- Switzerland

- /

- Specialty Stores

- /

- SWX:AVOL

Avolta (VTX:AVOL) Has Announced That It Will Be Increasing Its Dividend To CHF1.00

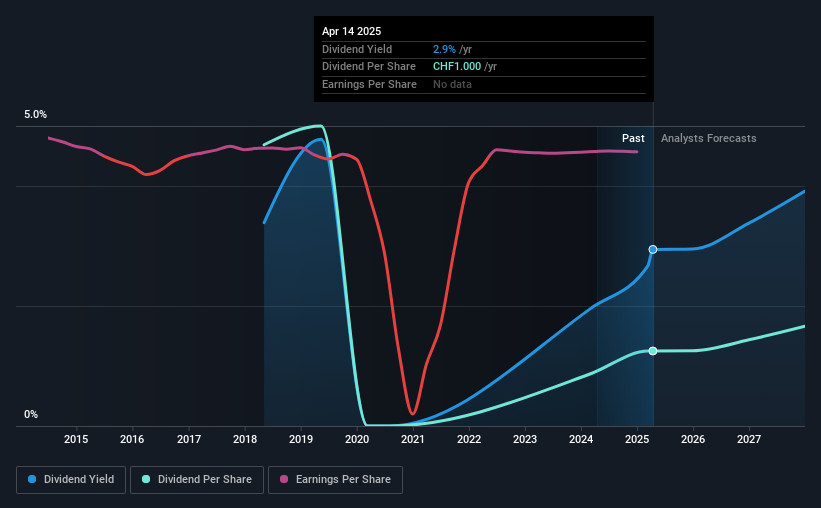

Avolta AG (VTX:AVOL) will increase its dividend from last year's comparable payment on the 20th of May to CHF1.00. This makes the dividend yield about the same as the industry average at 2.9%.

Our free stock report includes 2 warning signs investors should be aware of before investing in Avolta. Read for free now.Avolta's Projected Earnings Seem Likely To Cover Future Distributions

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important. Prior to this announcement, the company was paying out 143% of what it was earning, however the dividend was quite comfortably covered by free cash flows at a cash payout ratio of only 6.8%. Given that the dividend is a cash outflow, we think that cash is more important than accounting measures of profit when assessing the dividend, so this is a mitigating factor.

According to analysts, EPS should be several times higher next year. Assuming the dividend continues along recent trends, we estimate that the payout ratio could reach 31%, which is in a comfortable range for us.

View our latest analysis for Avolta

Avolta's Dividend Has Lacked Consistency

Looking back, Avolta's dividend hasn't been particularly consistent. Due to this, we are a little bit cautious about the dividend consistency over a full economic cycle. Since 2018, the annual payment back then was CHF3.75, compared to the most recent full-year payment of CHF1.00. The dividend has fallen 73% over that period. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

Dividend Growth Could Be Constrained

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. It's encouraging to see that Avolta has been growing its earnings per share at 61% a year over the past five years. While EPS is growing rapidly, Avolta paid out a very high 143% of its income as dividends. If earnings continue to grow, this dividend may be sustainable, but we think a payout this high definitely bears watching.

Our Thoughts On Avolta's Dividend

Overall, we always like to see the dividend being raised, but we don't think Avolta will make a great income stock. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We don't think Avolta is a great stock to add to your portfolio if income is your focus.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. Case in point: We've spotted 2 warning signs for Avolta (of which 1 makes us a bit uncomfortable!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:AVOL

Reasonable growth potential and slightly overvalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion