Advertisement

Beijing New Building Materials Public Limited Company (SZSE:000786) Shares Fly 27% But Investors Aren't Buying For Growth

Beijing New Building Materials Public Limited Company (SZSE:000786) shareholders would be excited to see that the share price has had a great month, posting a 27% gain and recovering from prior weakness. Notwithstanding the latest gain, the annual share price return of 4.0% isn't as impressive.

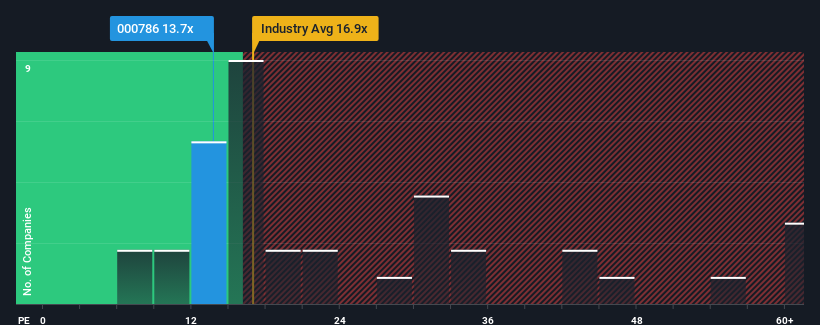

Although its price has surged higher, Beijing New Building Materials' price-to-earnings (or "P/E") ratio of 13.7x might still make it look like a strong buy right now compared to the market in China, where around half of the companies have P/E ratios above 29x and even P/E's above 54x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

Beijing New Building Materials certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Beijing New Building Materials

Does Growth Match The Low P/E?

In order to justify its P/E ratio, Beijing New Building Materials would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered a decent 13% gain to the company's bottom line. Although, the latest three year period in total hasn't been as good as it didn't manage to provide any growth at all. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 13% per year over the next three years. With the market predicted to deliver 19% growth per year, the company is positioned for a weaker earnings result.

With this information, we can see why Beijing New Building Materials is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On Beijing New Building Materials' P/E

Shares in Beijing New Building Materials are going to need a lot more upward momentum to get the company's P/E out of its slump. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Beijing New Building Materials' analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Having said that, be aware Beijing New Building Materials is showing 1 warning sign in our investment analysis, you should know about.

If these risks are making you reconsider your opinion on Beijing New Building Materials, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Beijing New Building Materials might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000786

Beijing New Building Materials

Manufactures and sells building materials in China and internationally.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor