XCMG Construction Machinery Co., Ltd. (SZSE:000425) Could Be Riskier Than It Looks

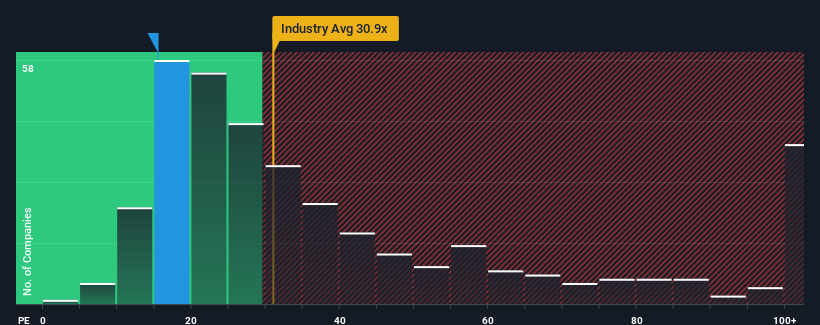

With a price-to-earnings (or "P/E") ratio of 15.4x XCMG Construction Machinery Co., Ltd. (SZSE:000425) may be sending very bullish signals at the moment, given that almost half of all companies in China have P/E ratios greater than 32x and even P/E's higher than 59x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Recent times have been advantageous for XCMG Construction Machinery as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for XCMG Construction Machinery

Does Growth Match The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like XCMG Construction Machinery's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 25% gain to the company's bottom line. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Shifting to the future, estimates from the eight analysts covering the company suggest earnings should grow by 43% over the next year. That's shaping up to be materially higher than the 38% growth forecast for the broader market.

In light of this, it's peculiar that XCMG Construction Machinery's P/E sits below the majority of other companies. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Final Word

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of XCMG Construction Machinery's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E anywhere near as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low, but investors seem to think future earnings could see a lot of volatility.

Before you take the next step, you should know about the 1 warning sign for XCMG Construction Machinery that we have uncovered.

If these risks are making you reconsider your opinion on XCMG Construction Machinery, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000425

XCMG Construction Machinery

Engages in the manufacture and sale of construction machinery in China.

Good value with reasonable growth potential and pays a dividend.