Advertisement

- China

- /

- Metals and Mining

- /

- SHSE:688750

Fraser and Neave And 2 Other Undiscovered Gems With Strong Fundamentals

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a complex landscape of cautious Federal Reserve commentary and political uncertainties, smaller-cap indexes have faced notable challenges, with the Russell 2000 Index experiencing significant declines. Amidst this backdrop, investors are keenly observing economic indicators such as consumer spending and job data to gauge potential opportunities within the small-cap sector. In this environment, strong fundamentals become crucial for identifying promising stocks, like Fraser and Neave and two other undiscovered gems that demonstrate resilience and potential despite broader market volatility.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sun | 14.28% | 5.73% | 64.26% | ★★★★★★ |

| Caisse Régionale de Crédit Agricole Mutuel Brie Picardie Société coopérative | 34.89% | 3.23% | 3.61% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Top Union Electronics | 1.25% | 6.67% | 17.52% | ★★★★★★ |

| Yulie Sekuritas Indonesia | NA | 18.62% | 9.58% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Chita Kogyo | 8.34% | 2.84% | 8.49% | ★★★★★☆ |

| Union Coop | NA | -4.69% | -14.06% | ★★★★☆☆ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

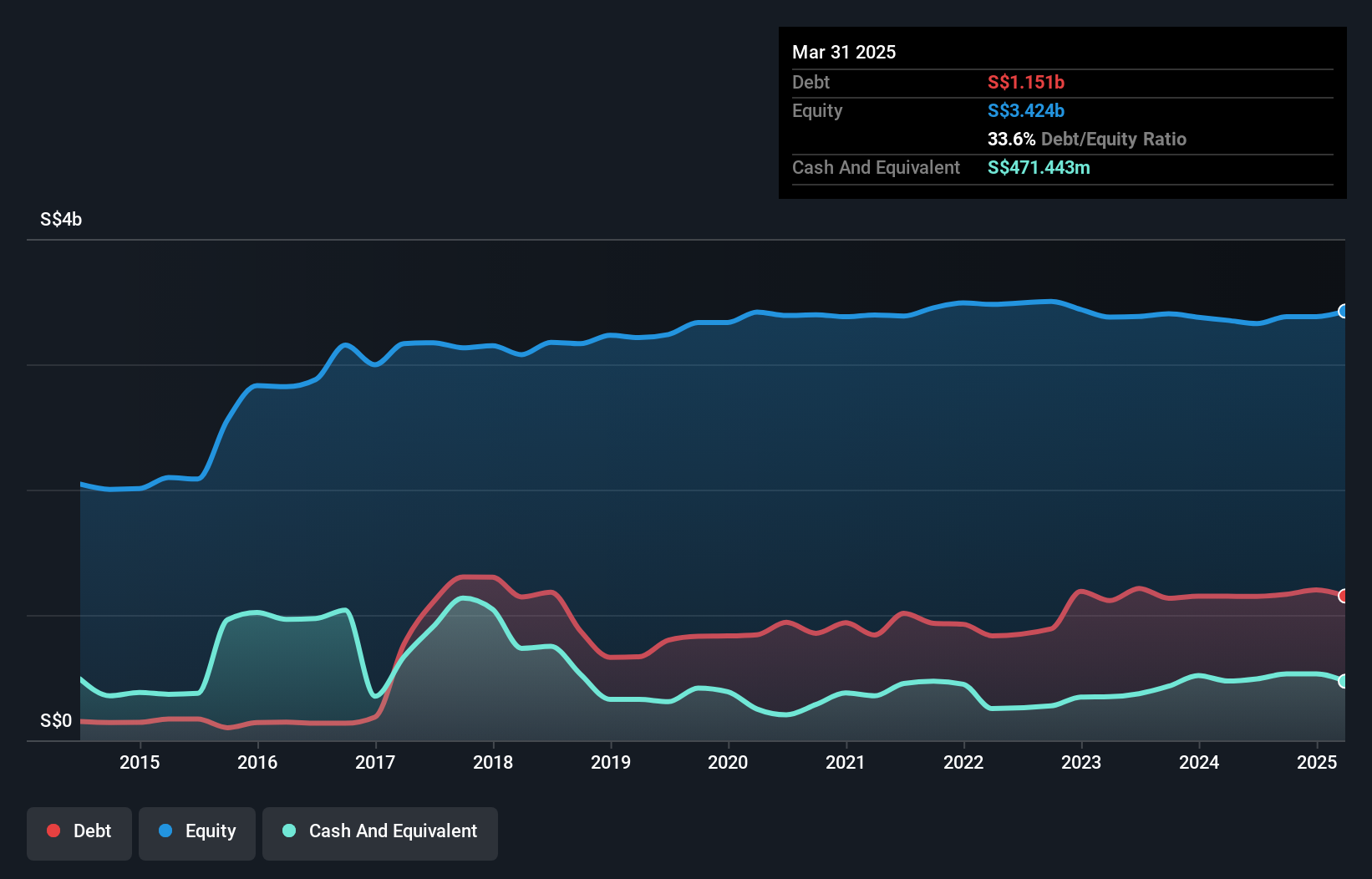

Fraser and Neave (SGX:F99)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Fraser and Neave, Limited operates in the food and beverage as well as publishing and printing sectors across Singapore, Malaysia, Thailand, Vietnam, and internationally with a market capitalization of SGD1.98 billion.

Operations: Fraser and Neave generates revenue primarily from its Dairies segment, contributing SGD1.21 billion, followed by Beverages at SGD672.65 million, and Printing & Publishing at SGD203.25 million.

Fraser and Neave, known for its robust performance in the food industry, reported a solid year with sales reaching S$2.16 billion, up from S$2.10 billion last year. The company boasts high-quality earnings and a net income of S$150.91 million compared to S$133.22 million previously, reflecting an earnings growth of 13.3% over the past year despite a broader industry downturn of -10.4%. Its debt to equity ratio increased from 24.9% to 34.5% over five years but remains satisfactory at 18.8%. Recent board changes signal strategic shifts as it continues navigating market challenges confidently.

- Navigate through the intricacies of Fraser and Neave with our comprehensive health report here.

Evaluate Fraser and Neave's historical performance by accessing our past performance report.

