- China

- /

- Household Products

- /

- SZSE:001206

It's A Story Of Risk Vs Reward With Tianjin Yiyi Hygiene Products Co.,Ltd (SZSE:001206)

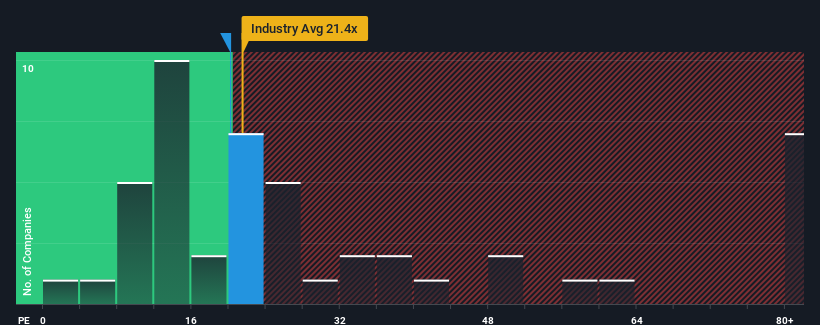

With a price-to-earnings (or "P/E") ratio of 20.2x Tianjin Yiyi Hygiene Products Co.,Ltd (SZSE:001206) may be sending bullish signals at the moment, given that almost half of all companies in China have P/E ratios greater than 30x and even P/E's higher than 53x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Recent times haven't been advantageous for Tianjin Yiyi Hygiene ProductsLtd as its earnings have been falling quicker than most other companies. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

View our latest analysis for Tianjin Yiyi Hygiene ProductsLtd

How Is Tianjin Yiyi Hygiene ProductsLtd's Growth Trending?

There's an inherent assumption that a company should underperform the market for P/E ratios like Tianjin Yiyi Hygiene ProductsLtd's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 20% decrease to the company's bottom line. As a result, earnings from three years ago have also fallen 59% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next year should generate growth of 63% as estimated by the four analysts watching the company. With the market only predicted to deliver 41%, the company is positioned for a stronger earnings result.

With this information, we find it odd that Tianjin Yiyi Hygiene ProductsLtd is trading at a P/E lower than the market. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On Tianjin Yiyi Hygiene ProductsLtd's P/E

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Tianjin Yiyi Hygiene ProductsLtd's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E anywhere near as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low, but investors seem to think future earnings could see a lot of volatility.

You always need to take note of risks, for example - Tianjin Yiyi Hygiene ProductsLtd has 1 warning sign we think you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Tianjin Yiyi Hygiene ProductsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:001206

Tianjin Yiyi Hygiene ProductsLtd

Engages in the research and development, design, production, and sale of disposable pet and personal hygiene care products in China and internationally.

Flawless balance sheet with proven track record.