Advertisement

Banco de Chile's (SNSE:CHILE) Dividend Will Be Increased To CLP9.85

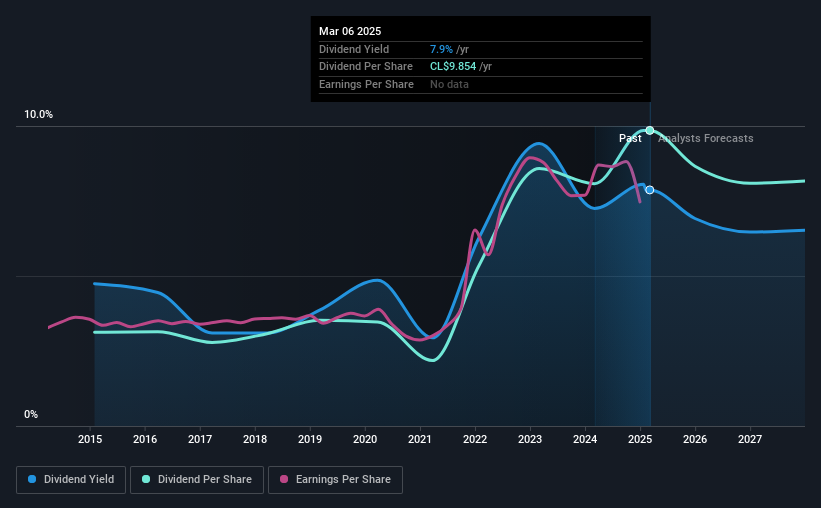

Banco de Chile (SNSE:CHILE) has announced that it will be increasing its dividend from last year's comparable payment on the 27th of March to CLP9.85. This makes the dividend yield 7.9%, which is above the industry average.

Check out our latest analysis for Banco de Chile

Banco de Chile's Earnings Will Easily Cover The Distributions

If the payments aren't sustainable, a high yield for a few years won't matter that much.

Banco de Chile has a long history of paying out dividends, with its current track record at a minimum of 10 years. Taking data from its last earnings report, calculating for the company's payout ratio shows 82%, which means that Banco de Chile would be able to pay its last dividend without pressure on the balance sheet.

Looking forward, EPS is forecast to rise by 2.6% over the next 3 years. Analyst estimates also show the future payout ratio being 67% in the same 3 years which brings it into quite a comfortable range.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2015, the dividend has gone from CLP3.13 total annually to CLP9.85. This means that it has been growing its distributions at 12% per annum over that time. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

Banco de Chile's Dividend Might Lack Growth

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Banco de Chile has impressed us by growing EPS at 15% per year over the past five years. Past earnings growth has been decent, but unless this is one of those rare businesses that can grow without additional capital investment or marketing spend, we'd generally expect the higher payout ratio to limit its future growth prospects.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. In general, the distributions are a little bit higher than we would like, but we can't ignore the fact the quickly growing earnings gives this stock great potential in the future. We don't think Banco de Chile is a great stock to add to your portfolio if income is your focus.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 1 warning sign for Banco de Chile that investors should take into consideration. Is Banco de Chile not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Banco de Chile might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SNSE:CHILE

Banco de Chile

Operates as a commercial bank that provides banking services in Chile.

Average dividend payer with moderate growth potential.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|32.6% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.6% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.6% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.2% undervalued

RO

Community Contributor