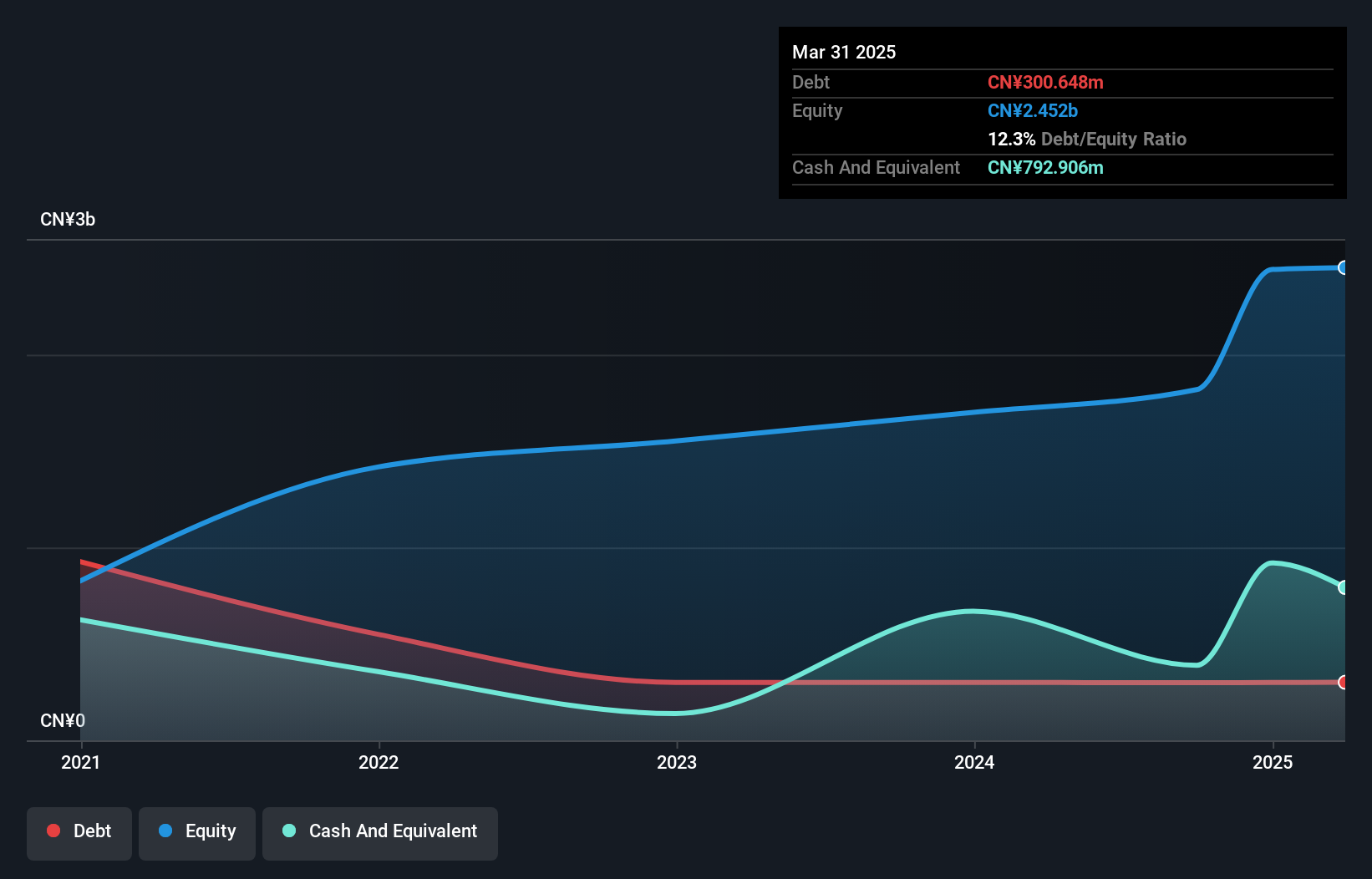

Hunan Xiangtou Goldsky Titanium Industry Technology (SHSE:688750)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hunan Xiangtou Goldsky Titanium Industry Technology Co., Ltd. is engaged in the production and processing of titanium materials, with a market capitalization of CN¥9.86 billion.

Operations: The primary revenue stream for Hunan Xiangtou Goldsky Titanium Industry Technology comes from its Metal Processors and Fabrication segment, generating CN¥855.13 million.

Hunan Xiangtou Goldsky Titanium Industry Technology, a small cap player in the metals sector, recently completed an IPO raising CNY 662.3 million, offering shares at CNY 7.16 each. The company's earnings surged by 17.9% last year, outpacing the broader Metals and Mining industry which saw a -2.3% change. With high-quality earnings and more cash than total debt, financial stability seems assured despite illiquid shares. Levered free cash flow improved significantly from CNY -9.21 million in 2020 to CNY 179.91 million in 2023 but dipped slightly to CNY 112.07 million by September 2024 due to increased capital expenditure of CNY -70.94 million this year.

- Click here to discover the nuances of Hunan Xiangtou Goldsky Titanium Industry Technology with our detailed analytical health report.

Learn about Hunan Xiangtou Goldsky Titanium Industry Technology's historical performance.

