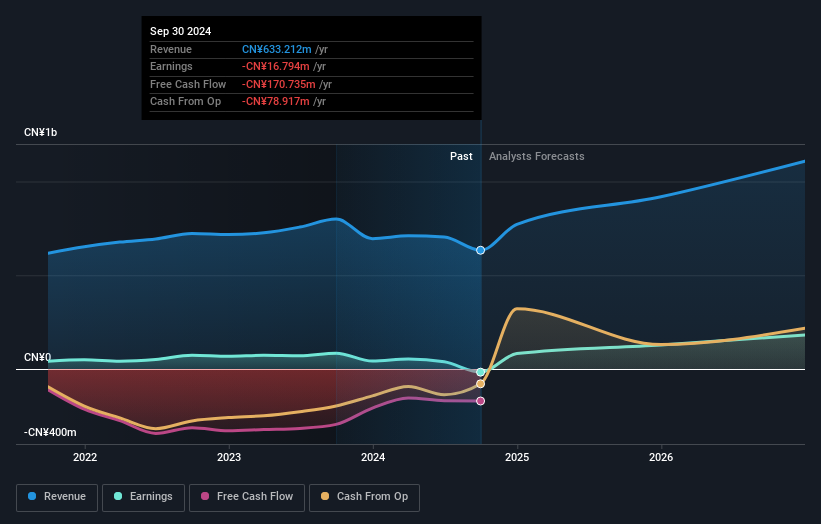

Goodwill E-Health Info (SHSE:688246)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Goodwill E-Health Info Co., Ltd. focuses on the research and development of medical information software in China, with a market cap of CN¥3.30 billion.

Operations: Revenue Segments (in millions of CN¥): [No specific revenue segments provided in the text.]

Insider Ownership: 20.3%

Earnings Growth Forecast: 73.2% p.a.

Goodwill E-Health Info forecasts robust revenue growth of 22.7% annually, outpacing the CN market's 13.4%, and is expected to become profitable within three years. However, recent financials reveal a net loss of CNY 41.26 million for the first nine months of 2024, contrasting with a net income in the previous year. The company's return on equity is projected to be low at 7.1%, and its share price has been highly volatile recently.

- Navigate through the intricacies of Goodwill E-Health Info with our comprehensive analyst estimates report here.

- Our valuation report here indicates Goodwill E-Health Info may be overvalued.

COLTENE Holding (SWX:CLTN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: COLTENE Holding AG is a company that develops, manufactures, and sells dental disposables, tools, and equipment across various regions including Europe, the Middle East, Africa, North America, Latin America, and Asia/Oceania with a market cap of CHF320.28 million.

Operations: The company's revenue from disposables, tools, and equipment for dental professionals and laboratories amounts to CHF238.80 million.

Insider Ownership: 22.2%

Earnings Growth Forecast: 22.9% p.a.

Coltene Holding is trading at a 40.1% discount to its estimated fair value, with earnings projected to grow significantly at 22.9% annually, surpassing the Swiss market's growth rate of 11.1%. Despite this strong earnings outlook, revenue growth is expected to lag behind the market and not exceed 20% per year. The return on equity is forecasted to reach a high level of 21.7%, yet profit margins have decreased from last year’s figures.

- Click here and access our complete growth analysis report to understand the dynamics of COLTENE Holding.

- Our valuation report here indicates COLTENE Holding may be undervalued.

Taking Advantage

- Click here to access our complete index of 1462 Fast Growing Companies With High Insider Ownership.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688246

Goodwill E-Health Info

Engages in the research and development of medical information software in China.

High growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor