Tianjin Guifaxiang 18th Street Mahua Food Co.,Ltd. (SZSE:002820) May Have Run Too Fast Too Soon With Recent 28% Price Plummet

The Tianjin Guifaxiang 18th Street Mahua Food Co.,Ltd. (SZSE:002820) share price has softened a substantial 28% over the previous 30 days, handing back much of the gains the stock has made lately. Longer-term shareholders will rue the drop in the share price, since it's now virtually flat for the year after a promising few quarters.

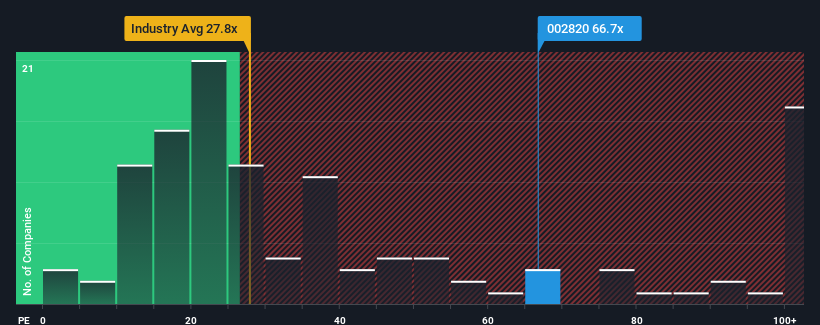

In spite of the heavy fall in price, Tianjin Guifaxiang 18th Street Mahua FoodLtd's price-to-earnings (or "P/E") ratio of 66.7x might still make it look like a strong sell right now compared to the market in China, where around half of the companies have P/E ratios below 32x and even P/E's below 19x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

For example, consider that Tianjin Guifaxiang 18th Street Mahua FoodLtd's financial performance has been poor lately as its earnings have been in decline. One possibility is that the P/E is high because investors think the company will still do enough to outperform the broader market in the near future. If not, then existing shareholders may be quite nervous about the viability of the share price.

See our latest analysis for Tianjin Guifaxiang 18th Street Mahua FoodLtd

Is There Enough Growth For Tianjin Guifaxiang 18th Street Mahua FoodLtd?

The only time you'd be truly comfortable seeing a P/E as steep as Tianjin Guifaxiang 18th Street Mahua FoodLtd's is when the company's growth is on track to outshine the market decidedly.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 9.6%. That put a dampener on the good run it was having over the longer-term as its three-year EPS growth is still a noteworthy 25% in total. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of earnings growth.

This is in contrast to the rest of the market, which is expected to grow by 38% over the next year, materially higher than the company's recent medium-term annualised growth rates.

In light of this, it's alarming that Tianjin Guifaxiang 18th Street Mahua FoodLtd's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Final Word

Tianjin Guifaxiang 18th Street Mahua FoodLtd's shares may have retreated, but its P/E is still flying high. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Tianjin Guifaxiang 18th Street Mahua FoodLtd currently trades on a much higher than expected P/E since its recent three-year growth is lower than the wider market forecast. When we see weak earnings with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Before you settle on your opinion, we've discovered 3 warning signs for Tianjin Guifaxiang 18th Street Mahua FoodLtd that you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Tianjin Guifaxiang 18th Street Mahua FoodLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002820

Tianjin Guifaxiang 18th Street Mahua FoodLtd

Tianjin Guifaxiang 18th Street Mahua Food Co.,Ltd.

Flawless balance sheet slight.

Market Insights

Community Narratives