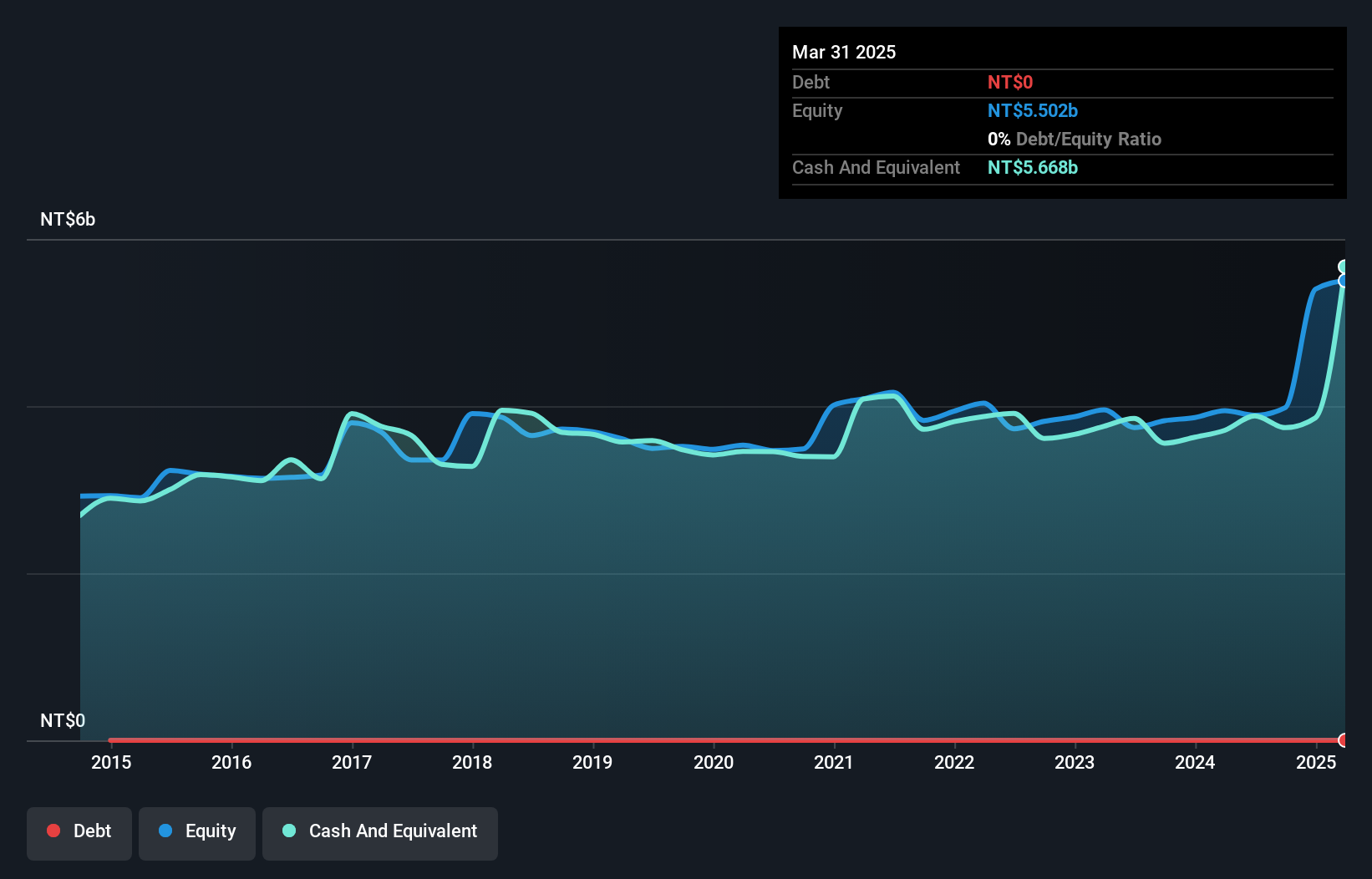

PharmaEngine (TPEX:4162)

Simply Wall St Value Rating: ★★★★★★

Overview: PharmaEngine, Inc. is a biopharmaceutical company focused on developing cancer treatment drugs in Taiwan and Europe, with a market capitalization of NT$13.07 billion.

Operations: PharmaEngine generates revenue primarily from new medicine development, amounting to NT$831.92 million.

PharmaEngine's recent performance highlights its robust position in the biotech sector, with earnings growth of 27.2% over the past year, outpacing industry peers. The company, debt-free for five years, reported a net income increase to TWD 92 million in Q3 2024 from TWD 81 million a year ago. Despite sales dipping to TWD 218 million from TWD 246 million, basic EPS rose to TWD 0.64 from TWD 0.56 due to efficient operations and high-quality earnings. A new distribution agreement with Shanghai RMX Biopharma for LIPORAXEL could bolster future revenues in Taiwan's market.

- Delve into the full analysis health report here for a deeper understanding of PharmaEngine.

Understand PharmaEngine's track record by examining our Past report.

Make It Happen

- Navigate through the entire inventory of 4632 Undiscovered Gems With Strong Fundamentals here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hunan Xiangtou Goldsky Titanium Industry Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688750

Hunan Xiangtou Goldsky Titanium Industry Technology

Hunan Xiangtou Goldsky Titanium Industry Technology Co., Ltd.

Adequate balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor