Kudelski SA (VTX:KUD) Just Reported Earnings, And Analysts Cut Their Target Price

Kudelski SA (VTX:KUD) shareholders are probably feeling a little disappointed, since its shares fell 2.6% to CHF4.78 in the week after its latest annual results. The result was fairly weak overall, with revenues of US$729m being 5.9% less than what the analysts had been modelling. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

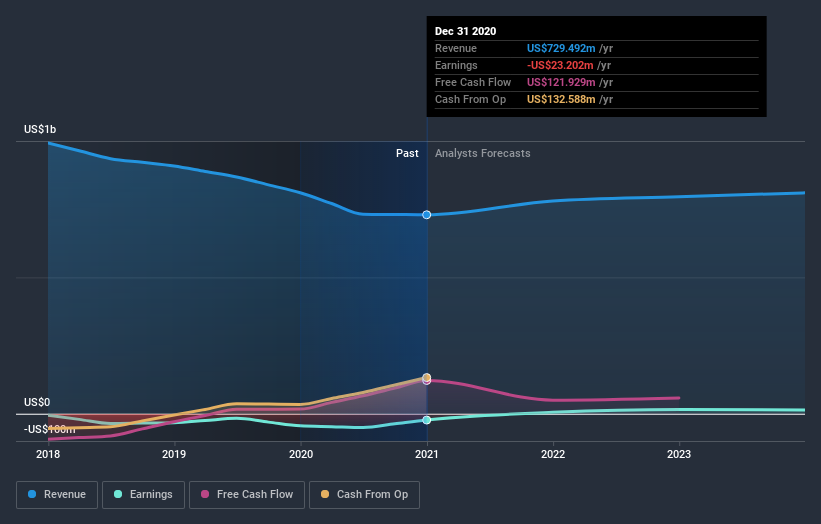

See our latest analysis for Kudelski

After the latest results, the three analysts covering Kudelski are now predicting revenues of US$780.3m in 2021. If met, this would reflect a modest 7.0% improvement in sales compared to the last 12 months. Kudelski is also expected to turn profitable, with statutory earnings of US$0.10 per share. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$780.9m and earnings per share (EPS) of US$0.23 in 2021. So there's definitely been a decline in sentiment after the latest results, noting the large cut to new EPS forecasts.

The average price target fell 28% to CHF1.64, with reduced earnings forecasts clearly tied to a lower valuation estimate. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Kudelski analyst has a price target of CHF2.08 per share, while the most pessimistic values it at CHF1.20. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. One thing stands out from these estimates, which is that Kudelski is forecast to grow faster in the future than it has in the past, with revenues expected to grow 7.0%. If achieved, this would be a much better result than the 6.4% annual decline over the past five years. Compare this against analyst estimates for the wider industry, which suggest that (in aggregate) industry revenues are expected to grow 8.0% next year. So while Kudelski's revenues are expected to improve, it seems that it is expected to grow at about the same rate as the overall industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Happily, there were no real changes to sales forecasts, with the business still expected to grow in line with the overall industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Kudelski going out to 2023, and you can see them free on our platform here..

We don't want to rain on the parade too much, but we did also find 3 warning signs for Kudelski (2 are potentially serious!) that you need to be mindful of.

If you’re looking to trade Kudelski, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kudelski might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SWX:KUD

Kudelski

Provides digital access and security solutions for digital television and interactive applications in Switzerland, the United States, France, Germany, Austria, and internationally.

Undervalued with high growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

CS Disco Stock: Legal AI Is Moving From Efficiency Tool to Competitive Necessity

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)