- Switzerland

- /

- Electrical

- /

- SWX:ABBN

Assessing ABB’s Value After Recent 20% Rally and Grid Modernization Push

Reviewed by Bailey Pemberton

Are you wondering if ABB’s stock still has gas in the tank, or if now’s the time to take a breather? You’re not alone. Investors everywhere are keeping an eye on this global automation and electrification leader, especially after some impressive moves on the chart. Just look at the numbers: ABB has climbed 2.5% in the last week, popped up 5.4% in the last month, and is up nearly 20% since the start of the year. Stretch the timeline out, and the gains are even more convincing. The stock is up more than 150% over three years and 185% in the last five years. That’s not just steady growth; it’s serious momentum, especially considering the shifts we’ve seen in technology and infrastructure markets worldwide.

The conversation around ABB has heated up lately, with investors noting how fresh market developments such as a global push toward smarter grids and energy efficiency could play into ABB’s strength. Still, as tempting as it is to buy in after a strong run, the real question comes down to value. Is ABB still undervalued, or are its bigger moves already baked into the price? By our current calculation, ABB clocks in with a valuation score of 1 out of 6, so it only meets one undervaluation benchmark by traditional measures.

Let’s dive deeper into how that score is calculated, and what different valuation methods reveal about the stock’s current pricing. Stay tuned, too, as there may be an even more insightful way to decide whether ABB is a buy for the future.

ABB scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: ABB Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model works by estimating all future cash flows that a company is expected to generate, then discounting those amounts back to today's value. This approach aims to determine a company's intrinsic worth based on its expected ability to generate cash in years to come.

For ABB, the most recent reported Free Cash Flow is $3.78 billion. Analysts provide forecasts for the next five years, projecting ABB’s annual FCF to climb steadily. By 2029, the estimated Free Cash Flow reaches $5.96 billion. There is further extrapolated growth beyond that point based on moderate growth assumptions by Simply Wall St. These ten-year projections show a continuation of positive momentum. It is worth remembering that forecasts after year five rely on less certain trends rather than published analyst data.

