- China

- /

- Electrical

- /

- SHSE:600847

There's Reason For Concern Over Chongqing Wanli New Energy Co., Ltd.'s (SHSE:600847) Massive 33% Price Jump

Chongqing Wanli New Energy Co., Ltd. (SHSE:600847) shares have continued their recent momentum with a 33% gain in the last month alone. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 3.7% in the last twelve months.

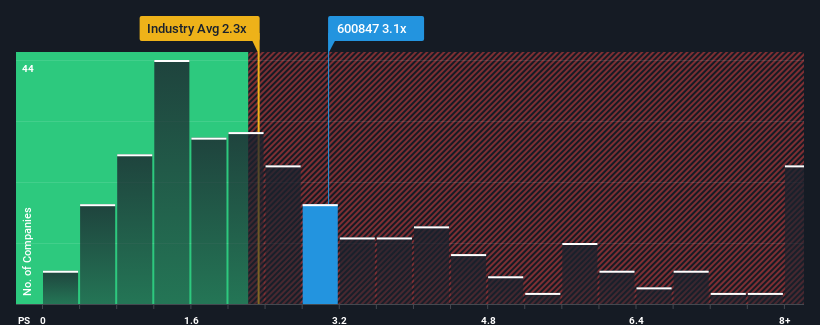

After such a large jump in price, given close to half the companies operating in China's Electrical industry have price-to-sales ratios (or "P/S") below 2.3x, you may consider Chongqing Wanli New Energy as a stock to potentially avoid with its 3.1x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

See our latest analysis for Chongqing Wanli New Energy

How Chongqing Wanli New Energy Has Been Performing

For example, consider that Chongqing Wanli New Energy's financial performance has been pretty ordinary lately as revenue growth is non-existent. Perhaps the market believes that revenue growth will improve markedly over current levels, inflating the P/S ratio. If not, then existing shareholders may be a little nervous about the viability of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Chongqing Wanli New Energy's earnings, revenue and cash flow.How Is Chongqing Wanli New Energy's Revenue Growth Trending?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Chongqing Wanli New Energy's to be considered reasonable.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. This isn't what shareholders were looking for as it means they've been left with a 16% decline in revenue over the last three years in total. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Comparing that to the industry, which is predicted to deliver 25% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

With this in mind, we find it worrying that Chongqing Wanli New Energy's P/S exceeds that of its industry peers. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Bottom Line On Chongqing Wanli New Energy's P/S

The large bounce in Chongqing Wanli New Energy's shares has lifted the company's P/S handsomely. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Chongqing Wanli New Energy currently trades on a much higher than expected P/S since its recent revenues have been in decline over the medium-term. Right now we aren't comfortable with the high P/S as this revenue performance is highly unlikely to support such positive sentiment for long. Should recent medium-term revenue trends persist, it would pose a significant risk to existing shareholders' investments and prospective investors will have a hard time accepting the current value of the stock.

A lot of potential risks can sit within a company's balance sheet. Our free balance sheet analysis for Chongqing Wanli New Energy with six simple checks will allow you to discover any risks that could be an issue.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

If you're looking to trade Chongqing Wanli New Energy, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600847

Chongqing Wanli New Energy

Engages in the design, manufacture, and sale of lead-acid batteries in China.

Flawless balance sheet and overvalued.

Market Insights

Community Narratives