Advertisement

3 Growth Companies With High Insider Ownership And Revenue Growth Up To 27%

Simply Wall St

Reviewed by Simply Wall St

As global markets experience mixed performances, with major U.S. indices like the S&P 500 and Nasdaq Composite reaching record highs amid a rally in growth stocks, investors are increasingly focused on opportunities within high-growth sectors. In this context, companies with significant insider ownership and robust revenue growth can be particularly appealing as they often signal confidence from those closest to the business and potential for continued expansion.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| SKS Technologies Group (ASX:SKS) | 32.4% | 24.8% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.9% | 39.9% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 34.2% |

| Medley (TSE:4480) | 34% | 31.7% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 131.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 66.7% |

| HANA Micron (KOSDAQ:A067310) | 18.4% | 110.9% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.6% |

Below we spotlight a couple of our favorites from our exclusive screener.

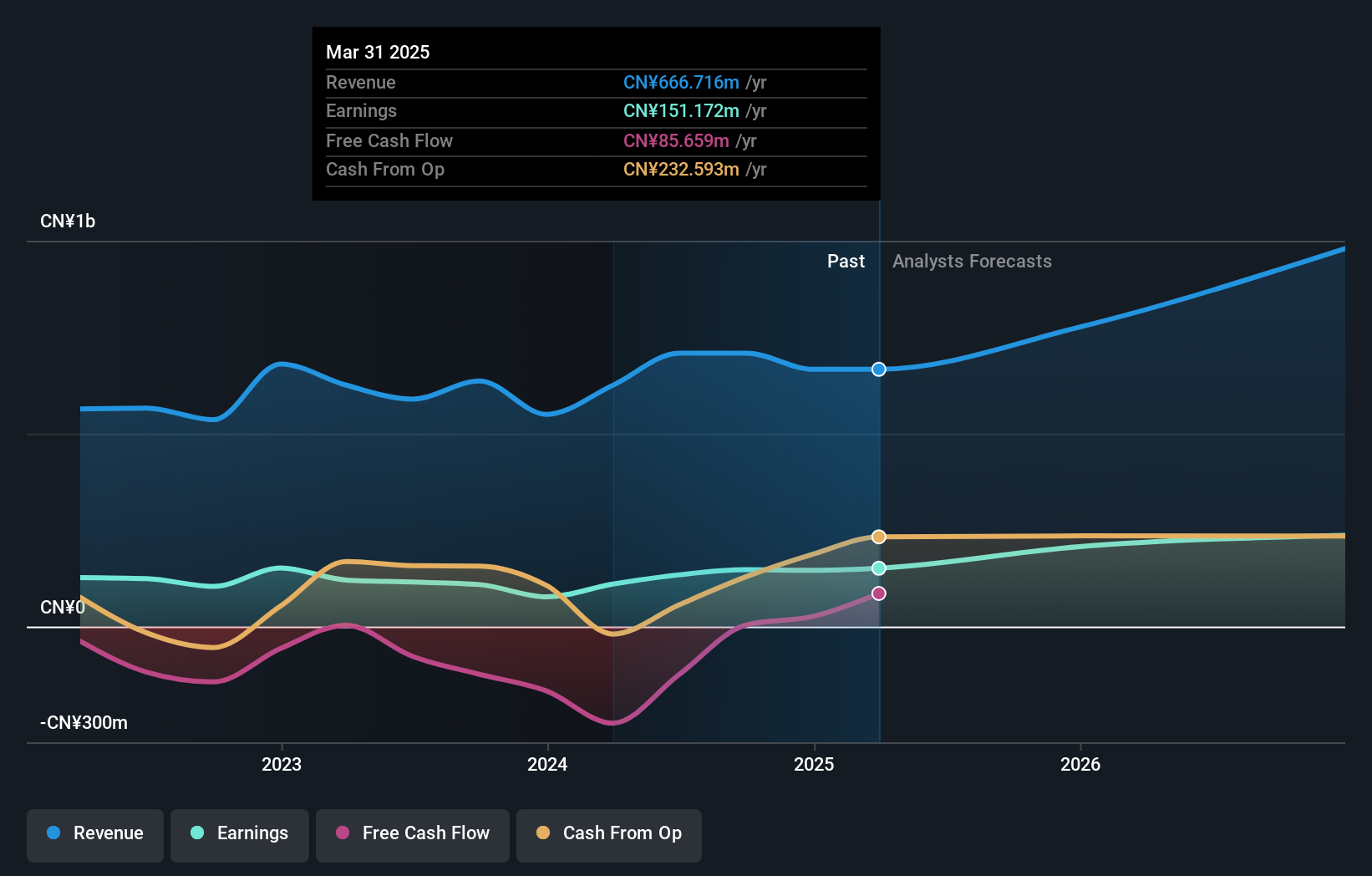

China Catalyst Holding (SHSE:688267)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: China Catalyst Holding Co., Ltd. focuses on the R&D, production, and sale of zeolite catalysts, customized process package solutions, and fine chemicals both in China and internationally, with a market cap of CN¥4.05 billion.

Operations: The company's revenue segment includes Chemical Reagent and Auxiliary Manufacturing, generating CN¥708.63 million.

Insider Ownership: 31.5%

Revenue Growth Forecast: 24.9% p.a.

China Catalyst Holding demonstrates robust growth potential with significant earnings expansion, reporting a net income of CNY 113.66 million for the first nine months of 2024, up from CNY 43.28 million a year prior. The company's revenue is forecast to grow at 24.9% annually, outpacing the broader CN market's growth rate of 13.7%. Despite its Price-To-Earnings ratio being lower than the market average, insider trading activity remains stable without substantial buying or selling in recent months.

- Click here and access our complete growth analysis report to understand the dynamics of China Catalyst Holding.

- Our expertly prepared valuation report China Catalyst Holding implies its share price may be too high.

OKE Precision Cutting Tools (SHSE:688308)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: OKE Precision Cutting Tools Co., Ltd. is involved in the research, development, production, and sale of cemented carbide and CNC cutting tool products with a market cap of CN¥3.38 billion.

Operations: The company's revenue primarily comes from its Metal Processors and Fabrication segment, which generated CN¥1.12 billion.

Insider Ownership: 25.2%

Revenue Growth Forecast: 18.5% p.a.

OKE Precision Cutting Tools shows promising growth with forecasted earnings expansion of 38.31% annually, surpassing the CN market's 25.9%. Despite a decline in net income to CNY 89.83 million for the first nine months of 2024, revenue increased to CNY 894.97 million from CNY 804.66 million last year. The Price-To-Earnings ratio is favorable at 35.1x compared to the market's 37.2x, yet profit margins decreased significantly from last year’s levels.

- Click here to discover the nuances of OKE Precision Cutting Tools with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential overvaluation of OKE Precision Cutting Tools shares in the market.

Chipsea Technologies (shenzhen) (SHSE:688595)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Chipsea Technologies (shenzhen) Corp. is a chip design company specializing in ADCs, MCUs, measurement algorithms, and IoT solutions in China with a market cap of CN¥4.23 billion.

Operations: The company generates revenue of CN¥663.45 million from its Integrated Circuit segment.

Insider Ownership: 36.9%

Revenue Growth Forecast: 27.2% p.a.

Chipsea Technologies is experiencing robust revenue growth, with a forecasted annual increase of 27.2%, outpacing the broader CN market's 13.7%. Despite reporting a net loss of CNY 114.98 million for the first nine months of 2024, sales surged to CNY 514.37 million from last year's CNY 283.87 million. The company is expected to achieve profitability within three years, although its return on equity is projected to be modest at 9.6%.

- Delve into the full analysis future growth report here for a deeper understanding of Chipsea Technologies (shenzhen).

- The valuation report we've compiled suggests that Chipsea Technologies (shenzhen)'s current price could be inflated.

Turning Ideas Into Actions

- Navigate through the entire inventory of 1511 Fast Growing Companies With High Insider Ownership here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688267

China Catalyst Holding

Engages in the research and development, production, and sale of zeolite catalyst, customized process package solutions, and fine chemicals in China and internationally.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor