Advertisement

- China

- /

- Consumer Services

- /

- SHSE:600636

China Reform Culture Holdings Co., Ltd.'s (SHSE:600636) Popularity With Investors Under Threat As Stock Sinks 27%

China Reform Culture Holdings Co., Ltd. (SHSE:600636) shares have had a horrible month, losing 27% after a relatively good period beforehand. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 17% share price drop.

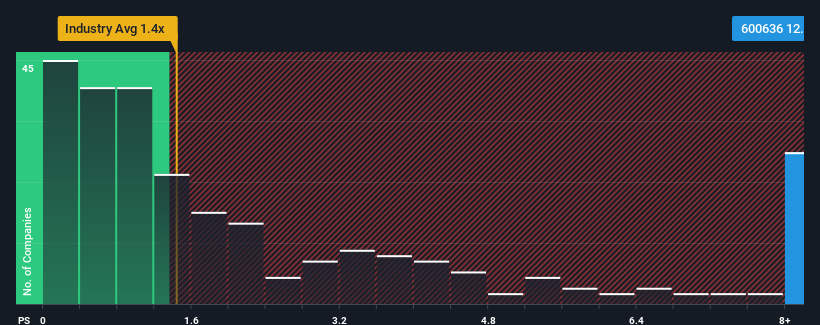

Although its price has dipped substantially, China Reform Culture Holdings may still be sending strong sell signals at present with a price-to-sales (or "P/S") ratio of 12.2x, when you consider almost half of the companies in the Consumer Services industry in China have P/S ratios under 4.5x and even P/S lower than 2x aren't out of the ordinary. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for China Reform Culture Holdings

How China Reform Culture Holdings Has Been Performing

China Reform Culture Holdings has been struggling lately as its revenue has declined faster than most other companies. It might be that many expect the dismal revenue performance to recover substantially, which has kept the P/S from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

Keen to find out how analysts think China Reform Culture Holdings' future stacks up against the industry? In that case, our free report is a great place to start.How Is China Reform Culture Holdings' Revenue Growth Trending?

In order to justify its P/S ratio, China Reform Culture Holdings would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered a frustrating 36% decrease to the company's top line. As a result, revenue from three years ago have also fallen 46% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 3.7% as estimated by the sole analyst watching the company. That's not great when the rest of the industry is expected to grow by 33%.

With this information, we find it concerning that China Reform Culture Holdings is trading at a P/S higher than the industry. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh heavily on the share price eventually.

The Final Word

Even after such a strong price drop, China Reform Culture Holdings' P/S still exceeds the industry median significantly. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

For a company with revenues that are set to decline in the context of a growing industry, China Reform Culture Holdings' P/S is much higher than we would've anticipated. Right now we aren't comfortable with the high P/S as the predicted future revenue decline likely to impact the positive sentiment that's propping up the P/S. Unless these conditions improve markedly, it'll be a challenging time for shareholders.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for China Reform Culture Holdings with six simple checks.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600636

China Reform Culture Holdings

Develops and sells educational recording and broadcasting software and hardware in China.

Flawless balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor