Advertisement

Returns On Capital At Luyang Energy-Saving Materials (SZSE:002088) Have Stalled

What trends should we look for it we want to identify stocks that can multiply in value over the long term? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. With that in mind, the ROCE of Luyang Energy-Saving Materials (SZSE:002088) looks decent, right now, so lets see what the trend of returns can tell us.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Luyang Energy-Saving Materials:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

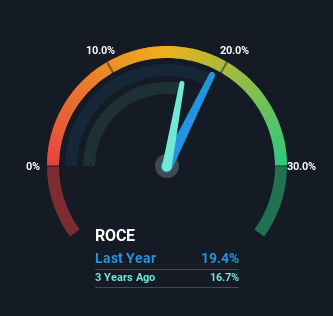

0.19 = CN¥555m ÷ (CN¥3.7b - CN¥852m) (Based on the trailing twelve months to September 2023).

So, Luyang Energy-Saving Materials has an ROCE of 19%. On its own, that's a standard return, however it's much better than the 5.9% generated by the Chemicals industry.

Check out our latest analysis for Luyang Energy-Saving Materials

In the above chart we have measured Luyang Energy-Saving Materials' prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for Luyang Energy-Saving Materials .

How Are Returns Trending?

While the returns on capital are good, they haven't moved much. The company has consistently earned 19% for the last five years, and the capital employed within the business has risen 46% in that time. 19% is a pretty standard return, and it provides some comfort knowing that Luyang Energy-Saving Materials has consistently earned this amount. Stable returns in this ballpark can be unexciting, but if they can be maintained over the long run, they often provide nice rewards to shareholders.

The Key Takeaway

The main thing to remember is that Luyang Energy-Saving Materials has proven its ability to continually reinvest at respectable rates of return. On top of that, the stock has rewarded shareholders with a remarkable 127% return to those who've held over the last five years. So even though the stock might be more "expensive" than it was before, we think the strong fundamentals warrant this stock for further research.

One more thing, we've spotted 1 warning sign facing Luyang Energy-Saving Materials that you might find interesting.

While Luyang Energy-Saving Materials may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002088

Luyang Energy-Saving Materials

Researches and develops, produces, and sells energy-saving products in the field of ceramic fiber, alumina fiber, soluble fiber, basalt fiber, and insulating firebrick in China and internationally.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor