3 Growth Stocks With High Insider Ownership And Up To 25% Revenue Growth

Reviewed by Simply Wall St

As global markets navigate a complex landscape marked by interest rate adjustments and sector-specific fluctuations, the S&P 500 Index has shown resilience with notable advances, particularly in utilities and real estate. Amidst these movements, growth companies with high insider ownership stand out as potential opportunities due to their alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.1% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.7% | 49.1% |

| Pharma Mar (BME:PHM) | 11.8% | 55.1% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Underneath we present a selection of stocks filtered out by our screen.

Ningbo Lehui International Engineering EquipmentLtd (SHSE:603076)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Ningbo Lehui International Engineering Equipment Co., Ltd. operates in the engineering equipment sector with a market cap of CN¥2.65 billion.

Operations: Ningbo Lehui International Engineering Equipment Co., Ltd. has revenue segments totaling CN¥0 million.

Insider Ownership: 21.2%

Revenue Growth Forecast: 14.5% p.a.

Ningbo Lehui International Engineering Equipment Ltd shows potential with forecasted annual earnings growth of 69.6%, outpacing the Chinese market's 23.8%. However, recent financial results reveal declining sales and net income, with profit margins dropping to 0.5% from last year's 1.1%. Revenue is expected to grow at a modest rate of 14.5% annually, slower than the desired benchmark of 20%. No significant insider trading activity has been reported in the past three months.

- Click to explore a detailed breakdown of our findings in Ningbo Lehui International Engineering EquipmentLtd's earnings growth report.

- Our valuation report here indicates Ningbo Lehui International Engineering EquipmentLtd may be overvalued.

