Investors Still Aren't Entirely Convinced By Hangzhou Juheshun New Material Co.,LTD's (SHSE:605166) Earnings Despite 28% Price Jump

Those holding Hangzhou Juheshun New Material Co.,LTD (SHSE:605166) shares would be relieved that the share price has rebounded 28% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 27% in the last twelve months.

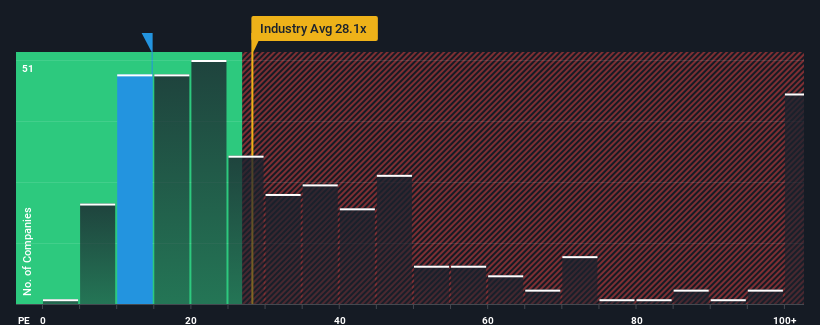

Although its price has surged higher, given about half the companies in China have price-to-earnings ratios (or "P/E's") above 30x, you may still consider Hangzhou Juheshun New MaterialLTD as a highly attractive investment with its 14.6x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Hangzhou Juheshun New MaterialLTD has been struggling lately as its earnings have declined faster than most other companies. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Check out our latest analysis for Hangzhou Juheshun New MaterialLTD

How Is Hangzhou Juheshun New MaterialLTD's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as depressed as Hangzhou Juheshun New MaterialLTD's is when the company's growth is on track to lag the market decidedly.

Retrospectively, the last year delivered a frustrating 23% decrease to the company's bottom line. Even so, admirably EPS has lifted 86% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 72% during the coming year according to the two analysts following the company. That's shaping up to be materially higher than the 41% growth forecast for the broader market.

In light of this, it's peculiar that Hangzhou Juheshun New MaterialLTD's P/E sits below the majority of other companies. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What We Can Learn From Hangzhou Juheshun New MaterialLTD's P/E?

Shares in Hangzhou Juheshun New MaterialLTD are going to need a lot more upward momentum to get the company's P/E out of its slump. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Hangzhou Juheshun New MaterialLTD currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Hangzhou Juheshun New MaterialLTD (1 makes us a bit uncomfortable!) that you need to be mindful of.

If these risks are making you reconsider your opinion on Hangzhou Juheshun New MaterialLTD, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Hangzhou Juheshun New MaterialLTD might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:605166

Hangzhou Juheshun New MaterialLTD

Engages in the research and development, manufacture, and sale of polyamide-6 chips in China, Europe, South America, Oceania, Southeast Asia, and internationally.

Undervalued with solid track record and pays a dividend.

Market Insights

Community Narratives