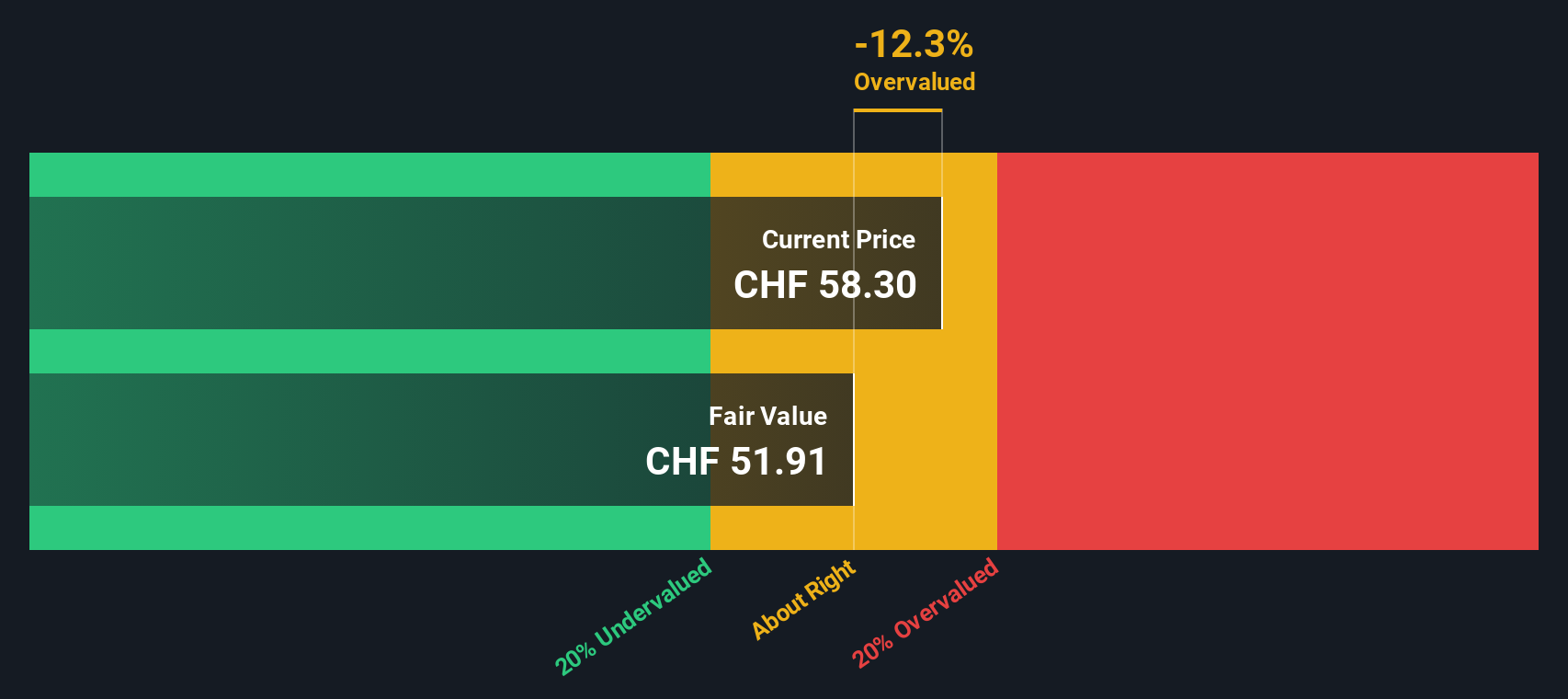

Pulling all these projections together, the DCF model calculates ABB’s fair value at $52.14 per share. Compared to the current share price, this suggests ABB stock is about 13.0% over its intrinsic value. According to this method, the shares appear somewhat expensive right now.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ABB may be overvalued by 13.0%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: ABB Price vs Earnings (PE Ratio)

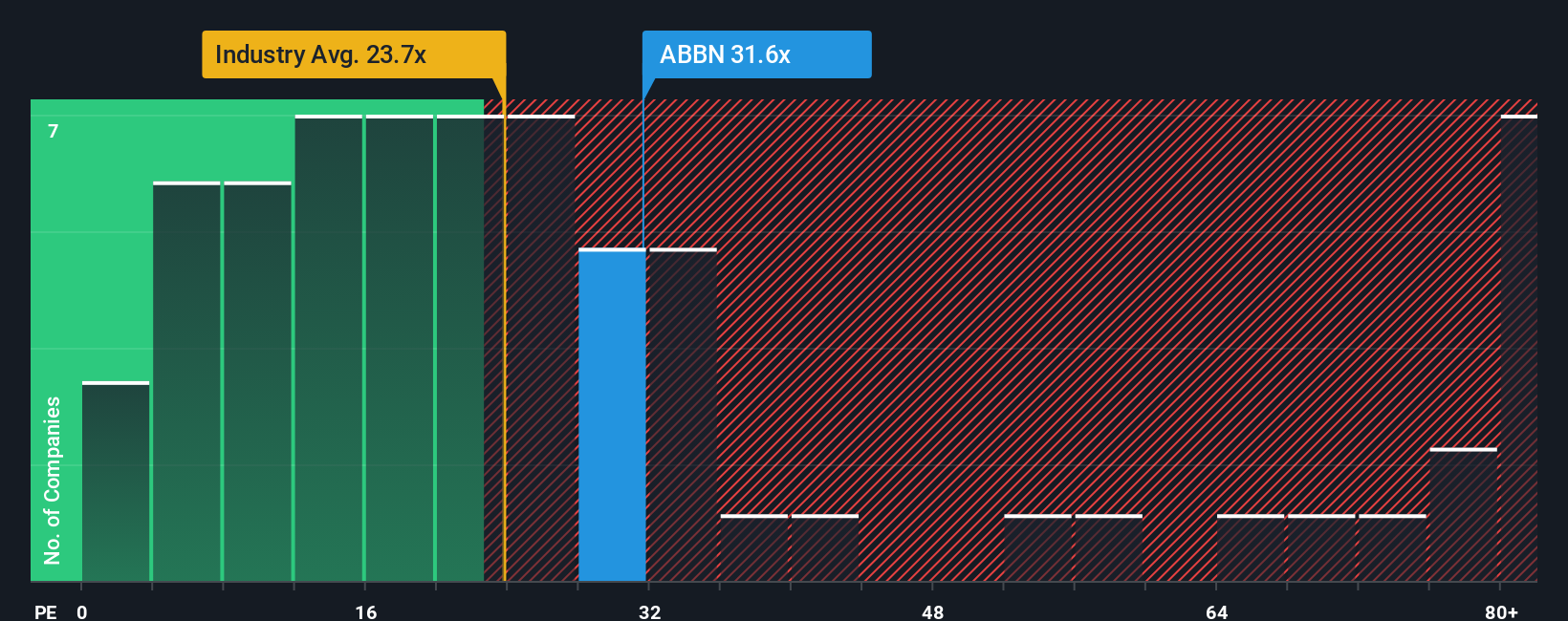

The Price-to-Earnings (PE) ratio is often the go-to metric when valuing established, profitable companies like ABB. The PE ratio helps investors quickly assess how much they are paying for each unit of earnings, which is a useful comparison point among businesses generating reliable profits.

It’s important to remember that a “normal” or “fair” PE ratio isn’t fixed. It tends to shift depending on a company’s expected growth and risk profile. Higher growth prospects or lower perceived risks can justify a higher PE, while slower growth or more uncertainty often brings that ratio down.

Currently, ABB trades at a PE of 31.9x, which is right in line with the Electrical industry average of 31.8x, and slightly above its peer group at 29.6x. While these benchmarks offer helpful context, they don’t capture the company’s full story.

That is where Simply Wall St’s “Fair Ratio” comes in. This proprietary metric calculates what ABB’s PE should be by factoring in specific elements like its earnings growth rate, profit margin, industry trends, market cap, and risk profile, rather than relying on surface comparisons alone. For ABB, the Fair Ratio is 35.0x. Because this tailored figure takes a more nuanced approach than a simple average, it can provide a clearer sense of underlying value.

With ABB’s current PE ratio just below its Fair Ratio, the numbers suggest that the stock is fairly valued based on this multiple.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your ABB Narrative

Earlier, we mentioned that there’s an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is simply your own investment story, where you connect how you see a company’s strategy, opportunities, and risks to a set of assumptions about its future revenue, earnings, and margins. This ultimately shapes your fair value estimate.

This approach bridges the gap between the “why” behind a company’s potential and the “how much” you think it’s worth, helping you anchor forecasts in real-world business drivers and industry shifts. Narratives are surprisingly easy to create, and on Simply Wall St’s Community page, millions of investors share their perspectives and keep their Narratives up to date as news, earnings, or key announcements break.

The power of Narratives is in helping you decide whether to buy, sell, or hold: by comparing your calculated Fair Value (based on your Narrative) to the current market price, you make decisions grounded in your own logic, not just broader sentiment. Since Narratives update automatically with new information, your analysis remains fresh and actionable, reflecting the latest developments.

For example, some investors project strong electrification demand and see ABB’s Fair Value as high as CHF 65, while others focus on global headwinds and estimate it closer to CHF 37. This demonstrates how different stories can lead to different investment decisions, all supported by the Narrative tool.

Do you think there's more to the story for ABB? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:ABBN

ABB

Provides electrification, motion, and automation solutions and products for customers in utilities, industry and transport, and infrastructure in Europe, the Americas, Asia, the Middle East, and Africa.

Excellent balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)