Advertisement

Nanjing Baose's (SZSE:300402) Solid Earnings May Rest On Weak Foundations

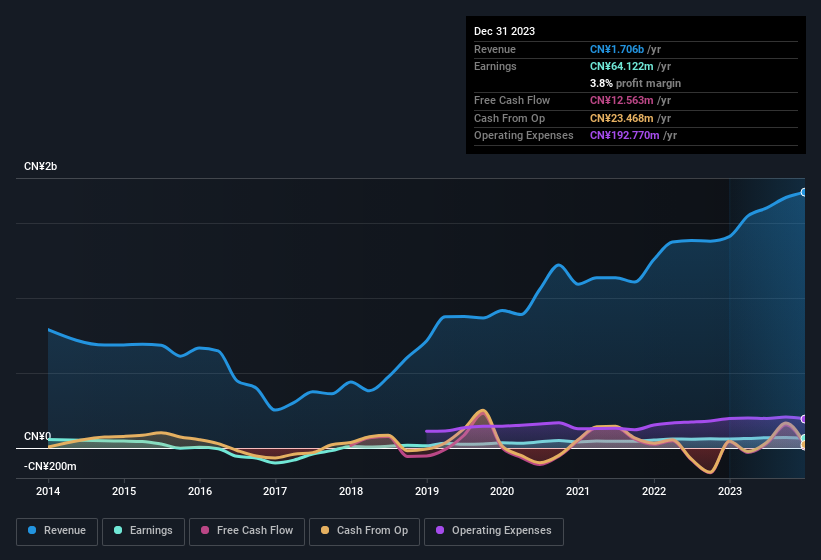

The recent earnings posted by Nanjing Baose Co., Ltd. (SZSE:300402) were solid, but the stock didn't move as much as we expected. However the statutory profit number doesn't tell the whole story, and we have found some factors which might be of concern to shareholders.

See our latest analysis for Nanjing Baose

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. Nanjing Baose expanded the number of shares on issue by 21% over the last year. That means its earnings are split among a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out Nanjing Baose's historical EPS growth by clicking on this link.

A Look At The Impact Of Nanjing Baose's Dilution On Its Earnings Per Share (EPS)

As you can see above, Nanjing Baose has been growing its net income over the last few years, with an annualized gain of 59% over three years. In comparison, earnings per share only gained 46% over the same period. And over the last 12 months, the company grew its profit by 6.2%. But that's starkly different from the 2.2% drop in earnings per share. Therefore, the dilution is having a noteworthy influence on shareholder returns.

In the long term, if Nanjing Baose's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Nanjing Baose.

Our Take On Nanjing Baose's Profit Performance

Each Nanjing Baose share now gets a meaningfully smaller slice of its overall profit, due to dilution of existing shareholders. Because of this, we think that it may be that Nanjing Baose's statutory profits are better than its underlying earnings power. Nonetheless, it's still worth noting that its earnings per share have grown at 46% over the last three years. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. You'd be interested to know, that we found 2 warning signs for Nanjing Baose and you'll want to know about these.

Today we've zoomed in on a single data point to better understand the nature of Nanjing Baose's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Valuation is complex, but we're here to simplify it.

Discover if Nanjing Baose might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300402

Nanjing Baose

Engages in the research and development, design, manufacture, and installation of special material pressure vessels and pipe fittings of titanium, zirconium, nickel, tantalum, copper, and stainless steel primarily in China.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor