Xizi Clean Energy Equipment Manufacturing Co., Ltd.'s (SZSE:002534) Shareholders Might Be Looking For Exit

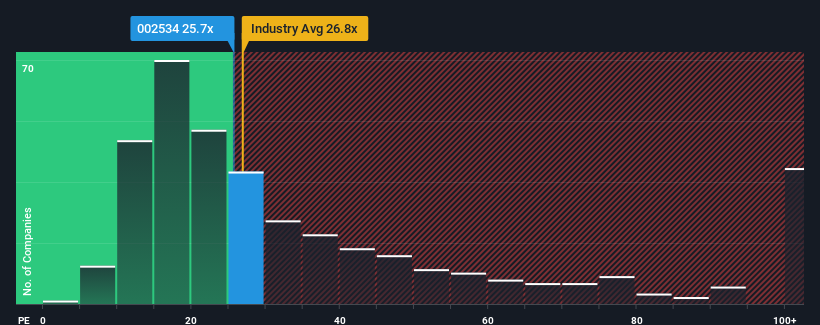

There wouldn't be many who think Xizi Clean Energy Equipment Manufacturing Co., Ltd.'s (SZSE:002534) price-to-earnings (or "P/E") ratio of 25.7x is worth a mention when the median P/E in China is similar at about 28x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Xizi Clean Energy Equipment Manufacturing certainly has been doing a good job lately as it's been growing earnings more than most other companies. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

See our latest analysis for Xizi Clean Energy Equipment Manufacturing

Does Growth Match The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like Xizi Clean Energy Equipment Manufacturing's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 54% last year. Still, incredibly EPS has fallen 45% in total from three years ago, which is quite disappointing. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next three years should generate growth of 17% per year as estimated by the lone analyst watching the company. That's shaping up to be materially lower than the 24% per year growth forecast for the broader market.

With this information, we find it interesting that Xizi Clean Energy Equipment Manufacturing is trading at a fairly similar P/E to the market. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as this level of earnings growth is likely to weigh down the shares eventually.

The Final Word

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Xizi Clean Energy Equipment Manufacturing's analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Xizi Clean Energy Equipment Manufacturing that you need to be mindful of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002534

Xizi Clean Energy Equipment Manufacturing

Researches, develops, produces, sells, installs, consults, and trades in boilers, pressure vessels, and environment protection equipment in China and internationally.

Excellent balance sheet average dividend payer.

Market Insights

Community Narratives