- China

- /

- Electrical

- /

- SHSE:603819

There's No Escaping Changzhou Shenli Electrical Machine Incorporated Company's (SHSE:603819) Muted Revenues Despite A 27% Share Price Rise

Changzhou Shenli Electrical Machine Incorporated Company (SHSE:603819) shareholders would be excited to see that the share price has had a great month, posting a 27% gain and recovering from prior weakness. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 22% over that time.

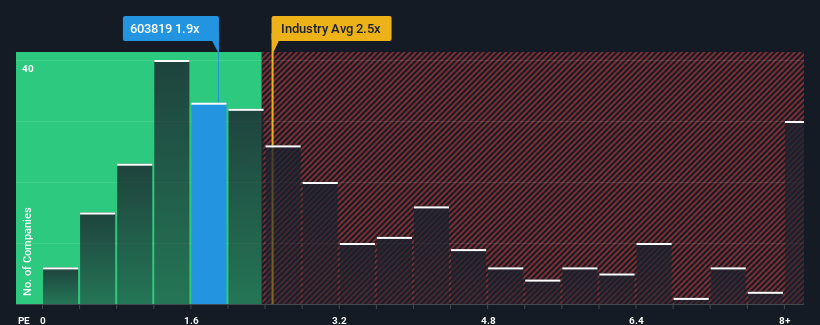

Even after such a large jump in price, Changzhou Shenli Electrical Machine's price-to-sales (or "P/S") ratio of 1.9x might still make it look like a buy right now compared to the Electrical industry in China, where around half of the companies have P/S ratios above 2.5x and even P/S above 5x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

See our latest analysis for Changzhou Shenli Electrical Machine

What Does Changzhou Shenli Electrical Machine's P/S Mean For Shareholders?

As an illustration, revenue has deteriorated at Changzhou Shenli Electrical Machine over the last year, which is not ideal at all. It might be that many expect the disappointing revenue performance to continue or accelerate, which has repressed the P/S. Those who are bullish on Changzhou Shenli Electrical Machine will be hoping that this isn't the case so that they can pick up the stock at a lower valuation.

Although there are no analyst estimates available for Changzhou Shenli Electrical Machine, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The Low P/S Ratio?

Changzhou Shenli Electrical Machine's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Retrospectively, the last year delivered a frustrating 6.1% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 1.6% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

In contrast to the company, the rest of the industry is expected to grow by 26% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this in mind, we understand why Changzhou Shenli Electrical Machine's P/S is lower than most of its industry peers. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as recent revenue trends are already weighing down the shares.

What We Can Learn From Changzhou Shenli Electrical Machine's P/S?

Despite Changzhou Shenli Electrical Machine's share price climbing recently, its P/S still lags most other companies. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Changzhou Shenli Electrical Machine revealed its shrinking revenue over the medium-term is contributing to its low P/S, given the industry is set to grow. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Before you take the next step, you should know about the 3 warning signs for Changzhou Shenli Electrical Machine (1 is a bit unpleasant!) that we have uncovered.

If you're unsure about the strength of Changzhou Shenli Electrical Machine's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

If you're looking to trade Changzhou Shenli Electrical Machine, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603819

Changzhou Shenli Electrical Machine

Manufactures and sells motors, generator stator and rotor punching sheets, and iron cores in China and internationally.

Low with imperfect balance sheet.

Market Insights

Community Narratives