Advertisement

- China

- /

- Basic Materials

- /

- SHSE:600176

Take Care Before Diving Into The Deep End On China Jushi Co., Ltd. (SHSE:600176)

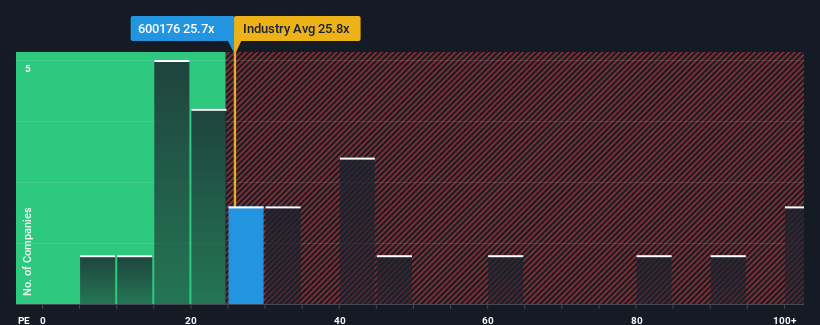

When close to half the companies in China have price-to-earnings ratios (or "P/E's") above 40x, you may consider China Jushi Co., Ltd. (SHSE:600176) as an attractive investment with its 25.7x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

China Jushi has been struggling lately as its earnings have declined faster than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

View our latest analysis for China Jushi

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like China Jushi's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 49%. This means it has also seen a slide in earnings over the longer-term as EPS is down 65% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 47% during the coming year according to the analysts following the company. With the market only predicted to deliver 37%, the company is positioned for a stronger earnings result.

In light of this, it's peculiar that China Jushi's P/E sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

What We Can Learn From China Jushi's P/E?

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that China Jushi currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. There could be some major unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

Before you take the next step, you should know about the 3 warning signs for China Jushi that we have uncovered.

If you're unsure about the strength of China Jushi's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600176

China Jushi

Engages in the manufacture and sale of fiberglass in China and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor