Advertisement

- Norway

- /

- Renewable Energy

- /

- OB:CLOUD

3 Stocks Including Cloudberry Clean Energy Estimated To Be Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

In a week marked by a divergence in major U.S. stock indexes, with growth stocks significantly outperforming value stocks, investors are navigating a complex landscape of mixed economic signals and geopolitical developments. As global markets continue to experience volatility and sector performance remains dispersed, identifying undervalued stocks becomes crucial for those looking to capitalize on potential market inefficiencies. In such an environment, assessing intrinsic value against current market prices can help investors uncover opportunities that might be overlooked amid broader market movements.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| SKS Technologies Group (ASX:SKS) | A$1.945 | A$3.85 | 49.5% |

| Aguas Andinas (SNSE:AGUAS-A) | CLP289.00 | CLP576.34 | 49.9% |

| Befesa (XTRA:BFSA) | €22.32 | €44.53 | 49.9% |

| Shanghai INT Medical Instruments (SEHK:1501) | HK$27.10 | HK$54.03 | 49.8% |

| Visional (TSE:4194) | ¥8535.00 | ¥17012.42 | 49.8% |

| Ingenia Communities Group (ASX:INA) | A$4.62 | A$9.15 | 49.5% |

| First Advantage (NasdaqGS:FA) | US$19.81 | US$39.49 | 49.8% |

| DoubleVerify Holdings (NYSE:DV) | US$20.77 | US$41.28 | 49.7% |

| Nyab (OM:NYAB) | SEK5.20 | SEK10.29 | 49.5% |

| Carter Bankshares (NasdaqGS:CARE) | US$19.30 | US$38.28 | 49.6% |

Let's take a closer look at a couple of our picks from the screened companies.

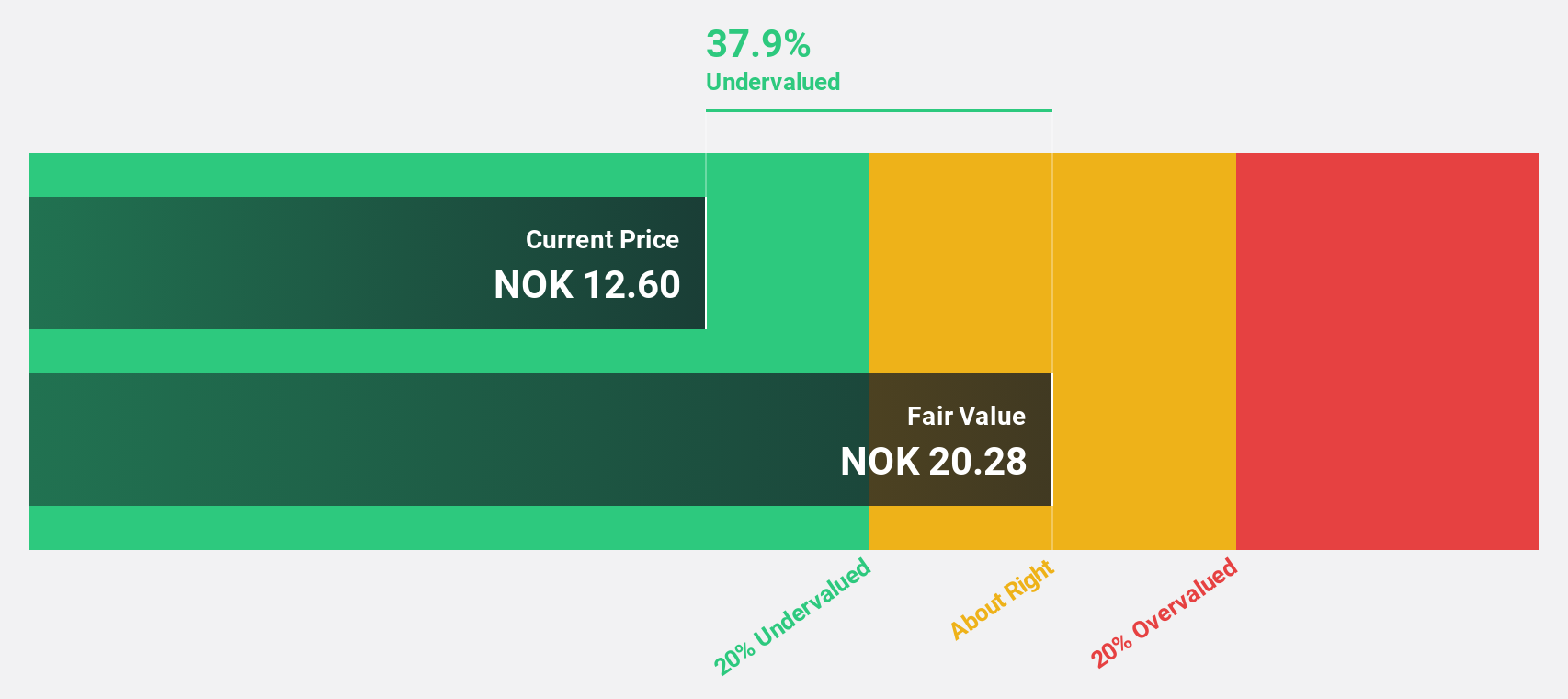

Cloudberry Clean Energy (OB:CLOUD)

Overview: Cloudberry Clean Energy ASA is a renewable energy company with a market cap of NOK3.46 billion.

Operations: The company's revenue segments include Operations at NOK60 million, Production at NOK572 million, and Development at NOK27 million.

Estimated Discount To Fair Value: 19.4%

Cloudberry Clean Energy is trading 19.4% below its estimated fair value of NOK14.89, suggesting potential undervaluation based on cash flows. Despite a forecasted revenue growth of 14.5% per year, which outpaces the Norwegian market, the company's Return on Equity is expected to remain low at 0.2%. Recent earnings showed improved net loss figures and increased power production year-to-date, indicating positive operational momentum despite lower quarterly sales compared to last year.

- Our growth report here indicates Cloudberry Clean Energy may be poised for an improving outlook.

- Click here to discover the nuances of Cloudberry Clean Energy with our detailed financial health report.

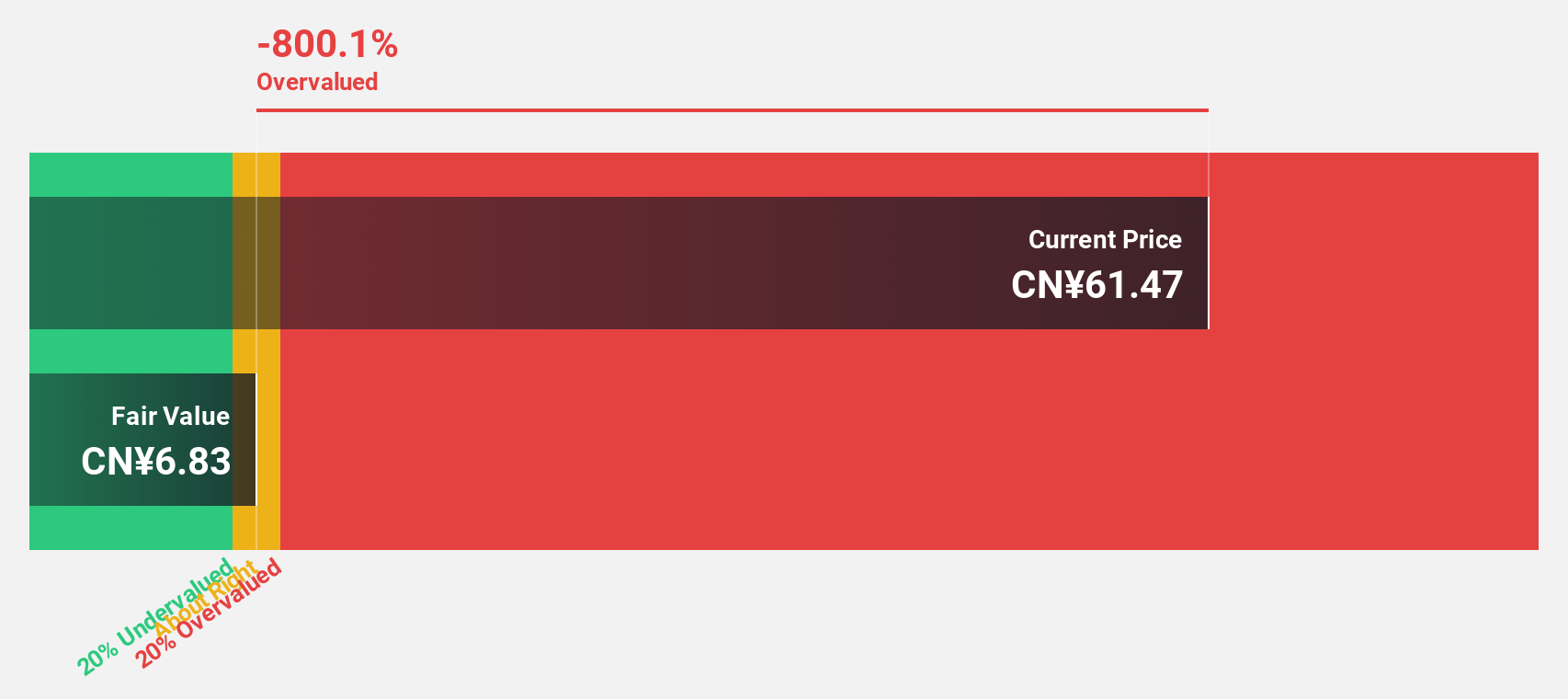

SolaX Power Network Technology (Zhejiang) (SHSE:688717)

Overview: SolaX Power Network Technology (Zhejiang) Co., Ltd. (SHSE:688717) operates in the renewable energy sector, focusing on the development and production of solar power products, with a market cap of CN¥9.01 billion.

Operations: The company generates revenue of CN¥2.87 billion from its Electronic Components & Parts segment.

Estimated Discount To Fair Value: 11.3%

SolaX Power Network Technology (Zhejiang) is trading 11.3% below its estimated fair value of CNY 63.49, reflecting potential undervaluation based on cash flows. Despite a significant drop in sales and net income for the nine months ending September 2024, earnings are projected to grow significantly at 54.1% annually, outpacing the Chinese market's growth rate. However, profit margins have decreased from last year, and share price volatility remains high over recent months.

- Upon reviewing our latest growth report, SolaX Power Network Technology (Zhejiang)'s projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of SolaX Power Network Technology (Zhejiang).

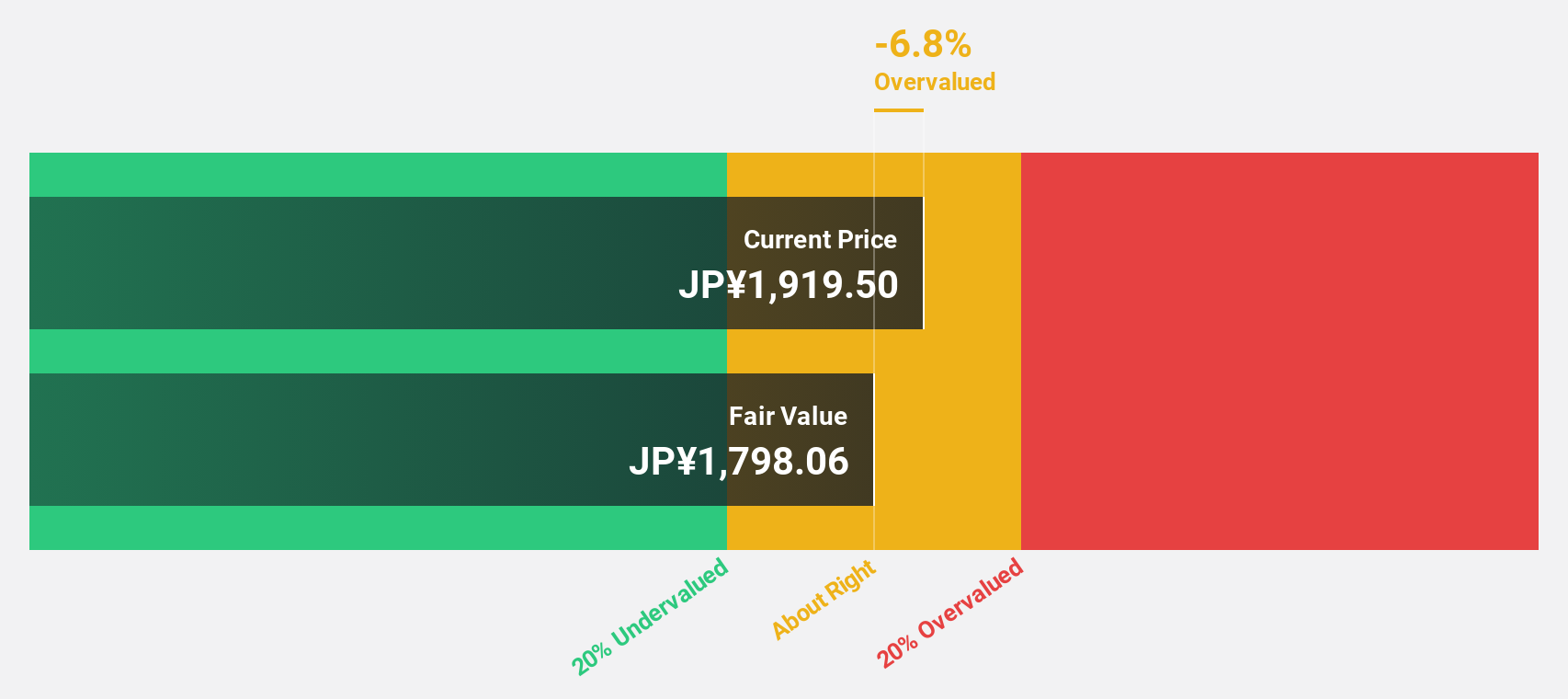

PARK24 (TSE:4666)

Overview: PARK24 Co., Ltd. operates and manages parking facilities both in Japan and internationally, with a market cap of ¥307.58 billion.

Operations: The company's revenue is derived from three main segments: the Mobility Business generating ¥107.36 million, Parking Lot Business Japan contributing ¥178.06 million, and Parking Lot Business Overseas accounting for ¥79.23 million.

Estimated Discount To Fair Value: 26.3%

PARK24 is trading at ¥1,803, 26.3% below its estimated fair value of ¥2,447.02, suggesting undervaluation based on cash flows. Earnings are projected to grow at 16.35% annually, surpassing the Japanese market's growth rate of 7.9%. Despite high debt levels and slower revenue growth forecasts of 5.7%, the company has shown a profit increase of 9.4% over the past year and anticipates strong future returns on equity at 30%.

- Our comprehensive growth report raises the possibility that PARK24 is poised for substantial financial growth.

- Get an in-depth perspective on PARK24's balance sheet by reading our health report here.

Seize The Opportunity

- Investigate our full lineup of 901 Undervalued Stocks Based On Cash Flows right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:CLOUD

Cloudberry Clean Energy

Operates as a renewable energy company in Norway, Denmark, Switzerland, and Sweden.

Limited growth with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.9% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.1% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|36.0% overvalued

DA

Community Contributor