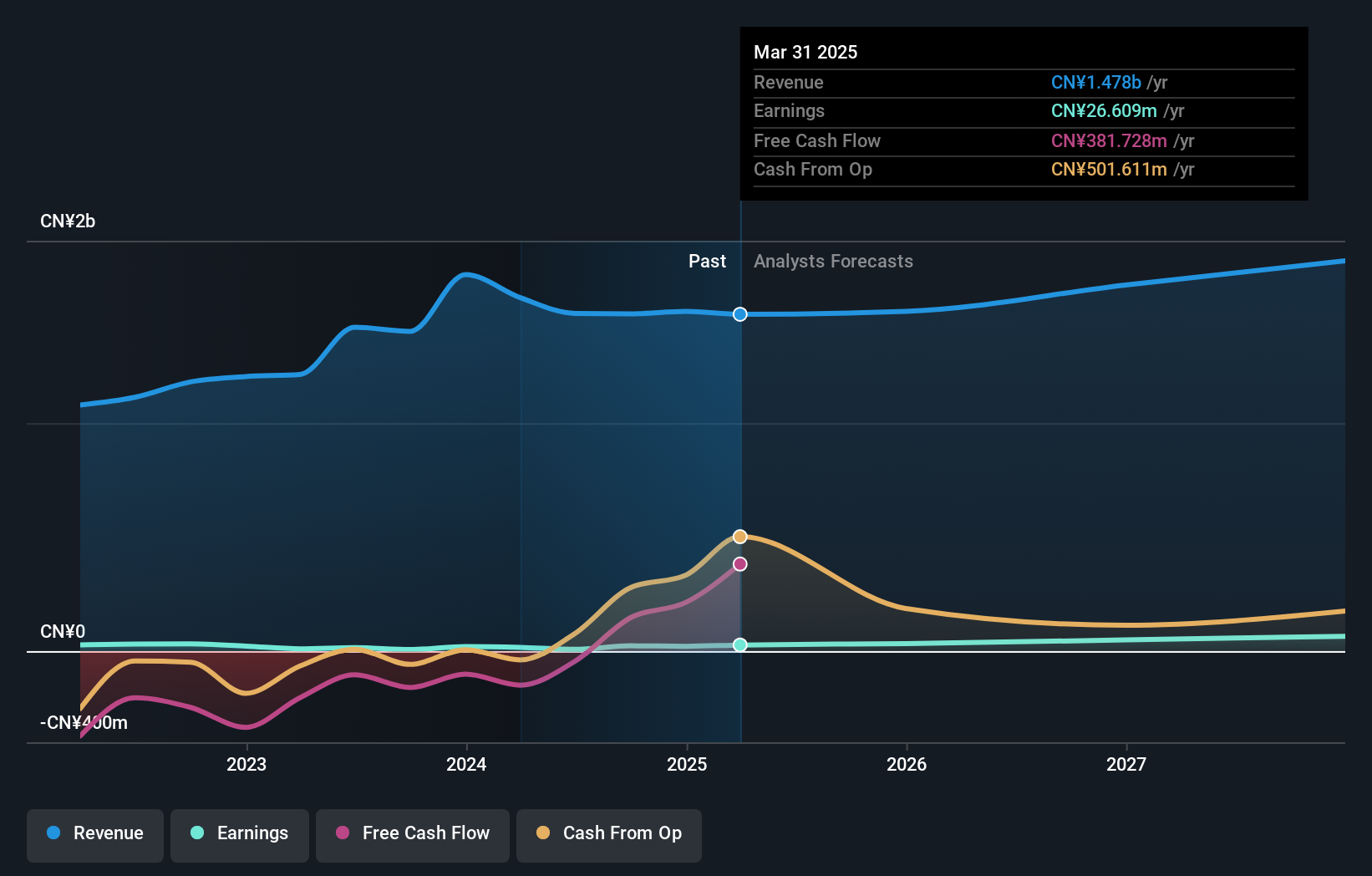

Beijing Tieke Shougang Rail Way-Tech (SHSE:688569)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Beijing Tieke Shougang Rail Way-Tech Co., Ltd. operates in the railway technology sector and has a market cap of CN¥4.92 billion.

Operations: The company's revenue is primarily derived from its Industrial Manufacturing segment, which generated CN¥1.33 billion.

Insider Ownership: 12%

Revenue Growth Forecast: 24.5% p.a.

Beijing Tieke Shougang Rail Way-Tech is forecast to achieve robust earnings growth of 44.4% annually, surpassing the Chinese market's average. Revenue growth is also expected to outpace the market at 24.5% per year. Despite these positive forecasts, recent financial results show a decline in sales and net income compared to last year, with profit margins decreasing from 20% to 13.7%. The company trades at a favorable price-to-earnings ratio of 27x relative to the market but has an unstable dividend track record.

- Click here to discover the nuances of Beijing Tieke Shougang Rail Way-Tech with our detailed analytical future growth report.

- Our valuation report here indicates Beijing Tieke Shougang Rail Way-Tech may be undervalued.

Jiangsu Kuangshun Photosensitivity New-Material Stock (SZSE:300537)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu Kuangshun Photosensitivity New-Material Stock Co., Ltd. operates in the photosensitive materials industry with a market capitalization of CN¥4.01 billion.

Operations: The company generates revenue from the Fine Chemicals Industry segment, amounting to CN¥527.07 million.

Insider Ownership: 37.5%

Revenue Growth Forecast: 25.3% p.a.

Jiangsu Kuangshun Photosensitivity New-Material Stock is experiencing strong growth, with earnings forecast to increase significantly at 62.1% annually, outpacing the Chinese market's average of 23.8%. Revenue is also expected to grow rapidly at 25.3% per year. However, the company has faced shareholder dilution recently and exhibits high share price volatility. Recent half-year results showed sales rising to CNY 259.2 million and net income reaching CNY 27.85 million, indicating robust performance despite these challenges.

- Take a closer look at Jiangsu Kuangshun Photosensitivity New-Material Stock's potential here in our earnings growth report.

- Our comprehensive valuation report raises the possibility that Jiangsu Kuangshun Photosensitivity New-Material Stock is priced higher than what may be justified by its financials.

Summing It All Up

- Unlock our comprehensive list of 1501 Fast Growing Companies With High Insider Ownership by clicking here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Ningbo Lehui International Engineering EquipmentLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603076

Ningbo Lehui International Engineering EquipmentLtd

Ningbo Lehui International Engineering Equipment Co.,Ltd.

Reasonable growth potential with adequate balance sheet.