- China

- /

- Medical Equipment

- /

- SHSE:688139

Further Upside For Qingdao Haier Biomedical Co.,Ltd (SHSE:688139) Shares Could Introduce Price Risks After 33% Bounce

Qingdao Haier Biomedical Co.,Ltd (SHSE:688139) shareholders would be excited to see that the share price has had a great month, posting a 33% gain and recovering from prior weakness. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 47% over that time.

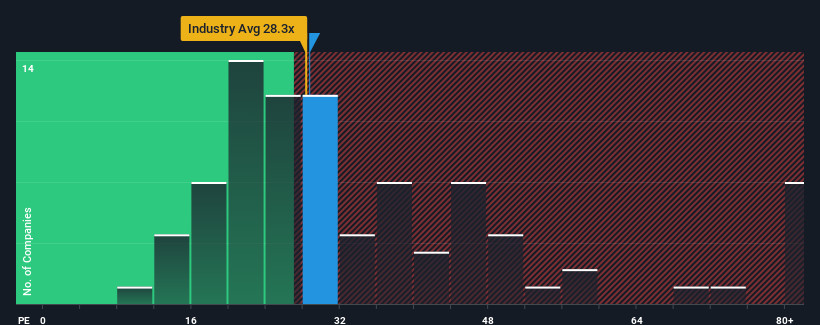

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Qingdao Haier BiomedicalLtd's P/E ratio of 28.7x, since the median price-to-earnings (or "P/E") ratio in China is also close to 30x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Qingdao Haier BiomedicalLtd could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to strengthen positively, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Check out our latest analysis for Qingdao Haier BiomedicalLtd

Does Growth Match The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like Qingdao Haier BiomedicalLtd's to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 34%. The last three years don't look nice either as the company has shrunk EPS by 44% in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next three years should generate growth of 23% each year as estimated by the four analysts watching the company. With the market only predicted to deliver 21% per annum, the company is positioned for a stronger earnings result.

With this information, we find it interesting that Qingdao Haier BiomedicalLtd is trading at a fairly similar P/E to the market. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Bottom Line On Qingdao Haier BiomedicalLtd's P/E

Qingdao Haier BiomedicalLtd appears to be back in favour with a solid price jump getting its P/E back in line with most other companies. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Qingdao Haier BiomedicalLtd currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Qingdao Haier BiomedicalLtd that you should be aware of.

You might be able to find a better investment than Qingdao Haier BiomedicalLtd. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Qingdao Haier BiomedicalLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688139

Qingdao Haier BiomedicalLtd

Engages in the design, manufacture, marketing, and sale of low temperature storage equipment for biomedical samples in China and internationally.

High growth potential with excellent balance sheet.

Market Insights

Community Narratives