- Switzerland

- /

- Software

- /

- SWX:TEMN

Top Growth Companies With High Insider Ownership On SIX Swiss Exchange October 2024

Reviewed by Simply Wall St

The Swiss market showed resilience recently, with the benchmark SMI recovering from early losses to close slightly higher, reflecting a cautiously optimistic sentiment among investors. In this context, growth companies with high insider ownership on the SIX Swiss Exchange are particularly noteworthy as they often signal strong confidence from those closest to the business and can be appealing in times of market fluctuation.

Top 10 Growth Companies With High Insider Ownership In Switzerland

| Name | Insider Ownership | Earnings Growth |

| Stadler Rail (SWX:SRAIL) | 14.5% | 24.1% |

| VAT Group (SWX:VACN) | 10.2% | 22.5% |

| Addex Therapeutics (SWX:ADXN) | 19% | 33.3% |

| Straumann Holding (SWX:STMN) | 32.7% | 21.8% |

| LEM Holding (SWX:LEHN) | 29.9% | 18.4% |

| Swissquote Group Holding (SWX:SQN) | 11.4% | 12.6% |

| Temenos (SWX:TEMN) | 21.8% | 14.4% |

| V-ZUG Holding (SWX:VZUG) | 20.9% | 38.7% |

| Sensirion Holding (SWX:SENS) | 19.9% | 102.7% |

| Kudelski (SWX:KUD) | 37.5% | 121.7% |

Here we highlight a subset of our preferred stocks from the screener.

Leonteq (SWX:LEON)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Leonteq AG offers structured investment products and long-term savings and retirement solutions across Switzerland, Europe, and Asia including the Middle East, with a market cap of CHF472.40 million.

Operations: The company's revenue segment includes brokerage services, generating CHF243.18 million.

Insider Ownership: 12.2%

Earnings Growth Forecast: 35.1% p.a.

Leonteq AG, with substantial insider ownership, is positioned for significant earnings growth at 35.1% annually, outpacing the Swiss market. Despite a challenging first half of 2024 with net income dropping to CHF 15.7 million from CHF 28.8 million year-on-year and profit margins decreasing to 3.1%, the stock trades significantly below its estimated fair value. Revenue growth is forecasted at 10.3% annually, surpassing the Swiss market average but trailing higher benchmarks for rapid expansion companies.

- Dive into the specifics of Leonteq here with our thorough growth forecast report.

- The valuation report we've compiled suggests that Leonteq's current price could be inflated.

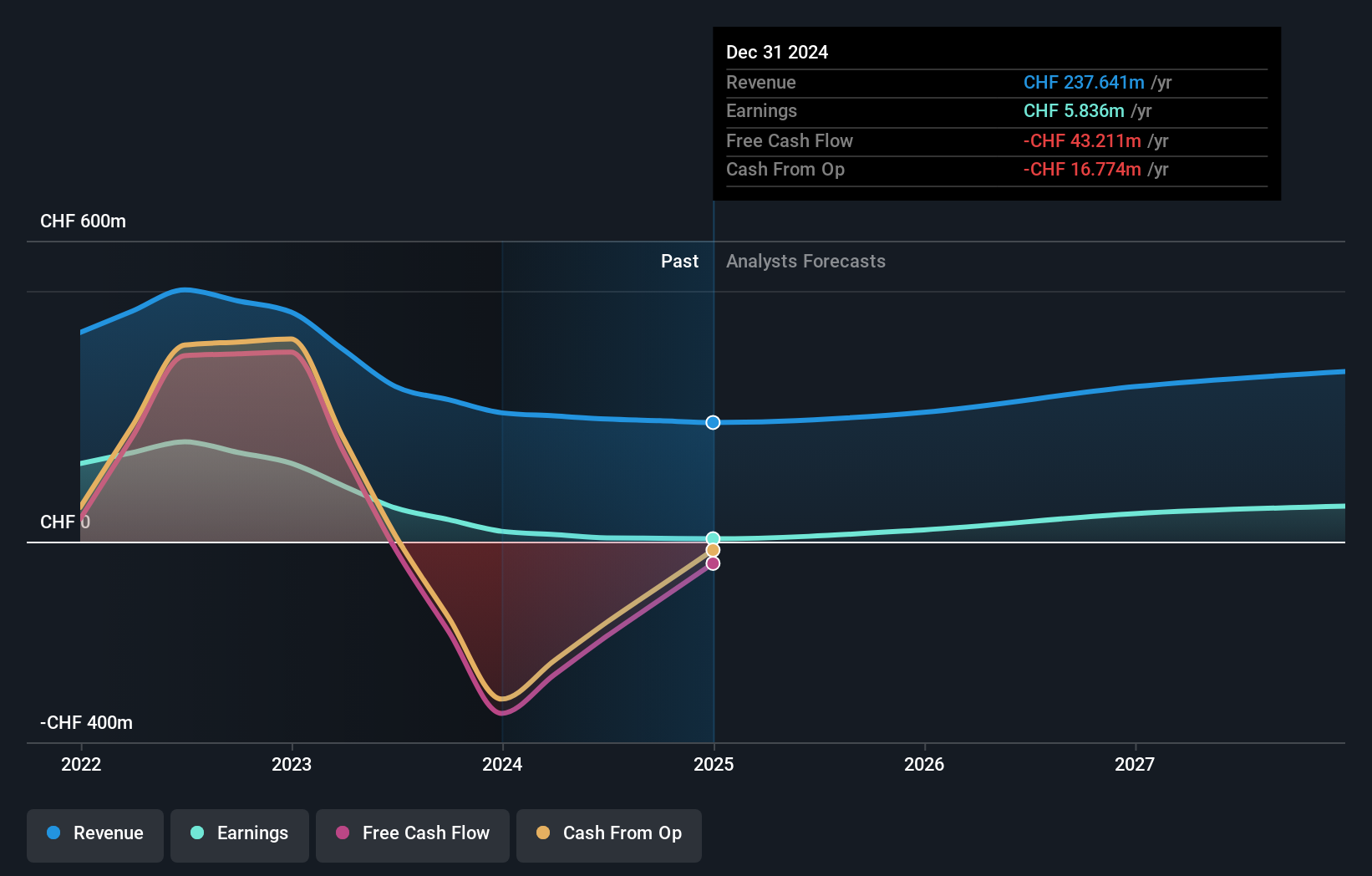

Temenos (SWX:TEMN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Temenos AG develops, markets, and sells integrated banking software systems to financial institutions globally, with a market cap of CHF4.32 billion.

Operations: The company's revenue is derived from two primary segments: Product, contributing $879.99 million, and Services, accounting for $132.98 million.

Insider Ownership: 21.8%

Earnings Growth Forecast: 14.4% p.a.

Temenos, with high insider ownership, is set for earnings growth of 14.4% annually, surpassing the Swiss market's 11.7%. Despite trading at a 24.1% discount to its estimated fair value and facing high debt levels, revenue is expected to grow at 7.6% per year. Recent strategic appointments aim to boost global expansion through cloud and AI solutions. The company completed a CHF 200 million share buyback program in August 2024, enhancing shareholder value.

- Get an in-depth perspective on Temenos' performance by reading our analyst estimates report here.

- Our valuation report here indicates Temenos may be undervalued.

V-ZUG Holding (SWX:VZUG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: V-ZUG Holding AG develops, manufactures, markets, sells, and services kitchen and laundry appliances for private households in Switzerland and internationally, with a market cap of CHF347.14 million.

Operations: The company's revenue primarily comes from its Household Appliances segment, generating CHF571.35 million.

Insider Ownership: 20.9%

Earnings Growth Forecast: 38.7% p.a.

V-ZUG Holding demonstrates significant earnings growth potential, with forecasts indicating a 38.7% annual increase, outpacing the Swiss market's 11.7%. Despite a recent dip in sales to CHF 284.08 million for H1 2024, net income doubled to CHF 8.73 million. The stock trades at a substantial discount to its estimated fair value and has high insider ownership, though its return on equity is projected low at 7.5% over three years.

- Take a closer look at V-ZUG Holding's potential here in our earnings growth report.

- The valuation report we've compiled suggests that V-ZUG Holding's current price could be quite moderate.

Seize The Opportunity

- Get an in-depth perspective on all 13 Fast Growing SIX Swiss Exchange Companies With High Insider Ownership by using our screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Temenos might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:TEMN

Temenos

Develops, markets, and sells integrated banking software systems to banking and other financial institutions worldwide.

Average dividend payer and fair value.