Advertisement

- China

- /

- Trade Distributors

- /

- SHSE:600153

Xiamen C&D Inc.'s (SHSE:600153) Price Is Right But Growth Is Lacking After Shares Rocket 33%

Xiamen C&D Inc. (SHSE:600153) shareholders would be excited to see that the share price has had a great month, posting a 33% gain and recovering from prior weakness. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 5.4% over the last year.

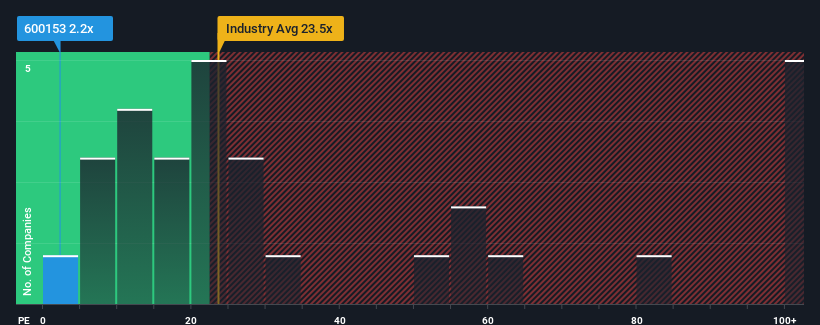

In spite of the firm bounce in price, Xiamen C&D's price-to-earnings (or "P/E") ratio of 2.2x might still make it look like a strong buy right now compared to the market in China, where around half of the companies have P/E ratios above 29x and even P/E's above 54x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Xiamen C&D certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Xiamen C&D

Is There Any Growth For Xiamen C&D?

The only time you'd be truly comfortable seeing a P/E as depressed as Xiamen C&D's is when the company's growth is on track to lag the market decidedly.

Retrospectively, the last year delivered an exceptional 143% gain to the company's bottom line. Pleasingly, EPS has also lifted 151% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to slump, contracting by 18% per year during the coming three years according to the five analysts following the company. That's not great when the rest of the market is expected to grow by 19% each year.

In light of this, it's understandable that Xiamen C&D's P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Bottom Line On Xiamen C&D's P/E

Xiamen C&D's recent share price jump still sees its P/E sitting firmly flat on the ground. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Xiamen C&D maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you settle on your opinion, we've discovered 3 warning signs for Xiamen C&D (1 makes us a bit uncomfortable!) that you should be aware of.

Of course, you might also be able to find a better stock than Xiamen C&D. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600153

Xiamen C&D

Engages in the supply chain and real estate development businesses in China and internationally.

Very undervalued with flawless balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|11.0% undervalued

CH

Community Contributor