Advertisement

Market Might Still Lack Some Conviction On China Railway Construction Heavy Industry Corporation Limited (SHSE:688425) Even After 35% Share Price Boost

China Railway Construction Heavy Industry Corporation Limited (SHSE:688425) shareholders have had their patience rewarded with a 35% share price jump in the last month. Taking a wider view, although not as strong as the last month, the full year gain of 15% is also fairly reasonable.

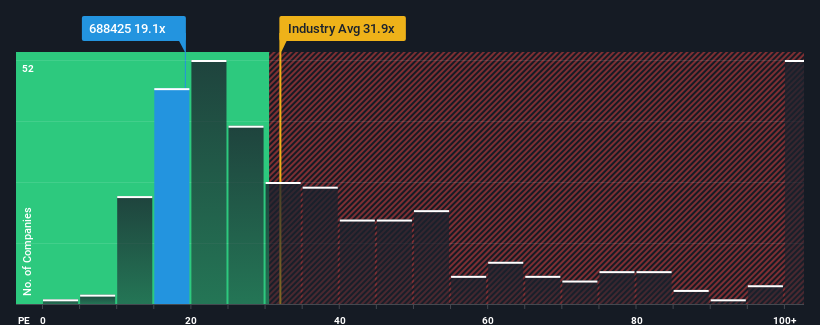

Even after such a large jump in price, China Railway Construction Heavy Industry's price-to-earnings (or "P/E") ratio of 19.1x might still make it look like a buy right now compared to the market in China, where around half of the companies have P/E ratios above 34x and even P/E's above 64x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

China Railway Construction Heavy Industry has been struggling lately as its earnings have declined faster than most other companies. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Check out our latest analysis for China Railway Construction Heavy Industry

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like China Railway Construction Heavy Industry's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 29%. The last three years don't look nice either as the company has shrunk EPS by 49% in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 19% per annum during the coming three years according to the sole analyst following the company. That's shaping up to be similar to the 19% each year growth forecast for the broader market.

In light of this, it's peculiar that China Railway Construction Heavy Industry's P/E sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

The Key Takeaway

Despite China Railway Construction Heavy Industry's shares building up a head of steam, its P/E still lags most other companies. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of China Railway Construction Heavy Industry's analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide more support to the share price.

You should always think about risks. Case in point, we've spotted 2 warning signs for China Railway Construction Heavy Industry you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688425

China Railway Construction Heavy Industry

Engages in the research, design, manufacturing, and servicing of underground engineering and rail transit equipment in China and internationally.

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor